dow

Forex Signals Brief July 30: Ford, MSFT, META, QUALCOMM Pre-Earnings

Markets pulled back from record highs as investors processed the results of U.S.-China trade negotiations, shifting economic indicators...

•

Last updated: Wednesday, July 30, 2025

Quick overview

- U.S.-China trade negotiations concluded with a constructive tone, aiming for a rebalancing of economic relations.

- The U.S. trade deficit narrowed significantly, driven by a decline in imports, indicating potential shifts in domestic consumption.

- Mixed economic signals emerged, with job vacancies falling slightly while consumer confidence improved ahead of the upcoming jobs report.

- U.S. equities paused after reaching record highs, as investors awaited clarity from central banks and economic data.

Live DOW Chart

DOW

Markets pulled back from record highs as investors processed the results of U.S.-China trade negotiations, shifting economic indicators, and anticipated several major policy decisions.

Constructive Progress in U.S.-China Talks

The major highlight of the day came from trade news, specifically the conclusion of a two-day negotiation between U.S. and Chinese officials. Treasury Secretary Bessent described the tone of the talks as “very constructive,” reinforcing that the United States does not aim to decouple from China but rather seeks a rebalancing of the economic relationship.

U.S. Trade Representative Greer projected that the bilateral trade imbalance could decline by at least $50 billion this year. He also reminded markets that President Trump still has the authority to adjust existing tariffs on Chinese imports if needed. Greer acknowledged China’s protest over U.S. objections to Iranian oil purchases, stating that Washington currently lacks the direct power to intervene on that front.

EU Deal Celebrated as Trade Deficit Narrows

In transatlantic trade developments, Commerce Secretary Lutnick praised the recently completed EU-U.S. agreement, which opens up access to the $20 trillion European market. Referring to it as a “masterclass,” Lutnick was visibly enthusiastic—though some observers noted that modesty might have been more appropriate given the volatility surrounding prior negotiations.

Elsewhere, the U.S. trade balance posted a notable improvement last month, narrowing from $96.42 billion to $85.99 billion. A significant $11 billion decline in imports was the key driver of this drop, suggesting a possible slowdown in domestic consumption or more favorable terms of trade.

Mixed Economic Signals Ahead of Jobs Data

Economic indicators released during the session painted a mixed picture. Job vacancies, as reported in the JOLTS survey, came in slightly below expectations, hinting at a gradual softening in labor demand. Meanwhile, consumer confidence climbed from 95.0 to 97.2, showing that household sentiment remains solid despite economic uncertainty. The Atlanta Fed also revised its Q2 GDP estimate upward from 2.4% to 2.9%, reflecting stronger-than-expected underlying growth in both services and manufacturing as the quarter drew to a close. All eyes now turn to the upcoming U.S. jobs report, due on Friday, which could either reinforce or challenge the prevailing narrative of resilience.

Stocks Pause After Setting New Highs

After a wave of optimism drove the S&P 500 and NASDAQ to record highs on Monday, U.S. equities took a breather. The Dow Jones Industrial Average slipped by 0.46%, hitting its lowest level since December 2024. The S&P 500 lost 0.30%, while the tech-heavy NASDAQ fell 0.38%. The Russell 2000, which tracks smaller-cap companies, fared the worst with a decline of 0.61%. The pullback was largely seen as a healthy pause following a strong rally, as traders awaited additional clarity from central banks and economic data.

Key Market Events Today

Key Central Bank Announcements on the Horizon

FOMC Announcement

Markets are now focused on Wednesday’s key central bank announcements, beginning with the Federal Reserve. The Federal Open Market Committee is expected to leave interest rates unchanged at the current range of 4.25% to 4.50%. While the consensus among economists is firmly in favor of a hold, some Fed officials, including Governors Waller and Bowman, have signaled support for a rate cut due to signs of a cooling labor market. Analysts at Morgan Stanley anticipate dissenting votes in favor of a 25 basis point reduction, potentially adding an element of surprise to the otherwise predictable decision.

US Q2 GDP

In terms of growth, the advance estimate for U.S. Q2 GDP is expected to show a rebound to 2.5% annualized, recovering from the prior quarter’s -0.5% contraction. The Atlanta Fed’s GDPNow model is currently projecting 2.4%, and recent PMI data from S&P Global suggest that both services and manufacturing sectors gained momentum by quarter’s end.

EZ Q2 GDP

Across the Atlantic, Eurozone GDP is also due on Wednesday. Analysts expect flat growth for the second quarter, following a 0.6% expansion in Q1. On a year-over-year basis, growth is forecast to slow from 1.6% to 1.2%. Much of Q1’s strength was attributed to front-loaded European exports to the U.S. ahead of anticipated Trump administration tariffs—an effect unlikely to repeat this quarter.

BOC Announcement

Meanwhile, the Bank of Canada is also scheduled to release its rate decision. The central bank is widely expected to keep its policy rate unchanged at 2.75%, a midpoint within its estimated neutral range. Given rising uncertainty over North American trade policies and global demand, the BoC is unlikely to provide explicit forward guidance. However, its accompanying Monetary Policy Report may shed light on how policymakers view the impact of U.S. tariffs on the Canadian economy.

Mixed Signals in Big Tech and Auto: Key Takeaways from Q2 2025 Earnings Reports

The Q2 2025 earnings season revealed a mixed bag across industries. Tech giants like Microsoft and Meta delivered solid growth from AI and ad platforms, while chipmaker Qualcomm showed strength in its core business. However, challenges remain for companies like Ford and Applied Digital, with cost pressures and demand shifts weighing on outlooks. As markets digest these results, investor focus turns to operational execution and strategic positioning for the second half of the year.

Ford Motor Company (F) – Q2 2025 Earnings Announcement

- Reported modest growth, but profit margins were squeezed by rising input and labor costs.

- EV segment faced ongoing challenges, with softer consumer demand and higher battery expenses.

- Traditional vehicle sales held steady, buoyed by strong fleet orders and incentives.

Microsoft Corporation (MSFT) – Q4 2025 Earnings Announcement

- Cloud and AI divisions continued to drive revenue growth, surpassing expectations in Azure and Copilot-related services.

- Enterprise software demand remained stable, but Windows license sales dipped slightly in developed markets.

- Announced new AI partnerships and infrastructure investments to support long-term scaling.

Meta Platforms, Inc. (META) – Q2 2025 Earnings Announcement

- Advertising revenue grew strongly, particularly from Instagram Reels and international markets.

- Threads and VR-related investments showed mixed progress, with Reality Labs still operating at a loss.

- Emphasized a renewed focus on monetization efficiency and generative AI rollout within apps.

QUALCOMM Incorporated (QCOM) – Q3 2025 Earnings Announcement

- Surpassed expectations due to a rebound in global smartphone shipments and demand for high-end 5G chips

- Automotive and IoT chip sales also improved, though margins were pressured by pricing competition.

- Provided upbeat guidance for Q4 as inventory levels normalize and demand rebounds in Asia.

Robinhood Markets, Inc. (HOOD) – Q2 2025 Earnings Announcement

- User growth slowed, but revenue rose thanks to increased interest income and a spike in crypto trading volumes.

- Operating costs remained elevated due to expansion efforts and legal reserves.

- Highlighted upcoming product launches aimed at increasing user retention and institutional adoption.

Applied Digital Corporation (APLD) – Q4 2025 Earnings Announcement

- Reported a wider-than-expected loss as data center profitability declined amid rising power costs.

- Some contracts with AI clients were delayed or revised, impacting forward revenue expectations.

- Management expressed confidence in new energy-efficient infrastructure projects underway for FY 2026.

Last week, markets were slower than what we’ve seen in recent months, with gold retreating and then bouncing to finish the week unchanged. EUR/USD slipped toward 1.16, while S&P and Nasdaq continued higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

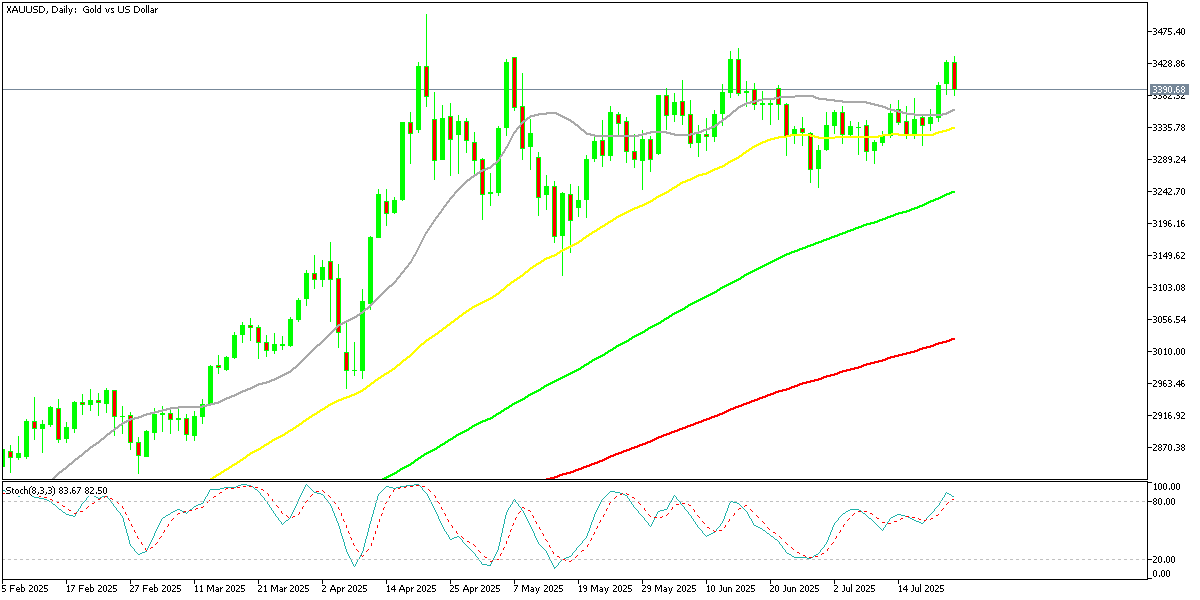

Gold Returns Below $3,400

Gold rebounded off its 20-week moving average near $3,150, climbing nearly $50 to finish around $3,438/oz. Still, after failing to hold above $3,400 post-U.S.-Japan trade talks, gold appears stuck in a consolidation phase below the $3,500 resistance. Traders await fresh inflation clues or remarks from the Fed to trigger the next move.

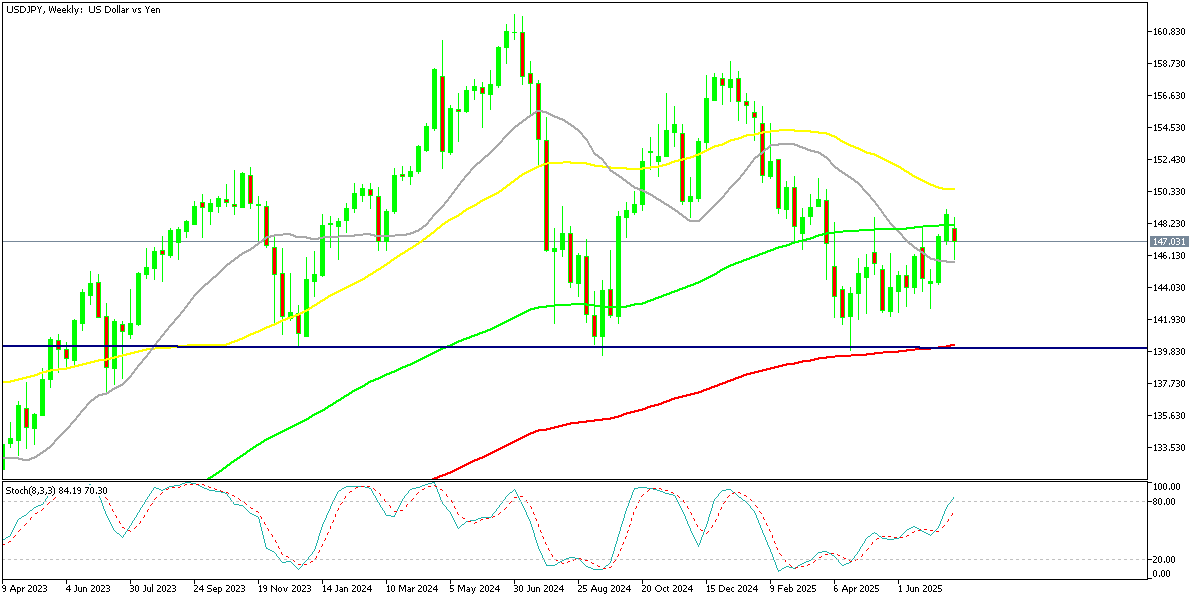

USD/JPY Returns Below the 100 Weekly SMA After Japanese Elections

USD/JPY Breakout Challenges BoJ Forecasts

The U.S. dollar surged past the 148 yen threshold, surprising many who expected further yen strength. This rally also took the pair above the 100-week moving average, a significant technical barrier often viewed as a long-term resistance level.

Fueling the move is a wave of Japanese capital seeking returns abroad, which is complicating the Bank of Japan’s policy outlook. If the pair manages to close the week firmly above this level, it could reinforce sentiment in favor of the dollar and reignite discussions around the policy gap between the Federal Reserve and the Bank of Japan.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Rebounds Strongly After Brief Breakdown

Bitcoin momentarily slipped under $113,000 earlier in the week but quickly reversed course, bouncing back above $120,000 with notable force. The dip triggered strong buying interest as the cryptocurrency tested its 50-day moving average, while further support held at the 20-week SMA.

Market participants appear to be treating these pullbacks as opportunities to reenter, especially amid ongoing uncertainty in traditional markets. Bitcoin’s recovery suggests continued appetite for digital hedges in times of macro volatility.

BTC/USD – Weekly chart

Ethereum Inches Closer to $4,000

Ethereum has recently outshone Bitcoin, rising 20% since April and breaking decisively above its 100-week moving average. The rally is being fueled by growing optimism over the upcoming “Pectra” upgrade, which is expected to significantly improve Ethereum’s scalability and transaction efficiency.

This upgrade has caught institutional attention, with increased inflows supporting the bullish momentum. Now targeting the $4,000 level, Ethereum is regaining favor as a high-conviction bet in the crypto space.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts