Nvidia NVDA Stock Risks Falling Under $200 as Rising Costs, China Risks Weigh on

Thanks to its Q1 profits, NVIDIA enjoyed again another stellar quarter; but, mounting prices and geopolitical risks put pressure on the stock.

Quick overview

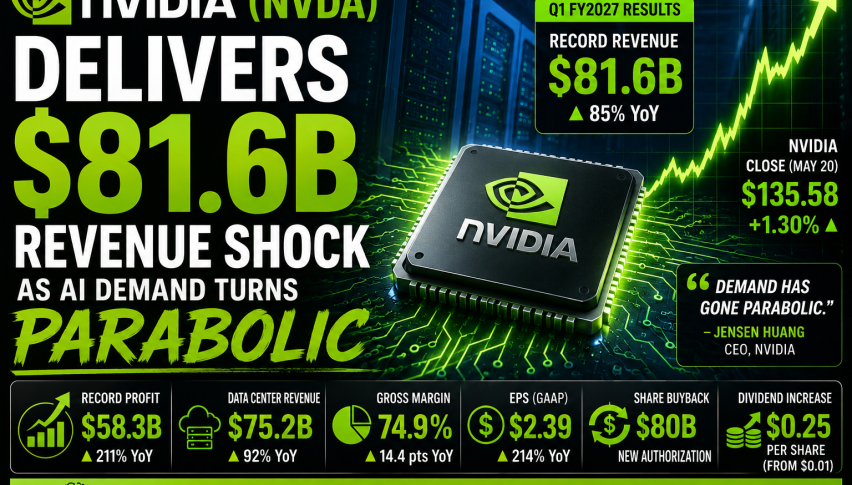

- NVIDIA reported Q1 FY27 revenue of $81.6 billion, driven by strong demand in the data center segment, particularly from hyperscale cloud providers.

- Despite impressive revenue growth, rising operating expenses and tax pressures have raised concerns about the company's profitability and efficiency.

- Geopolitical tensions and export restrictions have led to a forecast of no Data Center compute revenue from China in Q2, limiting growth potential.

- NVIDIA's stock has shown volatility, recently slipping below key technical support levels, while the company continues to return capital to shareholders through buybacks and dividends.

Live NVDA Chart

[[NVDA-graph]]

Thanks to its Q1 profits, NVIDIA enjoyed again another stellar quarter; but, mounting prices and geopolitical risks put pressure on the stock.

Strong Revenue Growth Anchored by Data Center Demand

NVIDIA reported Q1 FY27 revenue of $81.6 billion, marking a 20% sequential increase and an 85% year-on-year surge, underscoring sustained demand for high-performance computing infrastructure. The results were again driven by hyperscale cloud providers and continued expansion in AI-driven data center buildouts.

Earnings also came in strong, with GAAP diluted EPS of $2.39, supported by elevated pricing power and robust margins across its premium GPU and networking products. Gross margin remained exceptionally high at 74.9%, reinforcing NVIDIA’s dominant position in advanced semiconductor and compute systems.

The Data Center segment remained the core growth driver, generating $75.2 billion in revenue, with particularly strong performance in networking solutions as global infrastructure expansion continued at scale.

Rising Costs and Expanding Capital Pressure

Despite strong top-line growth, investor sentiment weakened as costs accelerated across multiple fronts. Operating expenses rose to $7.6 billion, driven by increased R&D spending, infrastructure investment, and intensifying competition in the semiconductor space.

Tax pressures also increased meaningfully, with income tax expense reaching $11.6 billion, adding another layer of drag on net profitability. Meanwhile, investing cash outflows climbed to $26.4 billion, highlighting the capital-intensive nature of sustaining leadership in next-generation compute platforms.

Although operating cash flow remained strong at $50.3 billion, markets appeared increasingly concerned that rising structural costs could gradually erode the efficiency profile that has defined NVIDIA’s growth cycle.

China Restrictions Add a Layer of Uncertainty

A key overhang for the outlook was management’s expectation of no Data Center compute revenue from China in Q2, reflecting ongoing export restrictions and geopolitical tensions. This continues to remove a major addressable market from near-term projections.

While global demand remains robust, particularly in North America, the absence of China growth limits upside optionality and increases reliance on a small group of hyperscale buyers. This dynamic contributed to a cautious reassessment of forward valuation assumptions.

Technical Picture Reflects Waning Momentum

Nvidia’s technical setup mirrors the shifting sentiment. The stock slipped below its 20-day simple moving average (gray) in early May, but reversed back up, so it provided reliable support and NVDA reached a new high of $236 last week before earnings. But then the stock reversed down and now sellers are testing the 20 SMA again. If it breaks, we will likely see a deeper pullback to $200.

NVDA Chart Daily – Heading to $200

Buybacks Support Sentiment but Don’t Eliminate Risks

NVIDIA returned approximately $20 billion to shareholders through buybacks and dividends during the quarter. It also authorized an additional $80 billion share repurchase program, signaling confidence in long-term cash generation.

The quarterly dividend was increased to $0.25 per share, reinforcing a stronger capital return posture.

However, despite these measures, shares declined for a second consecutive session and remain about 9% below recent highs, as investors weigh exceptional growth against rising execution, cost, and geopolitical risks.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts