Paramount Skydance Gains Regulatory Momentum as $111 Billion Warner Bros Deal Nears Finish Line

PSKY stock: Paramount Skydance advances $111B Warner Bros deal as DOJ approval boosts merger prospects amid streaming consolidation.

Written by:

Arslan Butt•Monday, June 15, 2026•4 min read

•Last updated: Monday, June 15, 2026

Quick overview

Paramount Skydance's proposed $111 billion acquisition of Warner Bros. Discovery has gained attention following DOJ approval, marking a significant regulatory milestone.

The merger aims to create a major media and streaming platform, uniting several well-known brands under one corporate structure.

Despite the approval, ongoing reviews by various regulatory bodies pose risks to the completion of the deal.

The long-term success of Paramount Skydance hinges on effective integration and execution of the merger amidst challenges in the competitive streaming landscape.

Paramount Skydance (NASDAQ: PSKY) is emerging as one of the most closely watched media stocks as investors assess the implications of its proposed $111 billion acquisition of Warner Bros. Discovery.

The stock has largely traded sideways near $10.50 in recent weeks. However, the latest regulatory developments could become a significant catalyst as the company seeks to create one of the world’s largest media and streaming platforms.

While Wall Street remains focused on AI and technology stocks, Paramount Skydance represents a different type of transformation story: industry consolidation in a rapidly evolving entertainment landscape.

DOJ Approval Marks Major Milestone in Paramount’s WB Acquisition

The biggest recent development came when the U.S. Department of Justice cleared Paramount Skydance’s proposed acquisition of Warner Bros. Discovery following an extensive eight-month review. The DOJ concluded the transaction was unlikely to harm competition across streaming, linear television, or theatrical film distribution.

The approval removes one of the most significant regulatory hurdles facing the transaction.

If completed, the deal would unite:

Paramount Pictures

Warner Bros.

CBS

CNN

HBO Max

Paramount+

Showtime

Nickelodeon

DC Studios

New Line Cinema

under a single corporate structure.

Supporters argue the combined company would possess the scale necessary to compete more effectively against streaming giants such as:

The DOJ specifically noted that combining HBO Max, Discovery+, and Paramount+ could create a stronger competitor within the streaming ecosystem.

Remaining Regulatory Risks

Despite the DOJ clearance, investors should not assume the deal is complete.

Several reviews remain ongoing:

U.S. Federal Communications Commission (FCC)

European Commission

UK Competition and Markets Authority (CMA)

Various U.S. state attorney general offices

California and New York have reportedly continued examining the transaction amid concerns about media concentration, employment impacts, and creative diversity.

The companies are targeting a third-quarter closing.

Importantly, the merger agreement reportedly includes a substantial breakup fee and shareholder compensation provisions if deadlines are missed, increasing pressure on management to secure remaining approvals.

Paramount’s Fundamentals: A Scale Play in a Difficult Industry

The merger reflects a broader reality confronting traditional media companies.

Streaming competition has intensified dramatically over the past decade.

Key challenges include:

Rising content costs

Subscriber acquisition expenses

Cord-cutting pressure

Declining linear television revenue

Competition from technology platforms

Paramount Skydance is betting that scale provides the answer.

Potential benefits include:

Cost Synergies

Management expects billions in savings through:

Content optimization

Marketing efficiencies

Technology integration

Corporate overhead reductions

Streaming Strength

The combined streaming operation would control:

HBO franchises

Warner Bros. film library

Paramount content portfolio

CBS programming

Discovery brands

This could improve customer retention and reduce content acquisition costs.

Advertising Reach

A combined entity would possess one of the largest advertising footprints in global media.

Should you buy Paramount stock before Warner Bros’ acquisition?

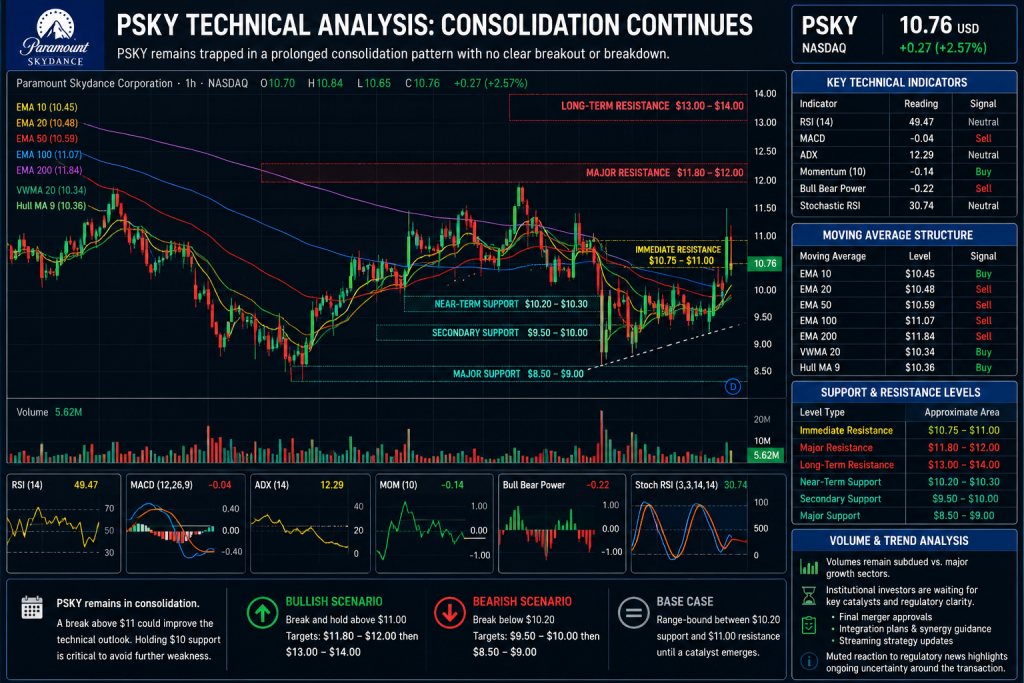

PSKY Technical Analysis: Ongoing Consolidation

From a technical perspective, PSKY remains locked in a prolonged consolidation pattern, showing neither bullish momentum nor signs of a major breakdown.

MACD at -0.04 (Sell): Minor negative bias, but lacks directional strength.

ADX at 12.29 (Neutral): Extremely weak trend strength; a reading below 15 confirms no active trend.

Momentum (10) at -0.14 (Buy): Flatlining near zero; buyers and sellers remain in equilibrium.

Stochastic RSI at 30.74 (Neutral): Approaching oversold territory but lacks a definitive reversal trigger.

Moving Average Structure

EMA 10 / VWMA 20 / Hull MA at $10.34 – $10.45 (Buy): Short-term averages and volume-weighted support provide a minor near-term floor.

EMA 20 / EMA 50 at $10.48 – $10.59 (Sell): Immediate overhead resistance keeps price action tightly capped.

EMA 100 / EMA 200 at $11.07 – $11.84 (Sell): Long-term averages bias the broader structure downward, confirming heavy overhead supply.

PSKY is trading near its short-term averages and slightly above volume-weighted support, but remains pinned below major long-term averages (including the 200-day EMA). This compression heavily favors continued consolidation over a new trend.

Support and Resistance Levels

Level Type

Approximate Area

Immediate Resistance

$10.75-$11.00

Major Resistance

$11.80-$12.00

Long-Term Resistance

$13.00-$14.00

Near-Term Support

$10.20-$10.30

Secondary Support

$9.50-$10.00

Major Support

$8.50-$9.00

A sustained move above $11 could improve the technical outlook significantly.

Failure to hold the $10 region could prolong the consolidation phase.

Volume and Trend Analysis

Trading volumes remain relatively subdued compared with major growth sectors.

Institutional investors appear to be waiting for:

Final merger approvals

Integration plans

Synergy guidance

Streaming strategy updates

The stock’s muted reaction to major regulatory news highlights ongoing uncertainty surrounding the ultimate outcome of the transaction.

Is Paramount (PSKY) a Good Long-Term Investment?

The long-term thesis depends largely on successful execution of the Warner Bros. Discovery acquisition.

Bull Case

The bullish argument centers on:

Massive content library

Strong streaming portfolio

Cost synergies

Enhanced advertising scale

Improved competitive position versus Netflix and Disney

If management executes effectively, the combined company could become one of the dominant global media platforms.

Bear Case

Risks remain substantial:

Integration complexity

Regulatory delays

Workforce reductions

Streaming profitability challenges

Debt burdens associated with large-scale consolidation

Critics within Hollywood have also argued the merger could reduce creative diversity and industry competition.

What Should PSKY Traders Watch Nex

Paramount Skydance is transitioning from a legacy media turnaround story into a merger-driven transformation play.

The DOJ’s approval significantly improves the probability of completing the Warner Bros. Discovery acquisition, but key regulatory reviews remain outstanding.

Technically, the stock remains stuck in consolidation, reflecting investor caution.

For long-term investors, the opportunity revolves around whether David Ellison can successfully integrate two of Hollywood’s most valuable content libraries and create a genuine streaming competitor capable of challenging industry leaders.

The merger may ultimately reshape the global entertainment landscape. The next several months will determine whether that vision becomes reality.

Lead Markets Analyst – Multi-Asset (FX, Commodities, Crypto)

Arslan Butt serves as the Lead Commodities and Indices Analyst, bringing a wealth of expertise to the field. With an MBA in Behavioral Finance and active progress towards a Ph.D., Arslan possesses a deep understanding of market dynamics.

His professional journey includes a significant role as a senior analyst at a leading brokerage firm, complementing his extensive experience as a market analyst and day trader. Adept in educating others, Arslan has a commendable track record as an instructor and public speaker.

His incisive analyses, particularly within the realms of cryptocurrency and forex markets, are showcased across esteemed financial publications such as ForexCrunch, InsideBitcoins, and EconomyWatch, solidifying his reputation in the financial community.