btc-usd

Forex Signals Brief August 1: Meta and Microsoft Lift Tech, Tariffs and Fed Concerns Pressure Markets

Wall Street navigated a volatile session as strong Big Tech earnings, fresh tariff headlines, and firm inflation data clashed to shape...

•

Last updated: Friday, August 1, 2025

Quick overview

- Wall Street experienced volatility as strong Big Tech earnings clashed with inflation data and tariff headlines.

- June's core PCE inflation rose 0.3% month-over-month, raising concerns for the Fed and reducing the likelihood of a September rate cut.

- Tech stocks like Meta and Microsoft saw significant gains, while broader indices faced profit-taking and selling pressure.

- The U.S. labor market is under scrutiny with expectations of slower job growth and a slight rise in the unemployment rate.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

Wall Street navigated a volatile session as strong Big Tech earnings, fresh tariff headlines, and firm inflation data clashed to shape market sentiment.

Inflation Data and Fed Caution

June’s core PCE inflation rose 0.3% month-over-month, marking the sharpest increase since February and keeping the annual rate at 2.8%, slightly above the 2.7% forecast. Rising costs in furniture, household goods, and recreational products—magnified by tariff-related pressures—highlighted the Fed’s ongoing inflation concerns.

Although the Fed anticipates that tariff-driven price increases may prove temporary, policymakers remain wary of delayed pass-through effects. Consecutive 0.3% monthly gains suggest inflation volatility could persist, cutting the probability of a September rate cut from 65% to 39%. For now, interest rates are likely to remain at 4.25%–4.50% until a more convincing disinflation trend emerges.

Market Performance and Big Tech Earnings

Markets opened sharply higher as Microsoft and Meta’s stellar results drove early NASDAQ gains of over 327 points. However, profit-taking and rate-sensitive selling reversed the optimism, leaving the NASDAQ slightly lower by the close, while the Dow, S&P, and Russell 2000 all retreated.

Even as broader indices softened, tech giants delivered outsized moves. Meta soared 11.25% to fresh records, and Microsoft climbed nearly 4%, underscoring the market’s reliance on mega-cap tech leadership. After-hours, Apple stock rose following its earnings beat, while Amazon plunged 7% as cautious guidance overshadowed a revenue beat.

Commodity and Currency Reactions

Tariff developments weighed heavily on metals. Copper prices tumbled after President Trump imposed 50% tariffs on semi-finished copper products and derivatives, effective August 1, 2025. The exclusions for scrap, concentrates, and refined cathodes caught the market by surprise, contributing to volatility.

Key Market Events Today

August 1st Tariff Deadline (Fri):

Energy Earnings on Deck

Chevron (CVX) and Exxon Mobil (XOM) are reporting Q2 2025 earnings amid a challenging energy price backdrop. Analysts expect EPS of $1.66 for Chevron and $1.49 for Exxon, both reflecting year-over-year declines exceeding 30%. Despite the weaker headline figures, both companies have a track record of exceeding forecasts, and market participants will closely monitor margins and production updates for signs of resilience.

Eurozone CPI Preview

The Eurozone’s July inflation release is expected to show a slight pullback in price pressures after June’s modest rebound. Headline HICP inflation is projected at 1.9% year-over-year, down from 2.0%, while the super-core measure—which strips out the most volatile items—is expected to ease to 2.2% from 2.3%.

June data showed headline inflation ticking up to 2.0%, while super-core held steady at 2.3% and services inflation rose to 3.3% from 3.2%. ING described the rebound as softer than anticipated after May’s “unusually low” reading. Investec now sees little reason for prices to have shifted significantly in July, with mild upward pressure from services likely offset by the firmer euro, which dampens goods prices.

Looking ahead, Eurozone inflation dynamics remain highly sensitive to the strength of the euro and to evolving trade frictions with the United States. July’s European Central Bank policy meeting emphasized a “wait-and-see” stance, with officials seeking clarity on both trade agreements and the durability of disinflation before adjusting rates.

U.S. Jobs Report Preview

The U.S. labor market will be in the spotlight with Friday’s July nonfarm payrolls report. Economists expect the economy to have added around 102,000 jobs, down from 147,000 in June. This compares to a three‑month average of 150,000 and a six‑month average of 130,000, suggesting a gradual cooling in employment growth.

The unemployment rate is expected to rise slightly to 4.2%, inching closer to the Fed’s year‑end projection of 4.5%. Average hourly earnings are forecast to increase by 0.3% month‑over‑month, up from 0.2% in June, while average workweek hours are likely to remain steady at 34.2.

Barclays analysts are more cautious than consensus, forecasting just 75,000 jobs, including a 25,000 decline in government employment, while private payrolls could modestly accelerate to around 100,000.

Last week, markets were slower than what we’ve seen in recent months, with gold retreating and then bouncing to finish the week unchanged. EUR/USD slipped toward 1.16, while S&P and Nasdaq continued higher. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

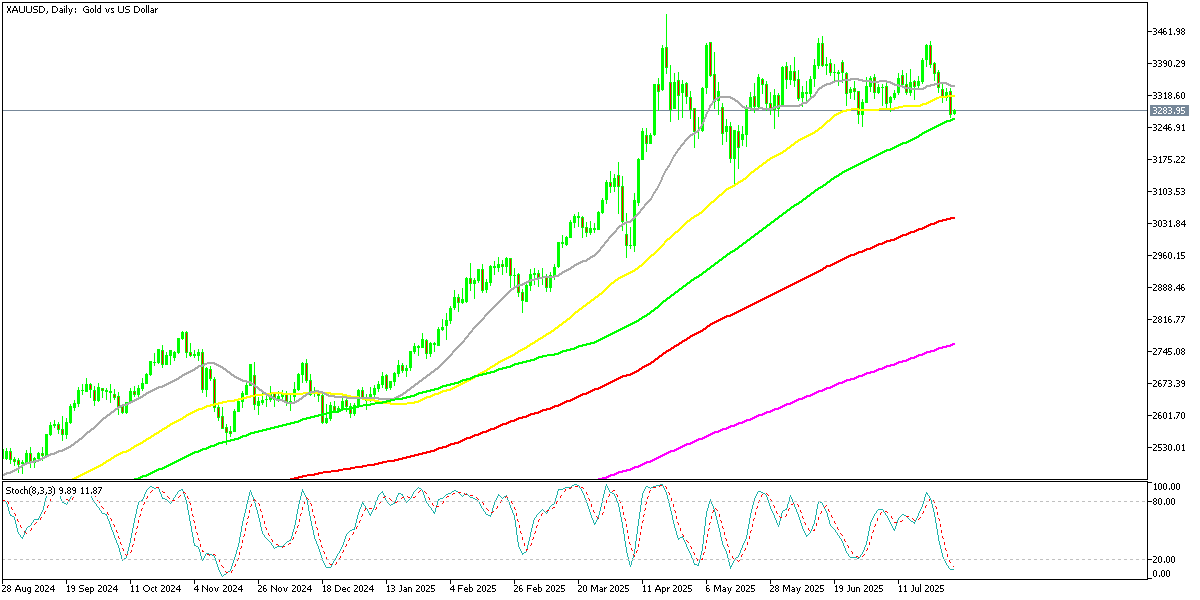

Gold Returns Below $3,300

Gold, which briefly touched $3,438/oz earlier this month, has entered a two-week slide, now trading near $3,268/oz. The metal is testing support at the 100-day SMA, while Fed hawkishness and dollar strength continue to cap upside potential. But the 100 daily SMA (green) is holding for now on the daily chart.

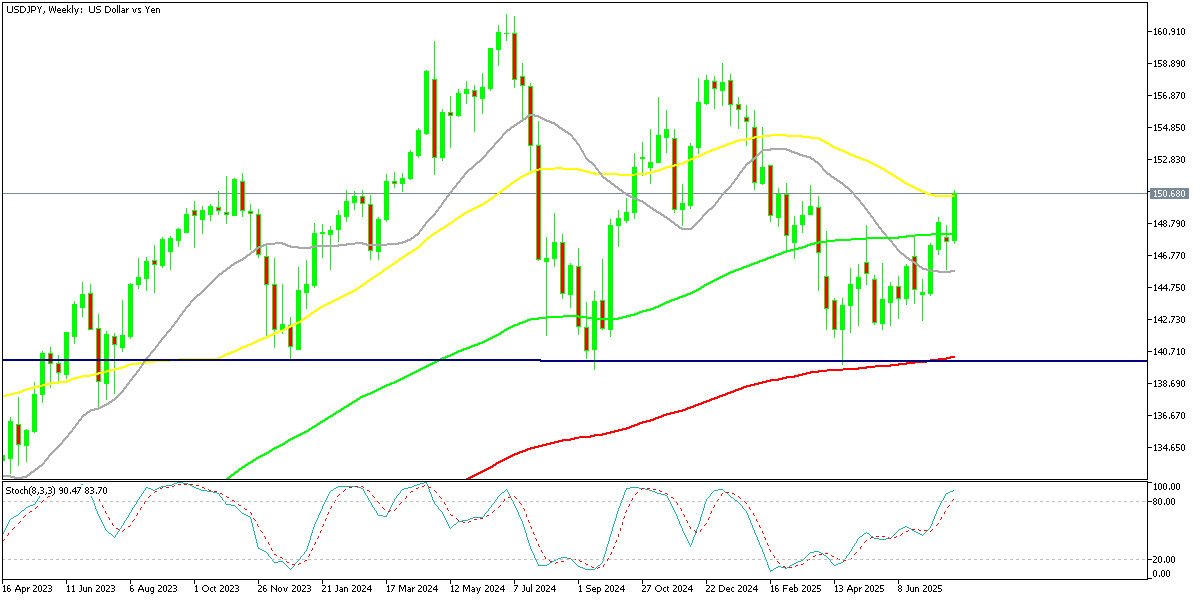

USD/JPY Breaks Above $150 Again

Meanwhile, the U.S. dollar surged above ¥150, breaking its 50-week moving average and reinforcing the policy divergence narrative between the Fed and the Bank of Japan. This move signals renewed Japanese capital outflows seeking higher yields abroad.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Pulls Back to $115K

Bitcoin momentarily slipped under $113,000 earlier in the week but quickly reversed course, bouncing back above $120,000 with notable force. The dip triggered strong buying interest as the cryptocurrency tested its 50-day moving average, while further support held at the 20-week SMA.

Market participants appear to be treating these pullbacks as opportunities to reenter, especially amid ongoing uncertainty in traditional markets. Bitcoin’s recovery suggests continued appetite for digital hedges in times of macro volatility.

BTC/USD – Weekly chart

Ethereum Inches Closer to $4,000

Ethereum has recently outshone Bitcoin, rising 20% since April and breaking decisively above its 100-week moving average. The rally is being fueled by growing optimism over the upcoming “Pectra” upgrade, which is expected to significantly improve Ethereum’s scalability and transaction efficiency.

This upgrade has caught institutional attention, with increased inflows supporting the bullish momentum. Now targeting the $4,000 level, Ethereum is regaining favor as a high-conviction bet in the crypto space.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts