AVGO Stock Risks Breakdown Under $400 Post Broadcom Earnings on the AI Guidance Shortfall

Following earnings, investors' record-breaking rise abruptly stopped as they became more concerned about the sustainability of enormous infrastructure investment, increased geopolitical risks, and poor AI forecasts.

Quick overview

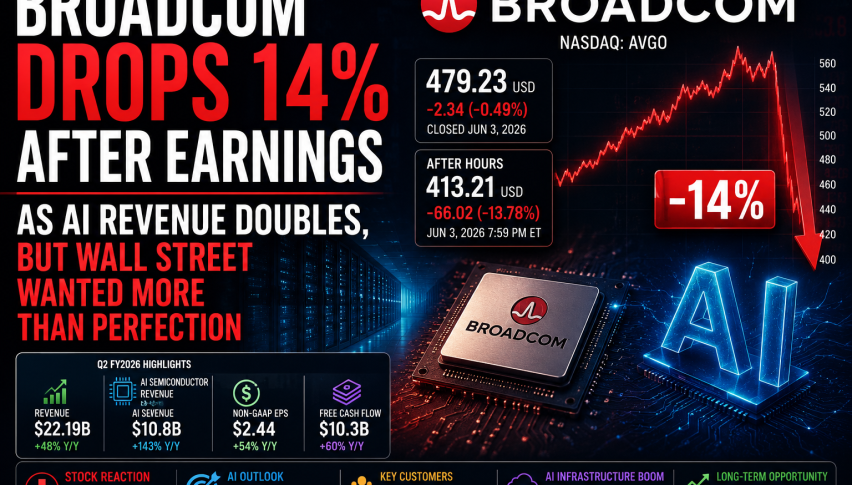

- Broadcom's shares fell approximately 15% in premarket trading after disappointing AI revenue guidance, despite exceeding fiscal second-quarter earnings expectations.

- The company's forecast of $16 billion in AI-related revenue for the third quarter fell short of analyst expectations, leading to widespread profit-taking.

- Concerns over U.S.-China technology tensions and financing challenges for OpenAI have added pressure on Broadcom's outlook and investor sentiment.

- Despite strong partnerships in the AI ecosystem, the selloff highlights growing investor caution regarding valuation and future growth sustainability.

Following earnings, investors’ record-breaking rise abruptly stopped as they became more concerned about the sustainability of enormous infrastructure investment, increased geopolitical risks, and poor AI forecasts.

Broadcom Suffers Sharp Selloff After Earnings

Shares of Broadcom plunged roughly 15% in premarket trading, falling to around $403 after closing at a record high near $495 the previous day. The sharp decline came despite the company reporting fiscal second-quarter results that exceeded Wall Street expectations.

The market reaction highlighted a growing disconnect between strong current performance and increasingly demanding investor expectations. While Broadcom continues to benefit from the global expansion of AI infrastructure, investors were disappointed that management failed to deliver the type of guidance increase many had anticipated after the stock’s powerful rally.

The selloff suggests that expectations had risen far beyond reported results, leaving little room for anything short of exceptional forward projections.

AI Revenue Outlook Disappoints Investors and AI Itself

The primary source of concern was Broadcom’s guidance for third-quarter AI revenue.

Management forecast approximately $16 billion in AI-related revenue for the quarter, below analyst expectations of roughly $17.3 billion. In addition, the company reiterated its fiscal 2027 AI revenue target of more than $100 billion rather than raising the outlook.

While those figures remain impressive by historical standards, investors had increasingly priced in even stronger growth assumptions. As a result, the lack of an upward revision triggered widespread profit-taking across the stock.

Analysts noted that supply limitations rather than demand weakness remain the key constraint. However, for investors who had anticipated accelerating guidance revisions, that distinction provided little reassurance.

Technical Analysis – The Lower Highs Continue

Broadcom entered the new year on uncertain footing, with its share price dipping below $300 as confidence across the semiconductor complex began to fray. But we saw a strong surge inn April and after a consolidation above the 20 daily SMA for a few weeks, AVGO stock resumed the uptrend last week and approached $500 on Wednesday before reversing down and falling to $400 lows. This is the previous high from December 2025, which is offering support. Although we might see a deeper retreat if the support zone around $400 breaks.

AVGO Chart Daily – Returning Above the 100 SMA

However we saw a strong rebound after the earnings, taking the stock to $406.83, but buyers couldn’t push the AVGO stock price to a new record high and today it fell under $400. Although buyers returned this week and pushed AVGO to a new record above $442 on Thursday, but has made a swift reversal on Friday and will be testing the 20 SMA at $400 again next week, so we will see if it holds.

Broadcom Q1 Earnings Report

-

- Revenue: $22.19 billion, 48% year-over-year growth

- Earnings: Adjusted $2.44 per share vs. $2.39 expected

- Semiconductor Solutions: $15.01 billion

- Infrastructure Software: ($7.18 billion

- AI Revenue: ($10.8 billion, 143% increase year-over-year

Forward Guidance & Analyst Sentiment

China Risks Continue to Cloud the Outlook

Beyond earnings, concerns surrounding U.S.-China technology tensions continue to weigh heavily on semiconductor stocks.

Washington has steadily tightened restrictions on advanced semiconductor exports to China, while Beijing continues investing aggressively in domestic alternatives. This trend threatens to reshape one of the industry’s most important markets over the coming decade.

China remains a major source of demand for AI infrastructure, cloud computing, and data-center expansion. Continued export restrictions could reduce future growth opportunities for American chipmakers while accelerating the development of competing domestic technologies.

Investor optimism that semiconductor-related tensions might ease has faded considerably, contributing to renewed caution across the sector.

OpenAI Financing Questions Add New Pressure

Additional concerns emerged following reports that OpenAI is facing challenges securing approximately $18 billion in financing linked to a custom chip initiative involving Broadcom.

The project was designed to support the development of proprietary AI accelerators and reduce dependence on competing hardware suppliers. However, financing uncertainty has raised broader questions about whether the industry’s ambitious infrastructure plans can be supported indefinitely.

Investors are increasingly concerned that AI spending commitments across the technology sector may be expanding faster than monetization opportunities. If economic conditions weaken or returns arrive more slowly than expected, some large-scale projects could face delays or restructuring.

Strong Partnerships Fail to Offset Growing Concerns

Despite the selloff, Broadcom remains deeply integrated into the AI ecosystem through relationships with major technology firms, including Alphabet, Meta Platforms, Microsoft Corporation, and Anthropic.

These partnerships provide significant long-term opportunities across custom chips, networking infrastructure, and cloud technologies. However, investors appear increasingly focused on risks rather than strategic advantages.

Valuation Becomes the Central Concern

The sharp decline underscores a broader market concern: valuation. Following a massive run higher, Broadcom entered earnings trading at levels that assumed years of uninterrupted AI-driven growth.

As competition intensifies, export restrictions expand, and infrastructure spending requirements continue to climb, investors are becoming less willing to overlook potential obstacles. Even strong earnings were not enough to justify expectations that had become exceptionally elevated.

For now, Broadcom remains a critical player in the AI infrastructure buildout, but the latest selloff demonstrates how quickly sentiment can shift when growth forecasts fail to keep pace with investor optimism.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts