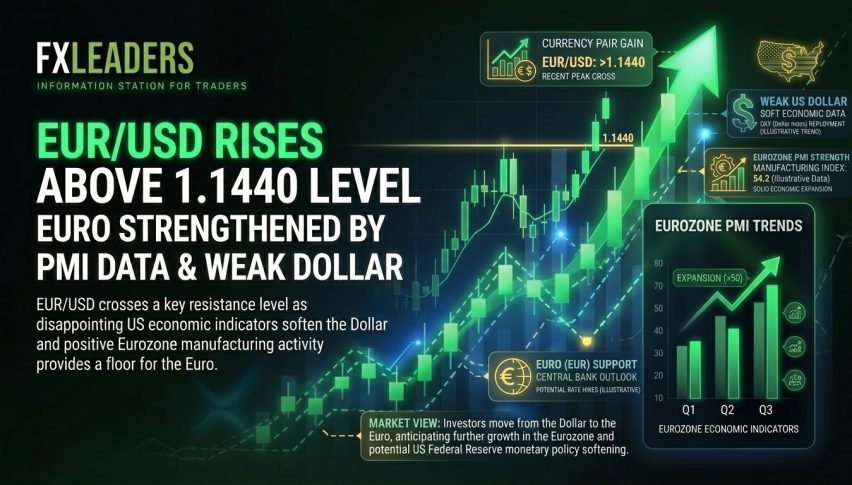

US dollar on 6th day losing streak

The US Dollar Index posted its sixth consecutive decline amid an improved appetite for risk

The US Dollar Index posted its sixth consecutive decline amid an improved appetite for risk. The U.S. dollar index traded at roughly 102.6 index points on Thursday during the London trading session.

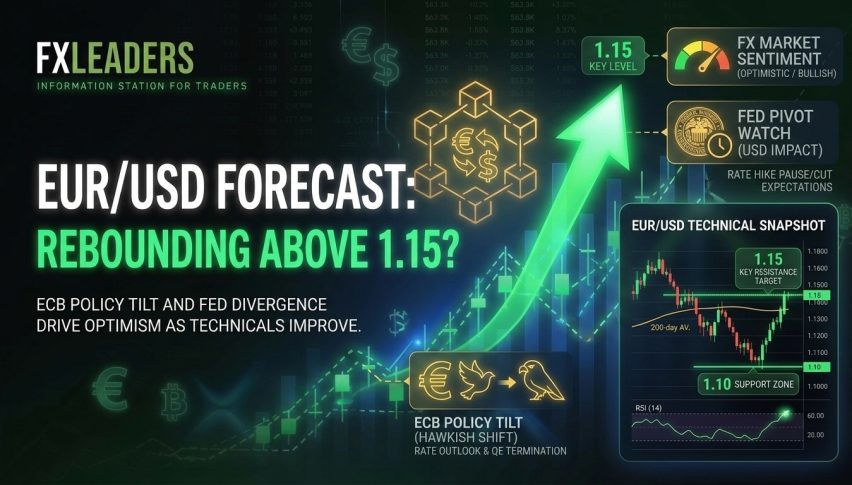

The EUR/USD pair retreats from the fresh seven-month high, consolidating its gains around 1.1010 during Thursday’s early European session The Eurozone’s Q2 GDP growth figure came in as expected, boosting the morale of the European currency.

The Consumer Price Index data released on Wednesday indicated a slight increase in the US inflation rate for July, on an annualized spectrum, which puts pressure on the Greenback. This has increased anticipation that the Federal Reserve will likely decrease interest rates by at least 25 basis points in September.

The US Consumer Price Index (CPI) increased 2.9% in July compared to the previous year, slightly lower than the 3% increase in June and less than anticipated by the market.

Except for food and energy, the Core CPI increased 3.2% YoY. This was less than the 3.3% increase in June but still in line with market expectations.

Investors debate the extent of the Federal Reserve’s (Fed) September rate reduction. With a 60% probability, traders are inclining toward a more moderate 25 basis point drop, although a 50 basis point cut is still possible. CME FedWatch estimates a 36% probability that the greater cut in September.

US President Joe Biden suggested that Iran wouldn’t attack Israel if a ceasefire is achieved in Gaza. These comments would have reinforced the risk-taking mindset and likely pressure on the haven currency. New cease-fire negotiations are scheduled in Qatar on Thursday, despite Hamas’s declaration that it will not participate in the talks. After holding flat at 0 percent in June, US retail sales are expected to rise to 0 percent on Thursday for July. The University of Michigan’s Consumer Sentiment Index for August is anticipated to report a new reading later this week, predicted to rise from 66.4 to 66.9.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts