AMD Stock Rockets 14% as Agentic AI Catalyst and Intel Read-Through Fuel Breakout

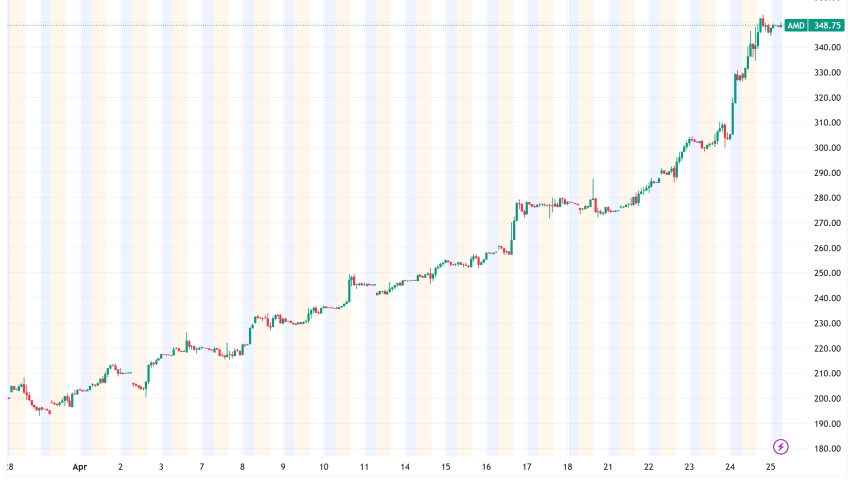

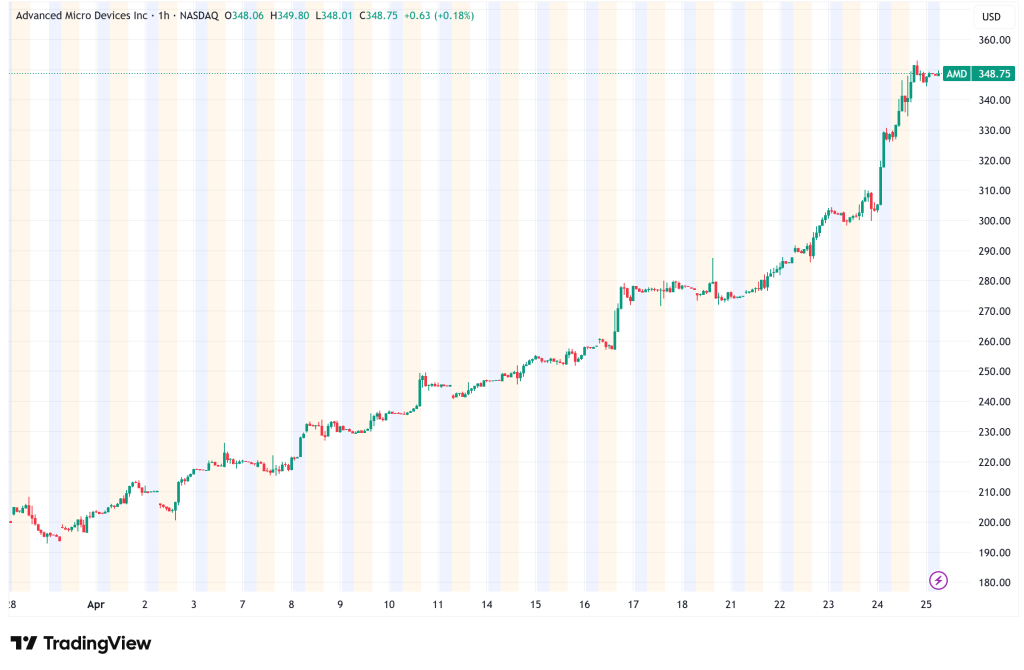

On April 24, shares of Advanced Micro Devices (NASDAQ: AMD) rose more than 13%, ending at $347.81, which is close to its 52-week high $353

Quick overview

- On April 24, AMD shares surged over 13% to $347.81, nearing its 52-week high, following a rating upgrade from Wall Street and positive sentiment from Intel's earnings report.

- Analyst Gil Luria raised AMD's price target from $220 to $375, citing a structural increase in CPU demand driven by the rapid deployment of agentic AI.

- AMD reported a 34% year-over-year sales increase in Q4 2025, with significant revenue growth from data centers and ambitious plans for AI expansion.

- Despite the optimism, concerns remain about AMD's high valuation and insider selling, alongside potential supply chain issues affecting revenue growth.

On April 24, shares of Advanced Micro Devices (NASDAQ: AMD) rose more than 13%, ending at $347.81, which is close to its 52-week high of $353. This was because Wall Street raised its rating and Intel’s earnings report gave investors a positive read-through for the AI chip trade.

D.A. Davidson analyst Gil Luria started the surge by raising his price target for AMD from $220 to $375 and changing his rating from Neutral to Buy. Luria’s main point is that there is a “structural increase” in CPU demand because agentic AI is being deployed quickly. Agentic AI is autonomous AI systems that need a lot of server-grade processors to work. His statement was clear: AMD is “well positioned to significantly raise prices across the portfolio” since demand will soon outstrip supply.

Intel’s Blowout Becomes AMD’s Tailwind

The improvement came out at the same time as Intel’s earnings report on Thursday, which was far better than expected and propelled Intel shares up 23%. It was evident to AMD investors that if Intel is seeing a huge rise in demand for data center CPUs, AMD, which has been steadily acquiring market share from Intel in the server CPU market for years, is likely in an even better position to benefit.

The foundations of AMD itself back up that hope. In the fourth quarter of 2025, the corporation made $10.3 billion in sales, a 34% increase over the year before. Revenue from data centers alone was $5.4 billion, net income rose 42% to $2.5 billion, and free cash flow almost doubled to $2.1 billion. During the results call, CEO Lisa Su talked about an ambitious plan for AI growth. This plan includes a multi-gigawatt GPU deal with OpenAI and intends to ramp up its next-generation MI450 GPU series in the second half of 2026. Su has also said again that the goal is to make tens of billions of dollars in AI revenue from data centers by 2027.

AMD’s MI450 Catalyst

Analysts think that the market could not be giving AMD’s impending MI450 launch and Helios rack-scale solutions enough credit for how much money they could make. AMD is in a rare position right now: TSMC is expected to significantly increase AMD chip output, which could lead to triple-digit revenue growth in the first quarters after the launch. This is because NVIDIA’s AI GPUs are mostly sold out and TSMC is having trouble ramping up production of Nvidia chips.

76% of the 40 analysts that MarketBeat follows who cover AMD give it a Buy or Strong Buy rating. The average price target has gone up more than 100% over the past 12 months. Analysts’ highest forecasts now exceed $380, which means a rise of almost 35% from where the stock is presently. However, some bulls say that even that could be too low if AMD’s Q1 2026 earnings, which come out on May 5, show fresh MI450 orders.

A Note of Caution on AMD Stock

Not everyone is in a hurry. On April 26, Cathie Wood’s ARK Investment Management sold about 215,643 AMD shares for about $75 million. This was after the stock rose almost 25% in just one week. GuruFocus says that AMD is very expensive compared to its own fair value calculation. The stock’s price-to-earnings ratio of 131x is substantially above its five-year median.

Insider selling has also reached around $64 million in the last three months. Some investors may see this as a warning from people who know the company best. There are still serious risks to AMD’s revenue growth because of problems in the supply chain, especially with high-bandwidth memory (HBM) chips that are said to be sold out until next year.

AMD is at a crossroads right now, with Q1 reports just a few days away. The stock has broken out technically, and analysts are becoming more confident in it, but the price is so high that there isn’t much space for disappointment.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts