SKHY ADR Tests $150 as SK Hynix Rout Raises Valuation Concerns After Nasdaq Debut

SK Hynix stock SKHY ADR holds near $152 as SK Hynix rout, ADR premium and HBM4 doubts pressure AI memory optimism.

Quick overview

- SK Hynix shares fell sharply after a strong Nasdaq debut as investors took profits and questioned AI memory valuations.

- The company's American Depositary Receipts (ADRs) opened at $170 but closed at $168.01, while local shares in Seoul dropped 15.4%.

- Concerns about high earnings expectations and a significant ADR premium are contributing to investor caution despite SK Hynix's strong fundamentals.

- The stock remains technically vulnerable, with critical support levels around $149-$150 that need to be maintained to avoid further declines.

SK Hynix shares plunged after their blockbuster Nasdaq debut as investors locked in profits and questioned whether AI memory optimism has already been priced in.

SK Hynix Slides After Nasdaq Debut as AI Memory Rally Faces Profit-Taking

SK Hynix’s long-awaited U.S. listing delivered a powerful first-day rally, but the enthusiasm faded almost immediately as investors moved to book gains.

The company priced its American Depositary Receipts at $149 before the Nasdaq listing. The ADRs opened near $170 and closed their debut session at $168.01, giving investors a gain of nearly 13% over the offer price.

However, the first full trading session brought a sharp reversal. SKHY fell toward the $152-$155 area, wiping out much of the debut rally while still holding slightly above its IPO price.

The move coincided with a much deeper selloff in Seoul, where SK Hynix’s local shares fell 15.4%, marking the stock’s worst one-day decline on record. Samsung Electronics also dropped sharply, dragging the KOSPI lower and triggering a market-wide trading halt.

Profit-Taking Meets AI Valuation Concerns

The selloff does not appear to reflect a new operating warning from SK Hynix. Instead, it looks like a combination of profit-taking, valuation pressure, index weakness and caution ahead of upcoming earnings.

SK Hynix had already delivered a massive rally before the Nasdaq debut, supported by its leadership in high-bandwidth memory chips used in AI accelerators. The company remains a critical supplier to Nvidia and other AI infrastructure customers, and its HBM market share has made it one of the clearest winners of the AI memory cycle.

But after such a large run, even strong fundamentals may not be enough.

Investors are now asking whether expectations have become too aggressive. Memory stocks often look cheap near peak earnings, only for profitability to compress when supply catches up with demand.

ADR Premium Adds Another Risk for U.S. Investors

A key issue is the valuation gap between SKHY and SK Hynix’s Seoul-listed shares.

Each SKHY ADR represents one-tenth of one Korean ordinary share. In theory, both securities provide exposure to the same company. In practice, ADRs can trade at a premium because they offer easier access for U.S. investors, deeper dollar liquidity and simpler settlement.

Following the Seoul rout, reports estimated the ADR premium at more than 20%, with Reuters citing a premium near 25.6% at one point.

That premium matters. Investors buying SKHY are not only buying SK Hynix’s memory cycle exposure; they may also be paying extra for U.S. market access. If that premium narrows, the ADR could underperform even if the underlying Korean shares stabilize.

HBM Strength Still Supports SK Hynix’s Long-Term Story

Despite the pullback, SK Hynix remains one of the most important beneficiaries of the AI infrastructure boom.

The company leads the high-bandwidth memory market, with Counterpoint data cited in the supplied notes showing SK Hynix held around 58% of HBM revenue share in the first quarter. HBM chips are essential for AI accelerators, where demand remains strong from Nvidia, hyperscalers and data center customers.

Management has also pushed back against oversupply fears. SK Hynix CEO Kwak Noh-jung has argued that the memory industry may face severe supply shortages in 2027, with demand continuing to exceed production capacity.

That keeps the bull case intact. If AI demand remains strong and HBM pricing holds, SK Hynix could continue generating exceptional margins.

SKHY Earnings Expectations May Be Too High

The problem is that expectations have risen sharply.

Analysts expect SK Hynix to report extraordinary Q2 results, with consensus estimates pointing to revenue above KRW 80 trillion and operating profit above KRW 60 trillion. Some forecasts imply operating margins in the mid-to-high 70% range.

However, some analysts have begun trimming estimates, partly due to uncertainty around HBM4 ramp timing and product mix. Korea Investment reportedly expects full-scale HBM4 production and sales to accelerate more meaningfully in Q3 rather than Q2.

That distinction matters because SK Hynix’s heavier HBM exposure may limit its ability to fully benefit from rising conventional DRAM prices, since HBM is often sold under longer-term agreements.

In other words, earnings can still be excellent and fall short of market expectations.

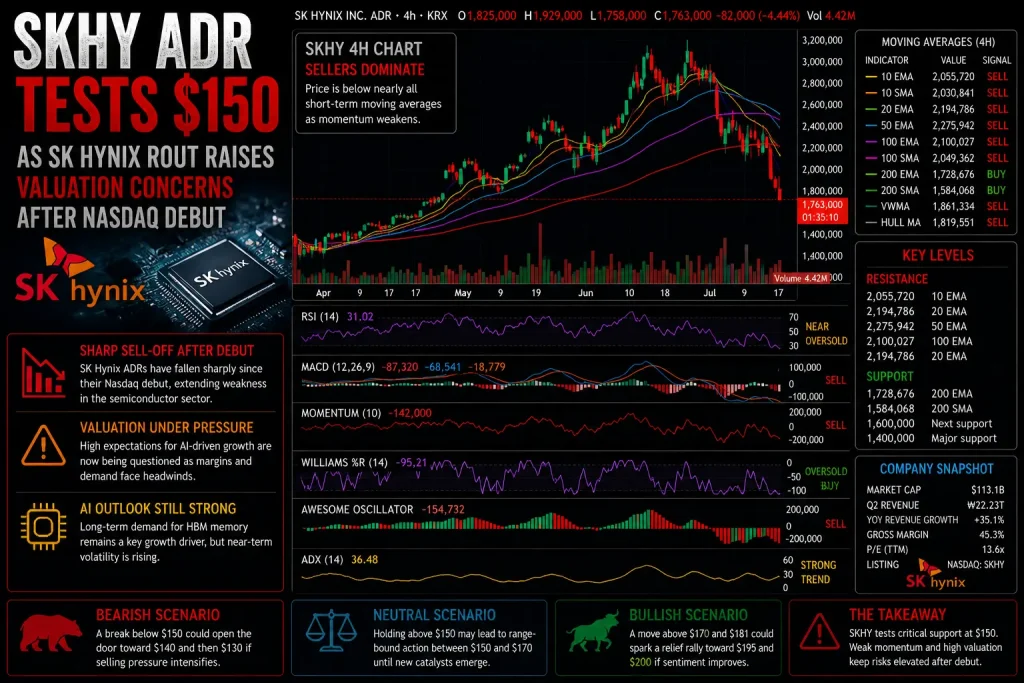

Technical Analysis: Seoul Shares Break Below Short-Term Averages

The 4-hour technical setup for SK Hynix’s Korea-listed shares remains weak after the sharp decline.

SK Hynix Chart 4H – Sellers Dominate Below Key Moving Averages

The stock is trading below nearly all short- and medium-term moving averages. The 10-period EMA stands near KRW 2,055,720, while the 20-period EMA sits around KRW 2,194,786. Both are above the current market and now act as resistance.

The 50-period EMA near KRW 2,275,942 and the 100-period EMA near KRW 2,100,027 also remain above price, confirming that the recent selloff has damaged short-term momentum.

The only major support signals come from the longer-term trend. The 200-period EMA near KRW 1,728,676 and the 200-period SMA near KRW 1,584,068 remain below the market, suggesting that the broader uptrend has not fully collapsed yet.

Oscillators show the stock is deeply stretched to the downside but not clearly reversing. RSI is near 31, close to oversold territory, while Williams %R at -95 is flashing a buy signal. However, MACD remains on sell and the Awesome Oscillator is negative, showing that bearish momentum has not yet fully faded.

SKHY Levels to Watch

For the U.S.-listed ADR, the first major level is the $149 offering price.

As long as SKHY holds above $149-$150, the debut structure remains technically intact. A break below that zone would be more damaging because it would signal that the ADR has fully surrendered its listing premium.

Below $149, sellers could target $145 and then $140 if broader chip weakness continues.

On the upside, buyers need to reclaim $157 first, followed by $162. A move back above $168 would be required to restore confidence in the post-listing rally. Until then, rebounds may be viewed as relief moves rather than a renewed breakout.

SK Hynix Is a Strong Company, But a Crowded Trade

SK Hynix remains a world-class memory chip leader with powerful exposure to AI infrastructure, HBM demand and Nvidia-linked supply chains. Its long-term growth story has not disappeared because of one sharp selloff.

However, the stock is now facing a more difficult setup. Investors are questioning the sustainability of peak memory margins, the pace of HBM4 ramp-up, future supply growth, and the large premium embedded in the new SKHY ADR.

The key issue is not whether SK Hynix is a strong company. It clearly is. The question is whether investors are paying too much for that strength after an explosive rally.

For now, SKHY remains vulnerable if it fails to hold the $149-$150 listing zone. A rebound above $162 would help stabilize sentiment, but until the ADR premium narrows or Q2 earnings confirm that expectations remain achievable, investors may continue treating rallies with caution.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts