AMD Stock Slides as OpenAI Costs Shake the AI Bubble, but $300 Zone Holds

Advanced Micro Devices is facing renewed pressure as concerns around OpenAI spending plans and stretched valuations weigh on sentiment.

Quick overview

- Advanced Micro Devices (AMD) is experiencing pressure due to concerns over OpenAI's spending plans and high valuations.

- After a significant rally that peaked above $350, AMD shares have fallen back to around $310, indicating a shift in market sentiment.

- Analyst downgrades and rising costs in AI infrastructure spending have raised questions about future demand in the semiconductor sector.

- The upcoming earnings release poses a risk for AMD, as any results below expectations could lead to further declines in share price.

Advanced Micro Devices is facing renewed pressure as concerns around OpenAI spending plans and stretched valuations weigh on sentiment.

Rally Loses Momentum After Sharp Surge

Shares of Advanced Micro Devices have come under pressure after an aggressive rally that pushed the stock above $350 last week. The momentum proved short-lived, with shares falling back to around $310, highlighting how quickly sentiment can shift when expectations are elevated.

The earlier surge was fueled by optimism across the semiconductor sector, but the rapid pace of gains left the stock vulnerable to even modest negative developments.

OpenAI Spending Outlook Raises Questions

A key overhang for the sector has emerged from updated expectations around OpenAI. While the company has outlined ambitious long-term plans—including potential advertising revenue growth and massive investments in computing infrastructure—these projections have also sparked debate.

Reports pointing to rising costs, tighter budget scrutiny, and questions around the pace of AI infrastructure spending have introduced uncertainty. With figures suggesting up to $600 billion in computing investment through 2030, investors are now questioning whether demand will scale as quickly as markets have priced in.

Analyst Downgrade Adds to Pressure

Further weighing on sentiment, Northland Securities issued a more cautious view on AMD, maintaining a neutral stance while signaling limited upside from current levels.

This reflects a broader shift in the market narrative, where high-growth expectations are being tested against valuation realities. After a strong run, AMD is increasingly viewed as priced for near-perfect execution.

Share Price Reacts Swiftly

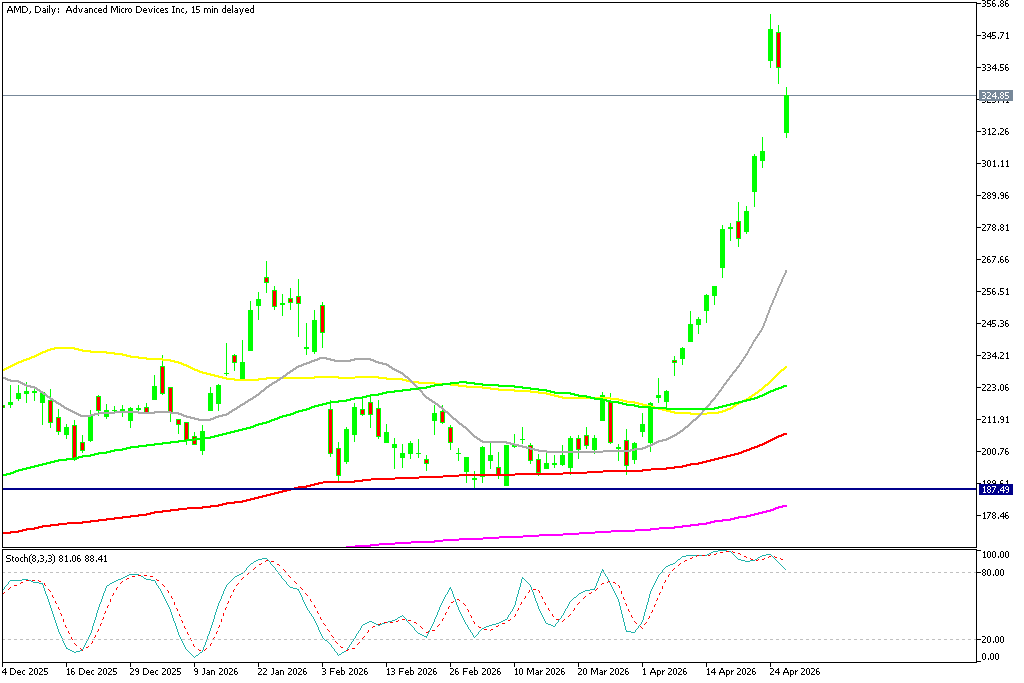

Following the earnings release, AMD shares fell sharply, sliding roughly 20% in January and pushing the stock below the $200 level. But the 100 SMA (red) acted as support on the daily chart. The price moved above and below $200 many times so the market was trying to decide which way to go, but decided on the upside in late March, breaking above the 50 daily SMA (yellow) and reaching a new record high of $353 late last week. However, the stock has reversed this week, but AMD is holding above $300 nonetheless.

AMD Chart Daily – Rebounding Off the 100 SMA

AI Demand Narrative Faces Scrutiny

Although AI remains a powerful long-term driver, the near-term outlook is becoming less certain. Semiconductor peers including NVIDIA, Broadcom, and Intel also moved lower, suggesting broader concerns across the sector.

As AI demand evolves beyond GPUs into more diverse workloads, growth may become less explosive and more incremental—challenging the market’s current assumptions.

High Expectations Leave Little Margin for Error

While AMD continues to build strategic partnerships and expand its role in AI infrastructure, investor focus is shifting toward execution and near-term results.

At current valuation levels, even small disappointments—whether from slowing demand, delayed spending, or weaker earnings—could trigger outsized reactions. The recent pullback suggests that the market is beginning to reassess just how much of the AI boom is already priced into the stock.

Earnings Loom as a Critical Test

The upcoming earnings release now carries heightened risk. With expectations elevated, anything short of exceptional results could trigger further downside.

Meanwhile, competition from NVIDIA remains intense, and AMD’s ability to deliver on its roadmap is far from guaranteed. After a steep rally and an early pullback, the stock’s volatility is becoming harder to ignore—suggesting that the recent surge may have been more hype than substance.

AMD Q4 2025 Earnings Overview

Headline Results

- EPS (Non-GAAP): $1.53, beating consensus by $0.21

- Revenue: $10.3 billion, exceeding expectations by $630 million

- Market Reaction: Shares declined post-earnings despite the beat

Market Position

- Market Capitalization: ~$394.2 billion

- Exchange / Sector: NASDAQ-listed, leading semiconductor designer

- Context: Results highlight strong execution, but expectations remain elevated

Financial Health Snapshot

- Revenue Growth (3Y): 5.6%, indicating steady expansion

Profitability:

- Net margin: 10.32%

- Gross margin: 48.26%

Balance Sheet:

- Current ratio: 2.31

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts