Nvidia (NVDA) Delivers $81.6B Revenue Shock as AI Demand Turns Parabolic

Quick overview

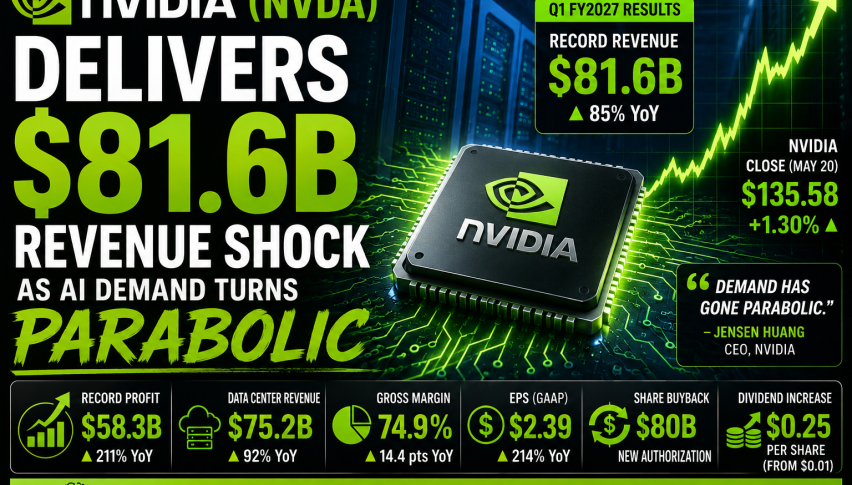

- Nvidia reported a record fiscal Q1 2027 revenue of $81.6 billion, up 85% year-over-year, with net income soaring to $58.3 billion.

- Despite strong results, Nvidia shares experienced a slight decline in after-hours trading, reflecting high market expectations.

- The company is expanding its focus beyond GPUs into inference computing and has announced significant new products and an $80 billion share buyback authorization.

- Nvidia faces increasing competition from major tech companies developing custom AI chips, but it maintains a strong position across multiple layers of AI infrastructure.

Shares of NVDA remained near record highs after the AI chip giant delivered another blockbuster quarter, posting results that once again reset expectations for the entire semiconductor industry.

The company reported fiscal Q1 2027 revenue of $81.6 billion, up 85% year-over-year, while net income surged to $58.3 billion. Data center revenue — Nvidia’s core AI growth engine — climbed 92% to a record $75.2 billion.

Despite the massive beat, the market reaction was muted. Nvidia shares slipped modestly in after-hours trading, underscoring how extraordinarily high expectations have become for the world’s most valuable company.

As one analyst put it: “Nvidia is no longer beating the bar — it is the bar.”

AI Infrastructure Spending Is Still Exploding

Nvidia’s results reinforced one core theme dominating markets in 2026: the AI infrastructure boom is far from slowing.

CEO Jensen Huang described demand as “parabolic,” driven by the rise of agentic AI systems capable of autonomous reasoning and execution.

“The buildout of AI factories — the largest infrastructure expansion in human history — is accelerating at extraordinary speed,” Huang said.

The company’s numbers support that claim.

NVIDIA’s Q1 FY2027 Highlights

| Metric | Result | YoY Growth |

|---|---|---|

| Revenue | $81.6B | +85% |

| Net Income | $58.3B | +211% |

| Data Center Revenue | $75.2B | +92% |

| Networking Revenue | $14.8B | +199% |

| Gross Margin | 74.9% | +14.4 pts |

| EPS | $2.39 | +214% |

Nvidia also forecast Q2 revenue of roughly $91 billion, comfortably above Wall Street expectations near $86.8 billion.

Nvidia Is Expanding Beyond GPUs

While Nvidia still dominates AI accelerators through Blackwell GPUs, the company is rapidly broadening its platform.

A major focus now is inference computing — the process of running trained AI models in production.

That shift is important because inference workloads increasingly require:

- Faster networking

- Efficient CPUs

- Optical interconnects

- Distributed AI infrastructure

- Lower power consumption

Nvidia unveiled several new products targeting that transition, including:

- Vera CPU platform

- Rubin AI architecture

- BlueField-4 infrastructure systems

- Dynamo inference software

- Agentic AI tools and frameworks

Huang said the new Vera CPU opens access to a potential $200 billion market.

He also revealed that Vera-related revenue was not included in Nvidia’s previously projected $1 trillion Blackwell and Rubin opportunity between 2025 and 2027.

NVDA Shareholder Returns Send a Strong Signal

Nvidia also announced one of the largest buyback authorizations in tech history.

The board approved:

- An additional $80 billion share repurchase authorization

- A dividend increase from $0.01 to $0.25 per share

The company returned roughly $20 billion to shareholders during the quarter through buybacks and dividends.

That matters because it signals Nvidia is evolving from a pure hypergrowth company into a cash-generation machine.

According to GraniteShares CEO William Rhind:

“When the marginal use of capital starts shifting toward buybacks and dividends, you’re watching a hypergrowth story begin to mature in real time.”

NVDA Technical Analysis: Momentum Remains Extremely Strong

Technically, NVDA continues trading in one of the strongest long-term uptrends in global markets. The chart shows the stock consolidating near record highs after a multi-year AI-driven breakout.

Key Technical Signals

- Shares remain above all major moving averages

- Long-term trend structure remains bullish

- Volume trends remain supportive

- Institutional accumulation continues

- Momentum indicators remain elevated but constructive

Moving Averages

The bullish setup remains intact:

- 20-day moving average: rising

- 50-day moving average: rising

- 200-day moving average: rising

This alignment confirms strong long-term momentum.

RSI and MACD

RSI appears elevated following Nvidia’s massive rally, suggesting the stock is approaching overbought conditions.

That raises the possibility of:

- Short-term consolidation

- Sideways price action

- Volatility around earnings reactions

However, MACD momentum remains firmly positive, indicating buyers still control the broader trend.

Key Support and Resistance Levels

| Level Type | Approximate Area |

|---|---|

| Immediate Resistance | Near recent highs |

| Psychological Resistance | $250 equivalent post-split zone |

| Near-Term Support | 20-day moving average |

| Secondary Support | 50-day moving average |

| Major Trend Support | 200-day moving average |

As long as Nvidia remains above major moving averages, bulls are likely to maintain control.

NVIDIA’s Competition Is Rising

Despite Nvidia’s dominance, competitive pressures are growing.

Major hyperscalers including:

- Alphabet

- Amazon

- Microsoft

are increasingly developing custom AI chips internally.

At the same time, rivals such as:

- Advanced Micro Devices

- Intel

are aggressively targeting inference and server CPU markets.

Nvidia is responding by expanding deeper into networking, CPUs, software, optics, robotics, automotive AI, telecom infrastructure, and enterprise AI systems.

The Biggest Risk for NVDA Stock: Expectations

The largest challenge for Nvidia may no longer be execution.

It may simply be expectations.

The company continues delivering historic growth, yet investors increasingly view massive earnings beats as routine.

That explains the muted stock reaction despite extraordinary results.

Analysts also continue debating whether the AI boom risks creating a bubble across technology markets.

Some concerns include:

- Slowing AI monetization

- Overspending by hyperscalers

- Competition from custom silicon

- Supply constraints

- Valuation risk

- AI demand normalization after 2027

Huang himself acknowledged supply limitations could persist across the lifecycle of the Vera Rubin platform.

Long-Term Outlook: Nvidia Still Controls the AI Stack

Despite growing competition, Nvidia remains uniquely positioned.

The company now controls multiple layers of AI infrastructure:

- GPUs

- CPUs

- Networking

- AI software

- AI operating systems

- Inference optimization

- Autonomous systems

- Data center infrastructure

That ecosystem advantage remains extraordinarily difficult to replicate.

Importantly, Nvidia is no longer just selling chips.

It is increasingly selling entire AI platforms.

As AI workloads shift from training to autonomous inference systems, Nvidia appears determined to own both sides of the market.

For now, the numbers continue justifying the bullish narrative. But after becoming a $5 trillion company, Nvidia faces a new reality: extraordinary growth is no longer surprising — it is simply expected.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts