Will CRM Stock Fall Below $160 as Salesforce Agentforce Doubts Hit AI Software Bulls?

Salesforce stock CRM falls as KeyBanc questions Agentforce momentum, with $160 support and $165 resistance now key for bulls.

Quick overview

- Salesforce's stock dropped after KeyBanc downgraded it, citing slow adoption of Agentforce and customer data readiness issues.

- Investor concerns are growing that Salesforce's AI growth narrative is not translating into immediate revenue acceleration.

- Despite the downgrade, Salesforce's near-term earnings expectations remain steady, with projected EPS and revenue showing growth.

- The stock is considered undervalued, but the market is seeking proof of Agentforce's adoption and enterprise spending stability.

Salesforce shares dropped after KeyBanc downgraded the stock, warning that Agentforce adoption is slower than expected and customer data readiness remains a major obstacle.

Salesforce Slides as AI Growth Story Faces Scrutiny

Salesforce fell even as the broader market gained, highlighting investor concern that the company’s AI growth narrative is not translating quickly enough into measurable revenue acceleration.

KeyBanc Downgrade Pressures CRM

The main catalyst was KeyBanc’s downgrade of Salesforce to Sector Weight.

Analyst Jackson Ader said customer and CIO feedback did not support a bullish near-term view of Agentforce, Salesforce’s flagship AI agent platform. According to the firm, customers repeatedly highlighted two problems: their data is not ready for meaningful AI workflows, and Agentforce is not yet mature enough as a product.

That is a direct challenge to Salesforce’s AI story. If enterprise customers need more time to clean, organize, and govern data before deploying autonomous agents, revenue from Agentforce may take longer to arrive than bulls expected.

CIO Spending Signals Raise Concern

KeyBanc also said more CIOs expect to deprioritize Salesforce spending over the next 12 months than increase it.

That finding matters because Salesforce depends on large enterprise renewals, cross-selling, and platform expansion. If customers slow spending or delay AI-agent projects, Salesforce’s growth recovery could be pushed further out.

Partners are reportedly just beginning to convert Agentforce proofs of concept into pipeline opportunities, suggesting the product is still early in its commercialization cycle.

Salesforce’s Earnings Expectations Remain Solid

Despite the downgrade, Salesforce’s near-term earnings expectations are still steady.

Analysts expect the company to report EPS of $3.27, up about 12.4% year over year, with revenue projected at $11.3 billion, up roughly 10.4%. For the full year, consensus estimates point to EPS of $14.12 and revenue of $46.09 billion.

That suggests Salesforce remains profitable and growing, even if investors are less convinced that AI will quickly reaccelerate the business.

CRM’s Valuation Looks Cheap, But Market Wants Proof

Salesforce now trades at a forward P/E of roughly 11.8x, well below the broader internet software industry average.

Its PEG ratio near 0.76 also suggests the stock is inexpensive relative to expected earnings growth. This is why some Wall Street analysts remain constructive, with average price targets still well above current levels.

However, the market is demanding evidence. A cheap valuation alone may not be enough if Agentforce adoption disappoints or enterprise spending softens.

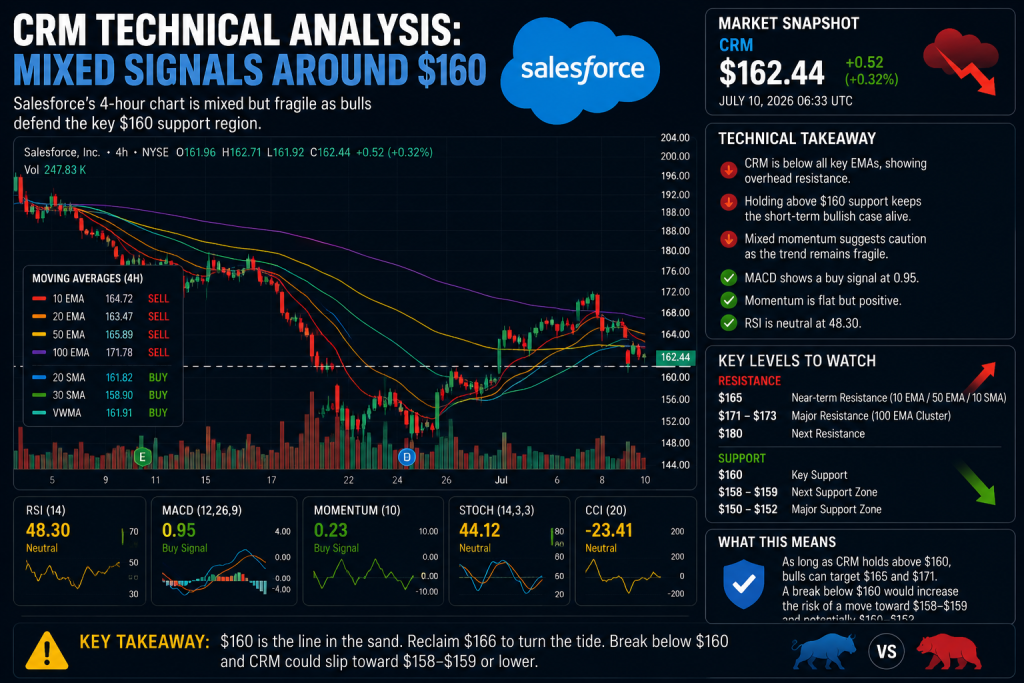

CRM Technical Analysis: Mixed Signals Around $160

From a technical perspective, Salesforce’s 4-hour chart is mixed but fragile.

CRM is trading below the 10 EMA at $164.72, 20 EMA at $163.47, 50 EMA at $165.89, and 100 EMA at $171.78, showing short-term resistance above the current price.

However, the stock remains slightly above the 20 SMA at $161.82, 30 SMA at $158.90, and VWMA at $161.91, meaning buyers are still trying to defend the $160 region.

Momentum is not decisively bearish. MACD shows a buy signal at 0.95, while Momentum also flashes buy despite sitting near flat. RSI is neutral at 48.30, suggesting room for either direction.

Key Levels: $160, $165 and $171

The first key support level is $160.

If CRM breaks below that area, the next downside zone sits near $158-$159, followed by a deeper risk toward $150-$152 if selling accelerates.

On the upside, buyers need to reclaim $164.70-$166, where the 10 EMA, 50 EMA, and 10 SMA cluster. A stronger rebound would require a break above $171-$173, where the 100-period moving averages sit.

Until CRM clears $166, the chart remains vulnerable to renewed selling.

Salesforce Is a Cheap Stock, with an Unproven AI Catalyst

Salesforce’s core business remains profitable, and valuation has compressed sharply after the stock’s steep year-to-date decline. That gives long-term bulls a reason to stay interested.

However, the AI catalyst is now under pressure. Agentforce must show clearer adoption, stronger pipeline conversion, and more visible revenue contribution before investors reward the stock with a higher multiple.

For now, $160 is the level bulls need to defend. A break below it could deepen the selloff, while a move back above $166 would suggest the downgrade-driven weakness is starting to fade.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts