Biden’s Call for More Oil Ahead of US Midterms, Helping the Downtrend

The upside momentum ended in Oil and this week we have been seeing sellers come back, with the US Biden admin helping along

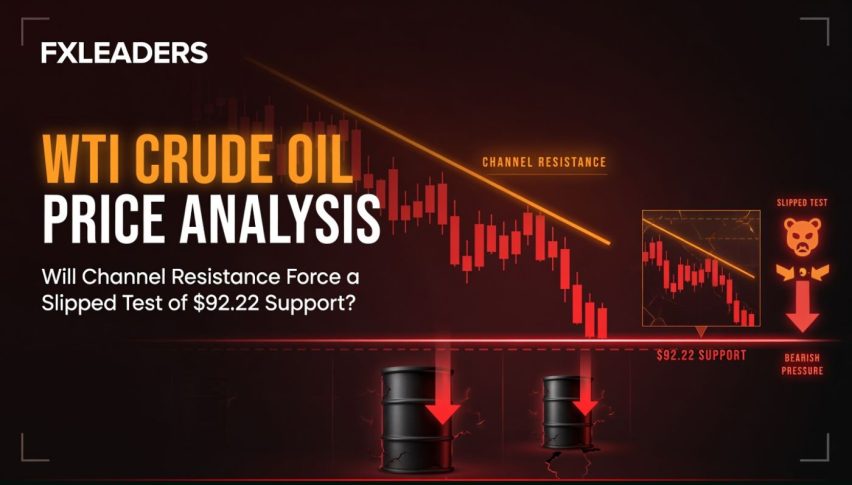

WTI Crude Oil made quite a comeback last week after a steep decline since June on global recession fears, gaining nearly $20 during that move. The 100 SMA (green) held as support on the weekly chart and the establishment cheered for higher Oil prices. But, the climb ended at the 50 SMA and the hawkish comments from the FED and the ECB on rate hikes are keeping the sentiment negative, indicating the upcoming recession as central banks continue to tighten the economy.

WTI Oil Weekly Chart – The 50 SMA Rejected the Price

The 100 SMA will probably be broken this time

The midterm elections in the US are another factor for the decline, since the current Biden administration wants cheaper prices as a small bonus to the US electorate. Oil took a dive yesterday and the selling accelerated after PPI report which was stronger than expected, with some broad USD strength and that’s also a time when liquidity in the Oil market was improving.

After the dip in prices, this was an interesting comment from deputy Treasury Secretary Wally Adeyemo:

The President wants more investment in hydrocarbons. He’s called for it. We’re seeing more of it. Right now we’re on pace — in 2023 — to have the largest level of production in history. We want to do more. What the President has said to the Secretary of Energy is that if there are any good ideas out there that are coming from the industry, please bring them forward because we want to produce more.

The industry wanted to build Keystone XL. Maybe bring that back rather than dropping sanctions on Venezuela? Besides that, OPEC on Wednesday cut its 2022 forecast for growth in world oil demand for a fourth time since April and also trimmed next year’s figure, citing slowing economies, the resurgence of China’s COVID-19 containment measures and high inflation.

Oil demand will increase by 2.64 million barrels per day (bpd) or 2.7% in 2022, the Organization of the Petroleum Exporting Countries (OPEC) said in a monthly report, down 460,000 bpd from the previous forecast. The lower demand outlook gives additional context for last week’s move by OPEC and its allies, known as OPEC+, to make their largest cut in output since 2020 to support the market. The United States criticized the decision.

US WTI Crude Oil Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts