btc-usd

Forex Brief August 5: AMD, Caterpillar and SMCI Earnings in Focus

Major U.S. companies across tech, industrials such as AMD, SMCI and Caterpillar are set to release critical quarterly results, with...

•

Last updated: Monday, August 4, 2025

Quick overview

- Major U.S. companies, including AMD, SMCI, and Caterpillar, are set to release important quarterly results, with investors keenly awaiting guidance and surprises.

- Equity markets have rebounded strongly after last week's decline, with the NASDAQ and S&P 500 showing signs of bullish momentum despite remaining below previous highs.

- The U.S. services sector showed strong growth in July, but concerns about uneven momentum and deteriorating manufacturing conditions persist.

- New Zealand's labor market is expected to show signs of weakening, with rising unemployment and moderating wage growth potentially influencing monetary policy.

Live BTC/USD Chart

BTC/USD

0.0000

MARKETS TREND

Major U.S. companies across tech, industrials such as AMD, SMCI and Caterpillar are set to release critical quarterly results, with investors watching for guidance and market-moving surprises.

Equity Markets Stage Strong Comeback

After last week’s sharp decline sparked by a weaker-than-expected U.S. jobs report, major indices bounced back impressively. The NASDAQ index climbed away from its 200-hour moving average and closed above its 100-hour moving average at 20,987.91, signaling a return of short-term bullish momentum. However, it remained below Thursday’s closing level of 21,122.45, leaving some ground to recover.

The S&P 500 also regained most of its losses, closing at 6,329.94 versus 6,339.39 last Thursday. Despite the rebound, the index remains just under its 100-hour moving average, keeping traders cautious. Market participants now look to Tuesday’s session as a critical test for the technical bias in both the S&P 500 and NASDAQ.

Forex Market Stays Quiet with One Outlier

Foreign exchange markets were relatively muted, with most major pairs trading within 0.20% of Friday’s close. The standout mover was USD/CHF, which rose 0.50%, reflecting a weaker Swiss franc.

Comments from San Francisco Fed President Mary Daly added a layer of intrigue, as she suggested the Federal Reserve may need to take further action if economic data weakens, leaving the door open for more than two rate cuts.

Key Market Events for the Day

US ISM Services PMI – Signals Strong but Uneven Growth

The July flash PMI report from S&P Global showed U.S. services sector business activity climbing to 55.2, up from 52.9 in June, marking a seven-month high. This expansion was largely driven by domestic demand, making services the primary engine of growth for the U.S. economy last month.

S&P Global highlighted that the pace of activity in services had not been seen since December, helping offset weakness in manufacturing. However, the report included a cautious note, stressing that this momentum is “worryingly uneven” and heavily dependent on the services economy, as manufacturing conditions deteriorated for the first time in 2025. The fading boost from tariff front-running also raises questions about the sustainability of the current expansion.

New Zealand Jobs – Labor Market Faces Pressure

The New Zealand Q2 2025 labor market report, due Tuesday, is expected to show weakening employment conditions. Forecasts are:

- Employment Change: -0.2% Q/Q (previous +0.1%)

- Unemployment Rate: 5.3% (previous 5.1%)

- Labour Cost Index (LCI): 0.6% Q/Q, 2.2% Y/Y

Analysts at Westpac project that job losses will continue, concentrated among younger workers. However, labor force exits are likely to moderate the rise in the unemployment rate. Wage pressures are expected to ease slightly, as signaled by the LCI, which should continue to show ongoing but moderating growth.

The forecast remains softer than the RBNZ’s May projections, reinforcing expectations that New Zealand’s labor market is cooling, with rising joblessness and slower wage gains potentially influencing monetary policy outlooks in the months ahead.

Key Earnings Announcements – Today’s Highlights

Today’s earnings slate represents a cross-section of the U.S. economy: semiconductors (AMD, SMCI) signaling AI and tech growth, heavy machinery (CAT) reflecting global industrial health, and media (FOX) testing advertising and streaming resilience. Market reactions will likely hinge not only on earnings figures but also forward guidance, particularly in sectors exposed to macroeconomic cycles and demand trends.

1. Advanced Micro Devices (AMD) – Q2 2025

Sector: Semiconductors & Computing

Focus Points:

- Market is closely watching AI chip sales and server processor demand, which have been AMD’s primary growth drivers.

- GPU competition with NVIDIA and progress on MI300 series adoption will be key discussion points.

- Analysts expect sequential revenue growth, but margins may face pressure due to heavy R&D and next-gen product ramp-up.

Market Impact:

A strong earnings beat or optimistic guidance could reinforce semiconductor sector momentum, while a miss may trigger profit-taking after recent tech rallies.

2. Caterpillar Inc. (CAT) – Q2 2025

Sector: Industrials / Heavy Equipment

Focus Points:

- Investors are monitoring construction machinery and mining equipment sales, especially in North America and emerging markets.

- Currency impacts, China demand recovery, and infrastructure spending trends will influence the outlook.

- Operating margins could fluctuate as input costs and supply chain dynamics continue to normalize.

Market Impact:

Strong earnings may signal resilience in the industrial cycle, while weak orders could raise concerns about global growth and construction activity.

3. Super Micro Computer (SMCI) – Q4 2025

Sector: Technology / Data Center Hardware

Focus Points:

- Market will watch for continued hyperscale server demand and AI-driven growth in rack-scale systems.

- Supply chain management and ability to fulfill backlog orders will be crucial for sustaining momentum.

- Any guidance on AI infrastructure expansion could heavily influence stock sentiment, given SMCI’s recent high-volatility trading patterns.

Market Impact:

A robust report could push shares toward new highs, reinforcing its role as an AI infrastructure leader, while a miss could trigger sharp downside given high expectations.

Last week, markets were quite volatile, with gold retreating and then bouncing to finish the week unchanged. EUR/USD slipped toward 1.14 but also rebounded on Friday, while S&P and Nasdaq ended the week lower. The moves weren’t too big though, and we opened 35 trading signals in total, finishing the week with 23 winning signals and 12 losing ones.

Support Holds for Gold

Gold prices remain trapped below their April peak as safe-haven demand meets fading momentum, with markets watching labor data and global tensions for the next trigger. Gold has been stabilizing under record levels since late April, caught between geopolitical uncertainty and shifting Federal Reserve expectations. After the Fed left interest rates unchanged at last week’s FOMC meeting, XAU/USD briefly fell to $3,268 before rebounding strongly, supported by the 100-day simple moving average.

Weak U.S. employment data, which some investors questioned for accuracy, fueled the rebound into the weekend, so this week’s Unemployment Claims take extra importance for Gold traders, as they will confirm or dismiss Friday’s NFP data. Despite this, buyers have been unable to retake the $3,450–$3,500 zone, leaving GOLD in a prolonged consolidation phase.

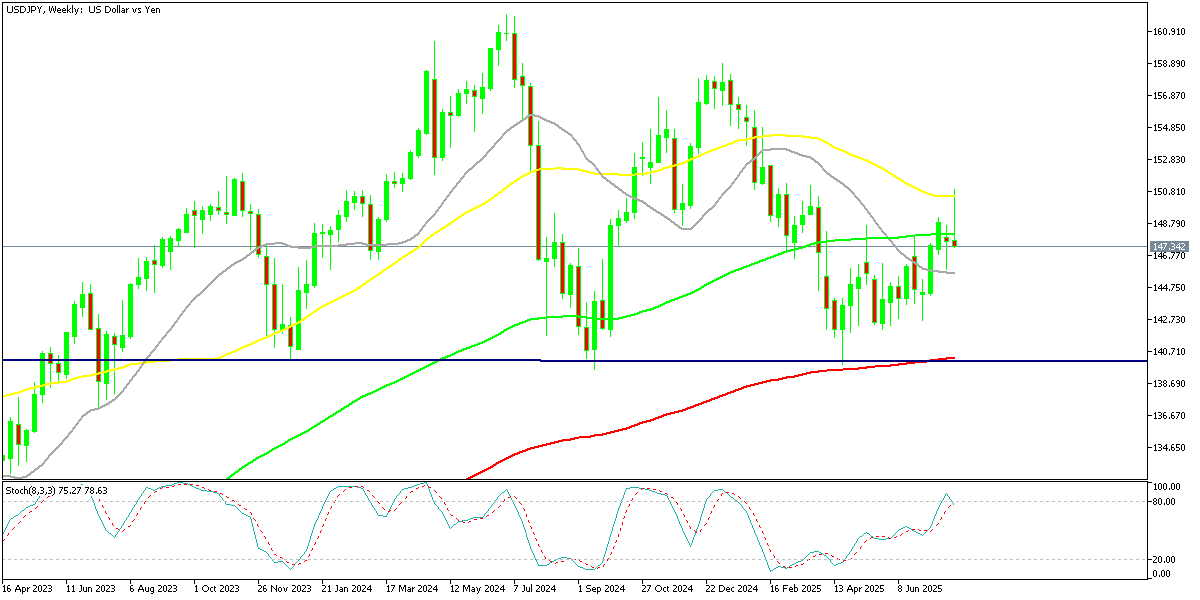

USD/JPY Dives to $147

The dollar initially surged against the yen, breaking its 50-week moving average and climbing above ¥150, as investors leaned into the policy divergence between the Fed and the Bank of Japan. Reports suggested that Japanese capital was again flowing overseas in search of higher returns. However, Friday’s weak U.S. jobs report sparked a pullback, with USD/JPY sliding nearly four cents as traders reassessed the labor market outlook.

USD/JPY – Weekly Chart

Cryptocurrency Update

Bitcoin Buyers Return

Cryptocurrencies remained a bright spot in an otherwise unsettled market. Bitcoin briefly fell below $112,000 last week before rebounding strongly off the previous high zone, which seems to have turned into support now.

BTC/USD – Weekly chart

Ethereum Inches Closer to $4,000

Ethereum continued to outshine Bitcoin, rallying 20% since April and breaking its 100-week moving average. The move has been fueled by optimism over the upcoming “Pectra” upgrade, which promises to enhance scalability and transaction efficiency, drawing renewed institutional inflows. Ethereum is now aiming for the $4,000 level, reinforcing its role as a favored high-conviction asset in times of macro uncertainty.

ETH/USD – Daily Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Skerdian Meta

Lead Analyst

Skerdian Meta Lead Analyst.

Skerdian is a professional Forex trader and a market analyst. He has been actively engaged in market analysis for the past 11 years. Before becoming our head analyst, Skerdian served as a trader and market analyst in Saxo Bank's local branch, Aksioner. Skerdian specialized in experimenting with developing models and hands-on trading. Skerdian has a masters degree in finance and investment.

Related Articles

Sidebar rates

Related Posts