AMD Stock Surges 16.5% After Hours as Data Center Revenue Jumps 57% and Q2 Guidance Crushes Estimates

AMD's 57% data center surge and $11.2 billion Q2 outlook signal it's no longer Nvidia's shadow but also a second force in AI chips.

Quick overview

- AMD reported a strong Q1 2026 with revenue of $10.25 billion and adjusted EPS of $1.37, both exceeding expectations.

- The Data Center division emerged as the primary revenue driver, with sales up 57% year-over-year to $5.8 billion.

- AMD's strategic partnerships, including a commitment to deploy 6 gigawatts of GPUs with Meta, position it as a key player in AI infrastructure.

- Despite strong performance, AMD faces challenges such as declining gross margins and competition from Intel in the CPU market.

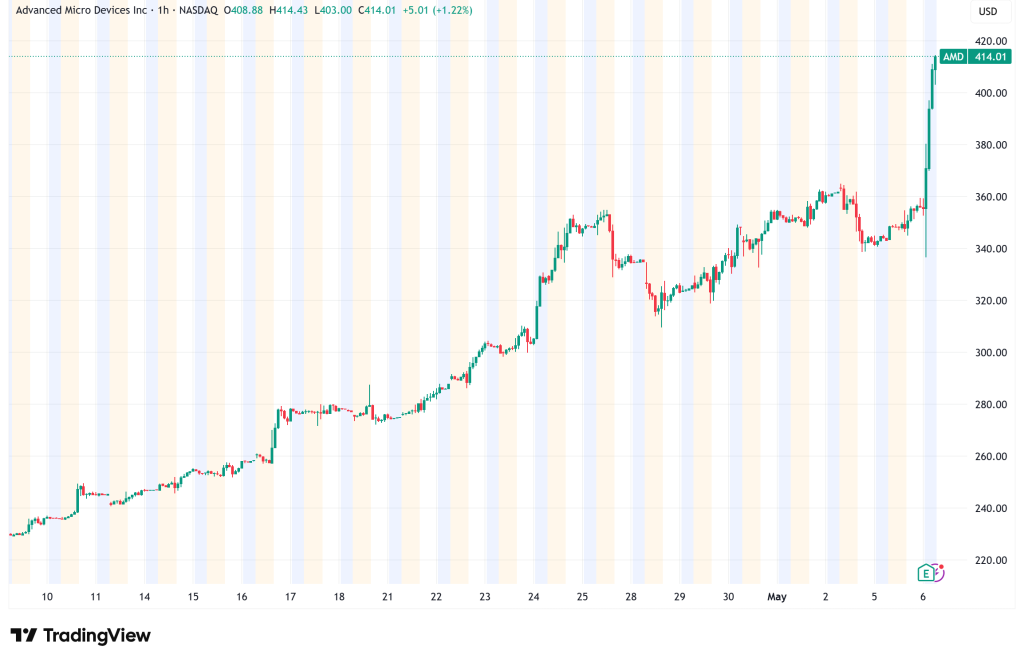

For naysayers, AMD (NASDAQ: AMD) had a quarter that will be hard to ignore. Revenue of $10.25 billion surpassed consensus by 4%, adjusted EPS of $1.37 beat by 6% and Q2 forecast of $11.2 billion beat expectations by over $700 million. The stock, which was up 66% year-to-date before the print, rallied another 16.5% in after-hours trading to $414, knocking down lingering worries about whether AMD’s AI momentum was translating into actual financial results.

Net income almost quadrupled year-over-year to $1.38 billion and non-GAAP operating income grew 43% to $2.54 billion. Also, CEO Lisa Su made it clear that the Data Center division is now “the primary driver of our revenue and earnings growth” — a milestone that represents a fundamental transformation in the kind of company AMD is becoming.

AMD’s Data Center Sales Run Hot

The headline metric out of the quarter was Data Center sector sales of $5.8 billion — up 57% year over year and above the $5.64 billion consensus projection. On both sides of the data center business, EPYC server CPUs continuing taking market share from key cloud providers, and Instinct GPU shipments kept ramping up to fulfill AI infrastructure demand.

Meta and AMD revealed plans to deploy up to 6 gigawatts of AMD Instinct GPUs, with the first gigawatt powered by a unique MI450-based design. Meta will also act as a lead client for AMD’s future 6th Gen EPYC CPUs. Leading the quarter were AWS, Google Cloud, Microsoft Azure, and Tencent announcing new or expanded EPYC powered cloud instances.

Maybe the most notable strategic move is AMD’s Helios rack-scale AI system, its answer to Nvidia’s Grace Blackwell and Vera Rubin platforms that retail for more than $3 million a piece. Both Meta and Open AI have already signed up for Helios shipments, which will begin in the second half of 2026. Su said these deals position AMD to be “a core partner to the world’s largest AI infrastructure builders, with deep co-engineering relationships and multiyear visibility into large-scale deployments.”

CPU Renaissance Continues to Support AMD’s Outlook

Another subplot worthy of equal attention is the resurrection of the CPU market. CPUs are seeing demand levels not seen in years as AI workloads transition from model training toward inference and agentic AI applications. AMD is in a great place here with EPYC leadership and recent market share increases.

Now the business estimates the server CPU addressable market will expand at more than 35% annually to reach more than $120 billion by 2030, a substantial change from the 18% annual growth it anticipated only six months ago. And for the server CPU business, revenue is predicted to climb over 70 percent year over year in Q2 alone.

AMD and Intel have also teamed up on AI computation Extensions for x86 CPUs, which will boost speed and energy efficiency by increasing computation density 16-fold. The partnership is especially interesting given the long-standing rivalry between the two firms and it reflects a broader convergence in the industry on the use of CPU acceleration for AI.

Risks to Watch for AMD Investors

Not all of the print was perfect. Non-GAAP gross margin was down sequentially 55% from 57% in Q4 2025 and GAAP operating margin was down three percentage points quarter-over-quarter. All of AMD’s manufacture is outsourced, to TSMC, and that poses capacity limits Intel (currently ramping its own in-house manufacturing) doesn’t have. As Nvidia’s AI roadmap advances, AMD might have to lock in additional production capacity earlier than it had anticipated.

Another consumer-facing impediment is the global memory chip scarcity. AMD anticipates PC shipments to decrease in the second half, with gaming revenue down more than 20% in the second half from the first half, impacted by rising memory and component costs weighing on demand. Client and Gaming rose 23% YoY in Q1 but the outlook is more cautious beyond.

Another consideration is competition from Intel, which has posted its strongest performance in years following a protracted recovery. Intel’s ambitious CPU ramp is in direct competition with the market share AMD has been grabbing. And the struggle for TSMC capacity between AMD, Nvidia and others is still a structural constraint on how fast AMD can scale.

What to Expect From AMD Stock in Q2 2026

AMD’s Q1 2026 results are a major tipping point. A 57% revenue increase in data centers, Q2 guidance that blew away estimates, a commitment to deploy 6 gigawatts of Meta GPUs, and a rack-scale AI system with OpenAI and Meta as launch customers paint a picture of a company that has gone from being Nvidia’s challenger to a legitimate co-incumbent in AI infrastructure.

The climb to $414 prices in a lot of that optimism after hours. For traders the key level to watch on any pullback is $375-$380 which was the prior closing range before the earnings trigger. A sustained hold over $400 would pave the way for new highs. The true test will come in Q2, when AMD has to prove it can turn its growing order book into high-margin income — and that Helios is shipping on time.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts