Nvidia Stock NVDA Heading to 200 Again as Costs Rise and China Risks Return

Growing expenses, geopolitical unpredictability, and strong spending pressures undermined investor confidence in NVIDIA despite yet another strong quarter driven by data center demand, sending the stock lower for the second consecutive day.

Quick overview

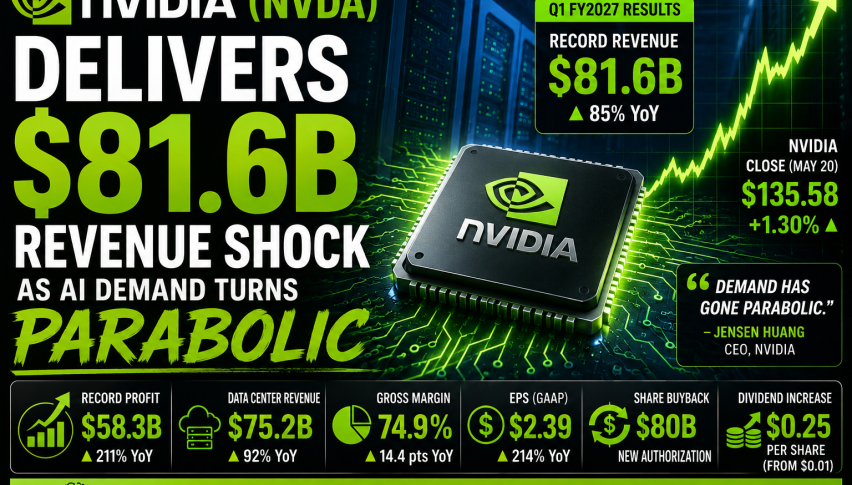

- NVIDIA reported strong Q1 FY27 revenue of $81.6 billion, marking a 20% sequential increase and an 85% year-over-year jump, driven by high demand for computing infrastructure.

- Despite impressive revenue growth, rising operating expenses and tax burdens raised concerns about the sustainability of profitability, leading to a decline in investor confidence.

- Geopolitical tensions and export restrictions have created uncertainty, particularly regarding the absence of Data Center revenue from China, which could limit future growth potential.

- NVIDIA's stock has shown waning momentum, with recent technical indicators suggesting a potential pullback to the $200 level amid rising investor caution.

Growing expenses, geopolitical unpredictability, and strong spending pressures undermined investor confidence in NVIDIA despite yet another strong quarter driven by data center demand, sending the stock lower for the second consecutive day.

Revenue Growth Remains Strong

NVIDIA reported Q1 FY27 revenue of $81.6 billion, representing a 20% sequential increase and an 85% jump compared to the same period last year. The results once again reflected strong demand for high-performance computing infrastructure and continued spending from hyperscale cloud providers.

GAAP diluted earnings per share reached $2.39, supported by elevated margins and continued pricing strength across NVIDIA’s premium product lineup. Gross margin remained exceptionally high at 74.9%, highlighting the company’s dominant market position in advanced computing hardware.

However, despite the impressive headline figures, investors appeared increasingly focused on the sustainability of growth as operational pressures continue building beneath the surface.

Rising Costs Begin to Pressure Sentiment

While revenue expanded rapidly, operating expenses climbed sharply to $7.6 billion, reflecting rising infrastructure investments, research spending, and escalating competitive pressures across the semiconductor industry.

At the same time, NVIDIA’s income tax expense surged to $11.6 billion, adding another layer of pressure to profitability. The company also reported investing cash outflows of $26.4 billion, underscoring the growing capital intensity required to maintain its leadership position.

The market reaction suggested concerns that accelerating expenses may eventually begin to erode the efficiency and profitability that investors have come to expect from NVIDIA during the current infrastructure boom.

China Restrictions Continue to Cloud Outlook

One of the biggest concerns surrounding the quarter was management’s expectation of no Data Center compute revenue from China during Q2. Ongoing export restrictions and geopolitical tensions continue to create uncertainty around one of the world’s largest technology markets.

Although NVIDIA’s global demand remains strong, the absence of China-related revenue growth could limit upside momentum in future quarters and increase reliance on North American hyperscale spending.

This uncertainty contributed to weaker post-earnings sentiment, with shares declining over two consecutive trading sessions as investors reassessed valuation risks near the $200 level.

Technical Picture Reflects Waning Momentum

Nvidia’s technical setup mirrors the shifting sentiment. The stock slipped below its 20-day simple moving average (gray) in early May, but reversed back up, so it provided reliable support and NVDA reached a new high of $236 last week before earnings. But then the stock reversed down and now sellers are testing the 20 SMA again. If it breaks, we will likely see a deeper pullback to $200.

NVDA Chart Daily – Heading to $200

Data Center Demand Still Drives the Business

The Data Center division remained the core growth engine, generating $75.2 billion in revenue during the quarter. Networking revenue within the segment posted especially strong gains as large-scale infrastructure buildouts continued across enterprise and cloud computing markets.

Operating cash flow improved substantially to $50.3 billion, reinforcing the company’s ability to generate enormous cash even as spending requirements continue expanding.

Still, the broader market response suggested that investors are becoming less impressed by growth alone and more concerned about long-term execution risks, geopolitical exposure, and rising financial commitments tied to the ongoing infrastructure race.

Buybacks Offer Support but Do Not Remove Risks

NVIDIA returned roughly $20 billion to shareholders through buybacks and dividends during the quarter. The company also approved an additional $80 billion share repurchase authorization with no expiration date, signaling confidence in future cash generation.

The quarterly dividend was also increased to $0.25 per share, reflecting a more aggressive capital return strategy.

Even so, the latest pullback highlights that investor expectations remain extremely high, leaving little room for geopolitical setbacks, cost overruns, or slower-than-expected infrastructure demand going forward.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts