Gold Price Forecast 2026: XAU to Reach $5,000+ as Mon Pol and Tensions Drive Safe-Haven

Gold continues to establish itself as a key asset going into 2026 as expectations of looser Federal Reserve policy collide with ongoing...

Quick overview

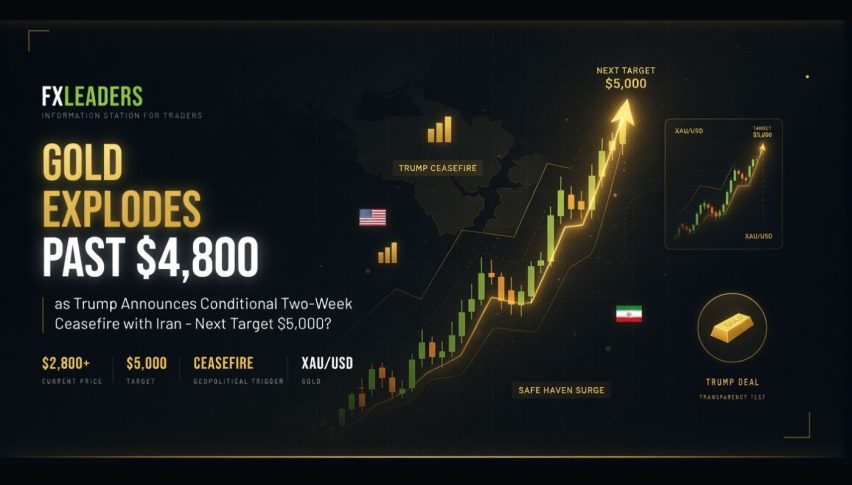

- Gold has emerged as a cornerstone asset, trading above $4,500 and approaching the $5,000 threshold amid geopolitical tensions and expectations of easier Federal Reserve policy.

- The recent rally in gold prices has been driven by disciplined accumulation from institutional and long-term investors, rather than speculative excess.

- Geopolitical risks and a cooling labor market have reinforced gold's appeal as a defensive asset, while central bank purchases continue to support its long-term value.

- As gold enters 2026, it is positioned for potential growth, supported by favorable monetary policy and strong demand, despite recent price consolidations.

Live GOLD Chart

Gold continues to establish itself as a key asset going into 2026 as expectations of looser Federal Reserve policy collide with ongoing geopolitical tensions.

Gold Holds Firm as Markets Swing Between Risk and Caution

As global markets alternate between optimism and caution, gold has emerged as one of the most consistent performers. While equities and high-beta assets experience sharp rotations, gold has maintained elevated levels, trading comfortably above $4,500 and steadily closing in on the psychologically important $5,000 threshold.

This resilience reflects more than short-term hedging. Investors increasingly view gold as strategic protection against unresolved macro risks, currency instability, and policy uncertainty. Even during periods of improving sentiment, the metal has retained strong underlying demand, reinforcing its role as a long-term store of value rather than a speculative vehicle.

Record Prices Signal Conviction, Not Speculation

Gold’s rally to record territory has unfolded in a notably disciplined manner. Unlike past cycles driven by leverage or speculative excess, the current advance has been underpinned by steady accumulation from institutional, sovereign, and long-term private investors.

After reaching new highs in late October, prices briefly consolidated as optimism around global growth and trade relations softened defensive positioning. That pause proved temporary. Renewed geopolitical tensions and lingering macro uncertainty reignited demand, pushing gold toward $4,550 in late December.

Although prices later eased by roughly $200 to close near $4,330, the pullback remained technically constructive, with key moving averages holding firm. The absence of panic selling or sharp breakdowns suggests investors are positioning for a prolonged period of elevated prices rather than a short-lived peak.

Technical Structure Reinforces the Bullish Trend

From a technical perspective, gold continues to exhibit classic accumulation behavior. Throughout the past year, pullbacks have been shallow and consistently supported by rising moving averages. The 20-day simple moving average has acted as a near-term floor, while longer-term averages continue to define a robust uptrend.

Gold Chart Daily – The 20 SMA Holding as Support

This structure has produced a steady sequence of higher lows, preserving momentum even during corrective phases. Following the resolution of a brief U.S. government shutdown and another 25-basis-point rate cut from the Federal Reserve, gold resumed its advance and surpassed previous resistance levels.

While momentum cooled slightly toward year-end amid thin holiday liquidity, there has been no sign of trend exhaustion. On the contrary, reduced liquidity may amplify price sensitivity, increasing the likelihood of an upside extension once participation normalizes.

Monetary Policy Expectations Remain a Powerful Tailwind

Federal Reserve policy continues to play a central role in gold’s strength. Markets are increasingly confident that U.S. interest rates have peaked, with futures pricing additional rate cuts extending into 2025 and 2026.

Lower yields reduce the opportunity cost of holding non-yielding assets, enhancing gold’s appeal relative to cash and bonds. Attention now turns to upcoming Federal Reserve communications, particularly meeting minutes and leadership outlook, for confirmation that policy will remain accommodative.

Speculation around future Fed leadership has added another supportive layer. Expectations that the next phase of monetary policy may lean more dovish have reinforced gold’s status as a hedge against policy uncertainty and currency debasement.

Geopolitical Risk Keeps Defensive Demand Elevated

Geopolitical tensions remain a persistent driver of gold demand. Ongoing conflicts, shifting alliances, and renewed friction between major global powers continue to inject uncertainty into financial markets.

Investors are increasingly aware that geopolitical risks are no longer isolated or short-lived events, but structural features of the global landscape. As a result, gold’s safe-haven premium has become more durable, supporting prices even during periods of relative calm.

This environment favors assets that are independent of political systems and counterparty risk, reinforcing gold’s relevance in diversified portfolios.

Labour Market Signals Encourage Defensive Positioning

Recent U.S. labour market indicators have added to gold’s appeal. Softer private payroll data, rising layoff announcements, and delays in official employment reporting suggest that labour market momentum is gradually cooling.

While these signals do not point to an imminent recession, they reinforce the view that economic growth is transitioning to a slower, more uneven phase. In such conditions, investors tend to maintain exposure to defensive assets rather than aggressively rotating into risk.

Gold’s steady bid amid these developments reflects its ability to perform well not only during crises, but also during periods of economic transition and policy recalibration.

Central Bank Buying Anchors the Long-Term Case

Perhaps the most compelling structural support for gold comes from central banks. Official sector purchases have remained strong, pushing global gold holdings to record levels. In a historic shift, central banks now collectively hold more gold than U.S. Treasuries.

This trend reflects a strategic reassessment of reserve assets, driven by a desire to diversify away from traditional financial instruments and reduce exposure to currency and geopolitical risk. While certain policy changes—such as adjustments to tax incentives in China—may temporarily affect consumer demand, sovereign and institutional buying continues to dominate the long-term picture.

Gold has gained roughly 61% year-to-date, ranking among the strongest-performing global assets and positioning it for a third consecutive year of double-digit returns.

Outlook for 2026: Stability With Breakout Potential

Gold enters 2026 with a rare combination of strength and stability. Supported by accommodative monetary policy, persistent geopolitical risk, cooling labour market dynamics, and unprecedented central bank demand, the metal remains firmly positioned as a core asset in an increasingly complex global environment.

Rather than signaling exhaustion, recent consolidation appears to be strengthening the foundation for the next advance. With liquidity conditions improving after the holiday period, gold may be well positioned to challenge the $5,000 level in the year ahead.

In a world where certainty remains elusive, gold continues to justify its role as a trusted anchor for investors navigating shifting economic and political terrain.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts