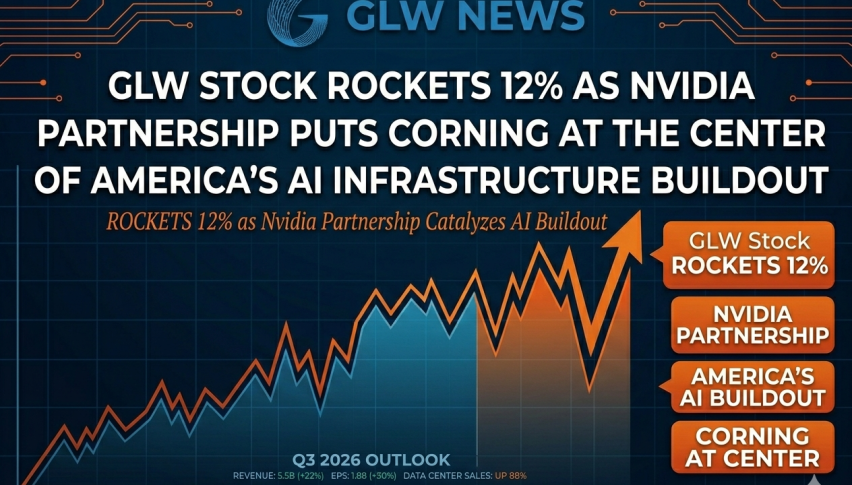

GLW Stock Rockets 12% as Nvidia Partnership Puts Corning at the Center of America’s AI Infrastructure Buildout

A $500 million Nvidia deal, three new US factories, and a path to $35 billion in sales by 2030, Corning is no longer just a glass company.

Quick overview

- Corning Incorporated has partnered with Nvidia as its optical connection partner for AI infrastructure, marking a significant commercial and strategic alliance.

- The partnership includes Nvidia purchasing shares from Corning and promises a tenfold increase in optical connectivity production and new manufacturing plants in the US.

- Corning's Springboard growth plan has been upgraded, with management projecting revenues of up to $40 billion by 2030 due to increasing demand for AI-driven optical connectivity.

- Despite positive analyst upgrades and a strong growth trajectory, Corning's high valuation raises caution for investors.

Corning Incorporated (NYSE: GLW) has been inventing things the world didn’t realize it needed for 175 years, including low-loss optical fiber, Gorilla Glass and LCD display panels. The company added another chapter on Wednesday: as the designated optical connection partner for the AI infrastructure buildout for Nvidia.

Nvidia Picks Corning as Its Optical Partner

The alliance established on May 6 is both a commercial supply deal and a strategic equity tie. Nvidia will buy 3 million shares from Corning for a token price and has options to buy another 15 million shares at $180 apiece, giving Jensen Huang’s company a direct financial stake in Corning’s fortunes. In return, Corning promises a massive increase in capacity: a tenfold increase in optical connectivity production, a more than 50% increase in fiber production in the US, and three new sophisticated manufacturing plants in North Carolina and Texas employing more than 3,000 individuals.

Huang described the relationship broadly: “AI is fueling the biggest infrastructure buildout of our time, and a once-in-a-generation opportunity to revitalize American manufacturing and supply chains.” For a company whose devices literally carry data through glass at the speed of light, the timing couldn’t be better.

What Makes Optical Connectivity Critical Infrastructure Now?

To appreciate why the deal is important beyond the headline statistics, it’s useful to know what optical fiber performs in an AI data center. Modern AI training and inference workloads require thousands of Nvidia GPUs working in close coordination, transferring huge amounts of data across chips, servers and racks at speeds and distances that copper cable cannot cheaply sustain. As AI factories get larger and more tightly interconnected, optical fiber moves from a nice-to-have to a foundational requirement.

The reason Nvidia has been aggressively locking up optical and fiber supply chain partnerships is precisely because the bottleneck isn’t just making GPUs, it’s transporting data between those GPUs. Corning, the originator of low-loss optical fiber and the world’s foremost innovator in optical physics, is the natural anchor partner for that plan.

This is not Corning’s first big AI infrastructure deal either. Corning in January won a $6 billion multiyear contract to aid Meta with its data center buildout, a contract that helped strengthen its bona fides as a hyperscaler supplier even before the Nvidia announcement.

Corning Springboard Plan Gets a Meaningful Upgrade

The relationship with Nvidia brought a major boost to Corning’s Springboard growth plan. Management now sees a road to $20 billion in annualized revenues by the end of 2026, ahead of prior estimates, with a high-confidence path to $27 billion by 2028 and an internal stretch goal of $30 billion. The strategy was also extended to 2030 with a high-confidence objective of $35 billion and an internal goal of $40 billion.

These are not gradual modifications. This reflects a fundamental reappraisal of Corning’s addressable market as demand for AI-driven optical connectivity expands from a data center niche to a key infrastructure requirement. Management forecasts growth to accelerate considerably starting in 2027 driven by AI related demand through its Enterprise Networks and Photonics products.

The path was already set in the recently released Q1 2026 results. Revenue of $4.35 billion was better than the $4.29 billion projection, EPS of $0.70 was ahead of the $0.69 consensus and the standout driver was the Optical Communications business. The company also said it would pay a quarterly dividend of 28 cents a share on June 29.

Analysts Raise Targets for Corning Stock, But Valuation Warrants Caution

Wolfe Research upgraded its price target to $230 from $185 and kept an Outperform rating in response to the Nvidia cooperation. The company raised its 2028 revenue forecast to $27.5 billion and EPS forecast to $5.75, citing fewer competition, technical and supply chain risk as warranting a higher multiple as the data center potential scales. Ahead of the next earnings period, five experts have raised the earnings estimates.

Other recent analyst movements include Citigroup boosting its target to $175, Susquehanna to $180 and BarCap to $149. The widespread trust in the growth trajectory is reflected in the Buy consensus rating.

The warning flag is the valuation. Corning trades at a P/E of 86.84, which is high for an industrial manufacturer, even one with real AI tailwinds of infrastructure. InvestingPro’s Fair Value analysis finds the company to be overvalued at current levels. The $200 psychological barrier level is anticipated to draw profit-taking as the stock approaches from below. RSI is neutral at 52.63 and does not indicate the momentum advance has yet entered technically overbought area — which may allow more extension before a consolidation.

What to Watch Next for Corning Investors

Corning’s 12% leap to an all-time high is a warranted re-rating not a speculative pop. The Nvidia alliance makes strategic sense, financial sense and operational sense – three new plants, 3,000 jobs and a tenfold boost in capacity are not press release abstractions. The earlier Meta deal now cements Corning’s positioning as critical optical infrastructure for the two businesses spending most aggressively on AI data center buildout.

For traders, the $158-$162 zone now serves as important medium-term support and $200 is the immediate psychological resistance to watch. Wolfe Research’s $230 goal serves as a directional anchor for longer term positioning. The danger is that the high valuation leaves the stock sensitive to any downturn in AI capex sentiment – but for now, momentum and the underlying story are aligned.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts