Will Apple (AAPL) Stock Break Above $317 or Is Hedgeye’s 23% Downside Call a Warning?

Apple stock AAPL nears record highs as Broadcom deal lifts supply confidence, but Hedgeye sees 23% downside risk.

Quick overview

- Apple shares are nearing record highs due to strong earnings expectations and a new multi-year deal with Broadcom.

- However, valuation concerns and a bearish short call from Hedgeye suggest potential downside risks of about 23%.

- Analysts are cautious as growth expectations for services and iPhone demand may be overly optimistic, especially in light of competition from Huawei.

- Technical indicators show a bullish trend, but the stock is approaching overbought territory, raising questions about sustainability.

Apple shares are trading near record highs after fresh supply-chain confidence from the Broadcom deal, but valuation concerns, insider selling, and a new Hedgeye short call are testing the rally.

Apple Pushes Toward Record Highs

Apple shares are once again pressing near record highs as investors reward the company’s supply-chain strategy, strong earnings expectations, and resilient iPhone demand. However, the rally is now facing a sharper debate as bearish analysts question whether current growth expectations are too optimistic.

Hedgeye Warns of 23% Downside

Hedgeye initiated a short call on Apple, arguing that the stock could fall by about 23%.

Analyst Felix Wang cited concerns that Apple’s previous advantage in beating revenue expectations may be fading as Wall Street forecasts have already been revised higher. Hedgeye also warned that double-digit growth expectations for FY2027 and FY2028 may be too aggressive, especially if Huawei gains more traction in China.

Valuation is the other major concern. Apple trades near 34x forward earnings and has a trailing P/E near 37.6x, well above historical norms. That leaves little room for disappointment if services growth, iPhone demand, or China sales soften.

Broadcom Deal Adds Supply-Chain Support for Apple

The bullish side of the Apple story received support from the company’s new multi-year Broadcom agreement.

Apple committed more than $30 billion to Broadcom for custom silicon components and wireless connectivity technologies. The deal runs through 2031 and is expected to support production of more than 15 billion U.S.-made chips.

Broadcom will also expand and modernize its Fort Collins, Colorado facility with a $1.5 billion investment.

For Apple, the deal helps secure critical wireless and custom silicon components while reinforcing its U.S. manufacturing strategy. It also reduces supply-chain uncertainty ahead of future iPhone, Mac, and AI infrastructure cycles.

AAPL’s Earnings Expectations Remain High

Apple is expected to report Q3 2026 earnings on July 30.

Analysts expect EPS of $1.88, up nearly 20% from the year-ago quarter. For fiscal 2026, EPS is projected near $8.74, representing roughly 17% growth from fiscal 2025.

Apple has beaten EPS estimates in each of its last four quarters. The company’s Q2 revenue reached $111.2 billion, while adjusted EPS came in at $2.01, both above Wall Street expectations.

Still, the bar is now high. Apple’s average analyst price target is near $315, meaning the stock is already trading around consensus fair value.

App Store and China Demand Send Mixed Signals

UBS estimates Apple’s June-quarter App Store growth was roughly 3%, with U.S. App Store revenue down about 6%.

That suggests services growth remains positive, but not explosive. UBS maintained a Neutral rating and a $296 price target, signaling caution at current levels.

In China, Jefferies noted that post-618 discounting helped drive stronger iPhone volume, with recent fortnight sales reportedly up around 20%. However, the firm warned that some of that strength may depend on elevated trade-in values and promotions that may not be sustainable.

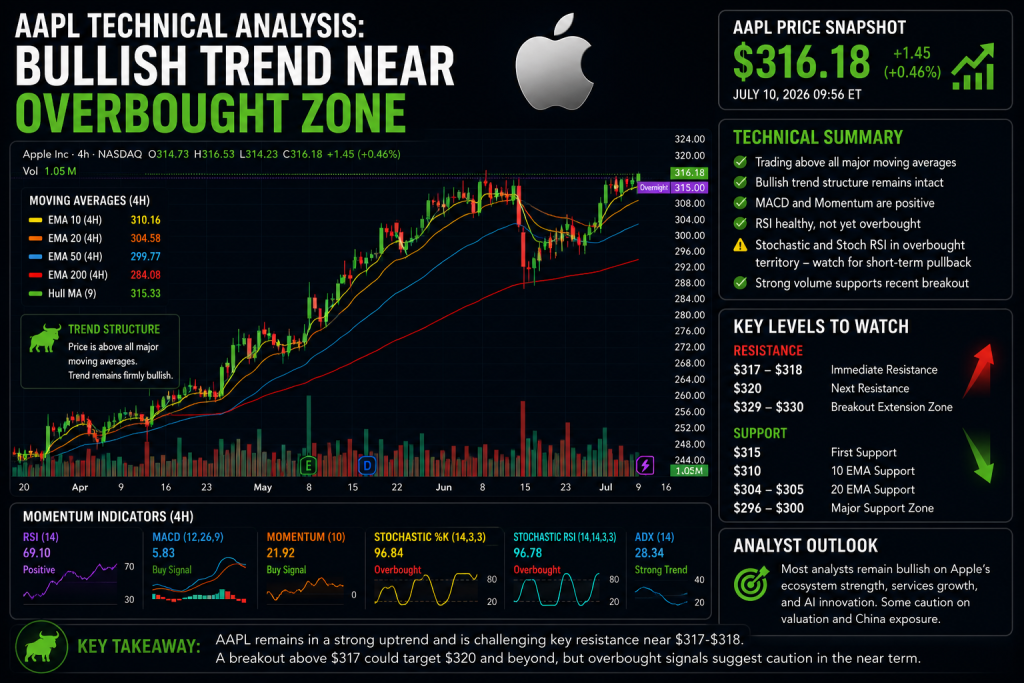

AAPL Technical Analysis: Bullish Trend Near Overbought Zone

From a technical perspective, Apple’s 4-hour chart remains firmly bullish.

AAPL is trading above all major moving averages, including the 10 EMA at $310.16, 20 EMA at $304.58, 50 EMA at $299.77, and 200 EMA at $284.08. The Hull Moving Average at $315.33 is also flashing a buy signal, showing near-term trend strength.

Momentum remains positive. MACD is on a buy signal at 5.83, while Momentum stands at 21.92. RSI sits at 69.10, just below overbought territory.

However, Stochastic %K at 96.84 and Stochastic RSI at 96.78 suggest the rally is stretched in the short term.

Key Levels: $317, $320 and $310

The immediate resistance zone is $317-$318, where Apple has recently struggled to break out.

A clean move above that level could open the door toward $320, followed by a possible extension into the $329-$330 zone.

On the downside, the first support is $315, followed by $310, where the 10 EMA sits. If AAPL breaks below $310, the next support zone is $304-$305, near the 20 EMA.

A deeper correction would bring $296-$300 back into focus, aligning with several analyst caution points.

Is Apple Stock Nearing a Breakout or Exhaustion?

Apple’s trend remains strong, supported by earnings momentum, supply-chain investment, and resilient demand. The Broadcom deal also strengthens the long-term hardware roadmap.

However, the stock is now pressing against record-high resistance while valuation concerns are rising. Hedgeye’s 23% downside call may not derail the rally on its own, but it highlights how much optimism is already priced in.

For now, bulls need a breakout above $317-$320 to keep momentum alive. If Apple fails there, the stock could consolidate toward $310 before earnings reset the narrative.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts