TSM Stock Tests $420 Support as Record Revenue Fails to Ease AI Valuation Concerns

Taiwan Semiconductor TSM stock tests $420 before Q2 earnings as record revenue clashes with AI spending, valuation and technical pressure.

Quick overview

- Taiwan Semiconductor Manufacturing Company (TSMC) reported record June revenue of NT$442.68 billion, but shares fell as investors questioned the sustainability of AI-driven demand.

- Despite strong fundamentals, TSMC's elevated valuation and capital spending concerns are causing caution among investors ahead of its Q2 earnings report.

- The upcoming earnings report is critical for the semiconductor sector, as TSMC's performance will serve as a barometer for AI spending and overall market sentiment.

- Options market data indicates a cautious outlook, with traders hedging against potential downside following the earnings announcement.

Taiwan Semiconductor shares fell despite record June revenue as investors questioned whether AI-driven demand can keep justifying the stock’s elevated valuation.

TSMC Slides Ahead of Q2 Earnings as AI Sentiment Weakens

Taiwan Semiconductor Manufacturing Company delivered another strong revenue update, but the stock still came under pressure as investors grew more cautious ahead of Q2 earnings.

TSMC reported June revenue of NT$442.68 billion, equivalent to roughly $13.8 billion, representing a 68% increase from a year earlier. Total second-quarter revenue reached NT$1.27 trillion, slightly below some analyst estimates but still above the company’s own guidance.

The numbers confirm that demand for advanced semiconductors remains strong, especially from artificial intelligence, high-performance computing, 5G and smartphone customers.

However, the reaction in TSM stock shows that investors are no longer rewarding strong AI revenue automatically. After a powerful rally, the market is asking whether future demand can remain strong enough to justify high capital spending and elevated valuation multiples.

Q2 Earnings Become a Major AI Sector Test

TSMC reports second-quarter earnings on Thursday, July 16, and the results could influence sentiment across the entire semiconductor sector.

As the world’s largest dedicated chip foundry, TSMC sits at the center of the AI hardware supply chain. Nvidia, AMD, Apple and other major technology companies depend on TSMC’s advanced manufacturing and packaging capacity.

That makes the upcoming earnings report more than a company-specific event. Investors will use it as a real-time check on the health of AI spending.

Consensus expectations point to strong growth, with analysts looking for Q2 revenue around $39.6 billion and EPS near $3.80, up sharply from last year. But guidance may matter more than the headline numbers.

Markets will be watching whether management raises, maintains or softens its outlook for AI, high-performance computing, advanced packaging and capital expenditures.

Capital Spending Remains the Key Question

TSMC’s capital budget has become one of the most important signals for the AI trade.

Management previously guided 2026 capital spending toward the high end of its $52 billion to $56 billion range. That level of investment reflects confidence in long-term demand, but it also increases risk if AI spending slows.

TSMC must expand capacity before customers fully consume it. That works well when demand keeps rising, but it can pressure margins if growth slows or customers delay orders.

Investors will therefore be listening closely for comments on CoWoS advanced packaging, N2 ramp progress, overseas fab expansion and gross margin dilution.

In Q1, high-performance computing generated 61% of revenue, while smartphones accounted for 26%. If HPC and AI demand remain robust, TSMC’s growth case stays intact. But any cautious language around customer orders or capacity utilization could pressure the broader chip sector.

Valuation Concerns Weigh Despite Strong Fundamentals

TSMC remains one of the strongest companies in the semiconductor industry, but valuation concerns are rising.

GuruFocus data cited in the supplied notes shows TSM trading at a significant premium to estimated fair value, with a P/E ratio around 35x compared with a five-year median near 22.8x. The company’s GF Score of 97/100 reflects exceptional profitability, growth and financial strength, but its valuation score is much weaker.

That split explains the current market reaction.

Operationally, TSMC remains dominant. The company holds roughly 70% of the dedicated foundry market and continues to lead in advanced manufacturing. But after a strong rally, investors are increasingly debating whether the stock has already priced in too much AI optimism.

Options Market Signals Near-Term Caution

Options data also suggests investors are hedging ahead of earnings.

According to Barchart data cited in the supplied material, the put-to-call ratio for contracts expiring July 17 recently stood near 1.25x, indicating a more cautious near-term derivatives setup.

The lower price level on those contracts was around $410, suggesting traders are watching for possible downside after earnings if guidance fails to impress.

Wall Street sentiment remains broadly positive, with a Strong Buy consensus and an average target near $463. But in the short term, the stock may need more than strong revenue growth to break higher. Investors want confirmation that AI demand, margins and capital spending are all moving in the right direction.

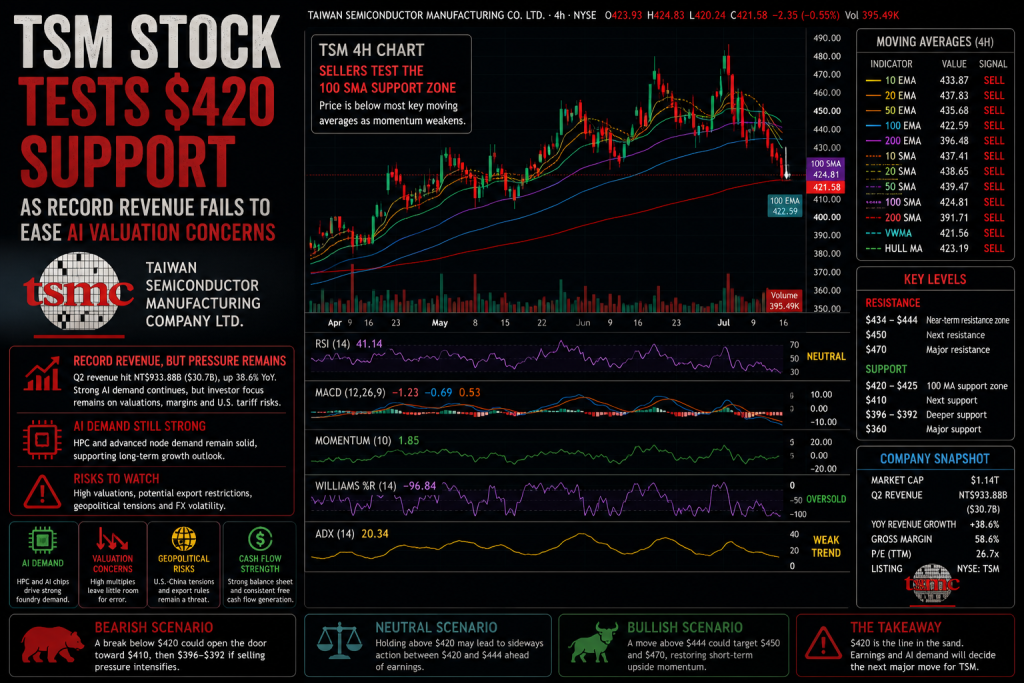

TSM Technical Analysis: $420 Becomes Immediate Support

TSM closed at $421.58 on July 13, down 2.89%, before recovering slightly to $422.98 in after-hours trading.

TSM Chart 4H – Sellers Test the 100 SMA Support Zone

The 4-hour chart shows that short-term momentum has weakened. TSM is trading below most major moving averages, including the 10-period EMA at $433.87, the 20-period EMA at $437.83 and the 50-period EMA at $435.68.

These levels now form a resistance band between roughly $434 and $444. A recovery above that zone would be needed to restore near-term bullish momentum.

The most important level is now the 100-period moving average area. The 100 EMA sits near $422.59, while the 100 SMA is around $424.81. TSM is trading right around this zone, making $420-$425 the key technical battleground before earnings.

If this support fails, sellers could target $410, which aligns with bearish options-market positioning. Below that, the next deeper support area sits near the 200-period EMA at $396.48 and the 200 SMA at $391.71.

Oscillators show selling pressure but not a confirmed breakdown. The RSI at 41.14 remains neutral, while Williams %R at -96.84 suggests the stock is near oversold territory. Momentum is flashing a buy signal, but MACD remains on sell, confirming mixed short-term conditions.

Taiwan Semiconductor Is a Strong Company, with a Demanding Setup

TSMC remains one of the clearest long-term beneficiaries of the AI infrastructure boom. Its leadership in advanced manufacturing, CoWoS packaging and next-generation process technology gives it a central role in the global semiconductor supply chain.

However, the stock is entering earnings with high expectations. Record revenue is no longer enough by itself. Investors want confidence that AI demand remains durable, capital spending will generate strong returns and margin dilution from overseas expansion and N2 ramp costs remains manageable.

For now, TSM stock remains vulnerable while trading below the $434-$444 resistance zone. Holding $420 would keep the broader technical structure intact, but a decisive break below that level could expose shares to $410 and then the 200-period moving average zone near $396.

A strong earnings report and confident AI outlook could help TSM retest $444 and move back toward $450. But if guidance disappoints, the recent pullback may deepen as investors continue reassessing AI valuations across the semiconductor sector.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts