Oracle Slumps: ORCL Stock Down 37% Amid Weak AI Profit, Targets $200 Zone

Oracle's stock is struggling to maintain its pace as investors start to worry about diminishing margins and losing faith in the company's...

Quick overview

- Oracle's stock is facing challenges due to insider selling and declining investor confidence in its AI and cloud growth prospects.

- Recent insider transactions, including a significant sale by co-CEO Clay Magouyrk, have raised concerns about the company's near-term outlook.

- Oracle's shares have dropped over 30% from record highs, with technical indicators suggesting a bearish trend and potential further declines.

- As competitors like Nvidia and Microsoft thrive, Oracle's profitability and growth narrative are increasingly questioned amid rising operational costs.

Oracle’s stock is struggling to maintain its pace as investors start to worry about diminishing margins and losing faith in the company’s once-hyped cloud growth story.

Mounting Pressure from Insider Sales

Oracle Corporation (NYSE: ORCL) extended its losing streak this week, undercut by a string of high-profile insider transactions and softening institutional sentiment.

Recent regulatory filings revealed that newly appointed co-CEO Clay Magouyrk sold 40,000 shares last week, pocketing roughly $11 million. The sale — coming just days after his promotion — raised eyebrows across Wall Street and fueled speculation that senior executives may be losing faith in Oracle’s near-term growth outlook.

Institutional investors have echoed that caution. Buckhead Capital Management LLC trimmed its Oracle position by more than 50%, while Tiemann Investment Advisors LLC reduced its stake by 21% during the second quarter, according to recent SEC filings. The wave of selling, both inside and outside the company, has heightened market skepticism at a time when other big tech peers are posting strong results.

Sharp Technical Breakdown

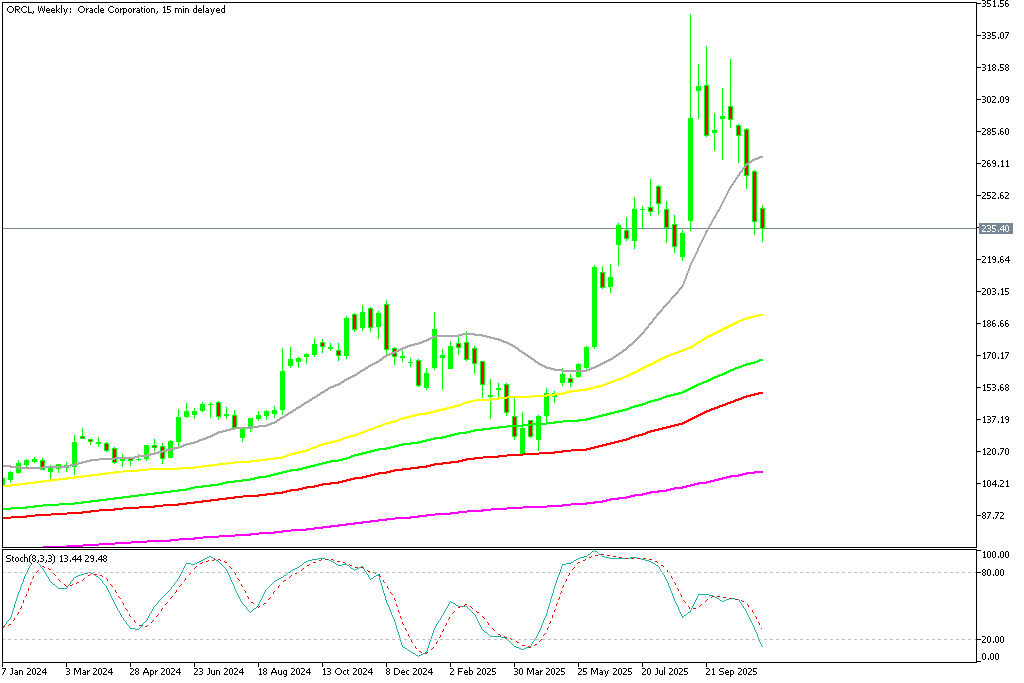

After reaching record highs above $345 in early September, Oracle’s shares have since tumbled by more than 30%, now hovering near $230. The stock has fallen decisively below its 20-week simple moving average (SMA) — a key level that had served as support for much of 2024.

Technical strategists warn that continued selling pressure could drive ORCL down toward $200, a previous breakout zone from early 2024 that may now serve as the next support level. The company’s technical outlook has shifted firmly bearish, with both the 50-day and 100-day SMAs flattening and turning lower — classic signs that the uptrend has reversed.

ORCL Chart Daily – Likely the Price Will Fall Below the 50 SMA

The weakness in Oracle stock intensified after CoreWeave’s 15% plunge earlier this week, triggered by a disappointing revenue forecast and supply chain hiccups at one of its data center partners. Although analysts from Mizuho emphasized that the CoreWeave setback was “specific to CRWV” and not directly tied to Oracle’s operations, investor sentiment across the AI infrastructure space soured broadly.

AI Ambitions Meet Harsh Reality

Oracle’s meteoric rise earlier this year was fueled by investor excitement over its AI and cloud infrastructure expansion, powered in part by Nvidia’s GPU technology. But as the dust settles, the financial returns appear underwhelming.

According to recent reports, Oracle’s Nvidia-linked cloud business generated roughly $900 million in revenue last quarter — but just $125 million in gross profit. That translates to a meager 14% margin, significantly lagging behind Microsoft Azure and Amazon Web Services, which operate at far higher profitability levels.

Rising energy costs, data center expenses, and infrastructure commitments are squeezing margins, undermining Oracle’s claim of being a serious AI infrastructure contender. The result: analysts are increasingly questioning whether Oracle’s AI narrative is more about hype than substance.

Lagging Behind Big Tech Rivals

While Oracle battles internal uncertainty, Nvidia, Microsoft, and Palantir have been powering higher. Nvidia continues to post record-breaking profits on soaring chip demand, while Microsoft’s Azure division has delivered consistent double-digit growth. Palantir, once seen as a niche analytics player, is now winning major government and enterprise AI contracts — a stark contrast to Oracle’s slowing growth.

The divergence underscores a growing belief that Oracle’s growth story may have peaked, at least temporarily. Despite expanding its AI partnerships and cloud footprint, the company’s execution has lagged its marketing promises.

Confidence Erodes as Growth Story Weakens

Investor confidence in Oracle’s long-term vision is eroding. The company’s AI-driven profitability remains uncertain, and cost pressures are rising across its infrastructure operations. With insiders selling into strength and institutions trimming exposure, the perception of internal caution is adding fuel to the fire.

Analysts warn that without clear evidence of margin recovery or a meaningful acceleration in cloud growth, Oracle may continue to lag behind its peers well into 2026. For now, optimism has been replaced by hesitation — and what was once a high-flying AI narrative is now being tested by hard financial reality.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM