GOOG Stock Jumps Above $260 on Strong Alphabet Results as Cloud Drives Growth

Alphabet Inc. surged after earnings as strong cloud growth offset lingering concerns over rising costs and aggressive tech spending.

Quick overview

- Alphabet Inc. shares surged in after-hours trading following a strong Q1 earnings report, with revenue reaching $109.9 billion, exceeding expectations.

- Google Cloud emerged as a key growth driver, generating $20.03 billion in revenue, reflecting over 60% year-over-year growth.

- Despite solid performance in advertising, YouTube's revenue slightly missed expectations, indicating potential moderation in that segment.

- Concerns remain about rising costs associated with infrastructure investments, which could impact future profitability.

Live GOOGL Chart

[[GOOGL-graph]]

Alphabet Inc. surged after earnings as strong cloud growth offset lingering concerns over rising costs and aggressive tech spending.

Strong Earnings Drive After-Hours Rally

Shares of Alphabet Inc. jumped sharply in after-hours trading, with the stock climbing to around $360 after closing at $347. The move followed a strong first-quarter report, where revenue reached $109.9 billion, comfortably beating expectations of $107.1 billion and marking roughly 22% year-over-year growth.

The results represent Alphabet’s fastest growth pace since 2022, reinforcing the company’s ability to deliver strong top-line performance even amid macro uncertainty.

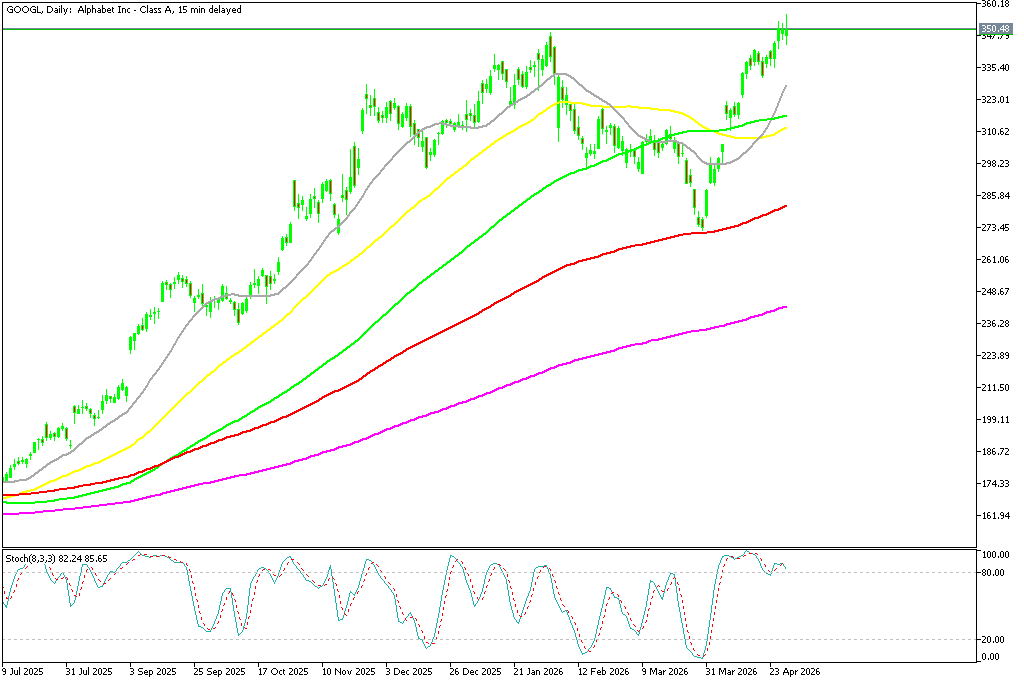

GOOGL Chart Daily – The 200 SMA Held As Support

Cloud Emerges as Key Growth Engine

The standout segment was Google Cloud, which generated $20.03 billion in revenue—well above forecasts and reflecting growth of more than 60% year over year. This surge highlights strong enterprise demand and improving conversion of its large backlog into recognized revenue.

The company’s recent acquisition of Wiz also adds to its cloud ambitions, though investors will be watching closely for signs of meaningful integration and returns from the deal.

Advertising Remains Resilient

Alphabet’s core advertising business also delivered solid results. Google Search revenue exceeded expectations, while total advertising revenue reached $77.25 billion, beating estimates.

These figures suggest that new search features and platform enhancements are helping maintain engagement and monetization, even as broader economic concerns persist.

However, YouTube advertising slightly missed expectations, indicating some moderation in growth within that segment.

Margins Hold Despite Heavy Spending

Operating income came in well above forecasts, easing fears that rising infrastructure spending would significantly compress margins. Capital expenditure remained high but slightly below expectations, suggesting a more measured rollout of investment plans.

This balance between growth and cost control addresses one of the key investor concerns: whether Alphabet can sustain profitability while pursuing one of the largest spending cycles in its history.

Caution Around Rising Costs

Despite the strong quarter, concerns remain around escalating expenses tied to next-generation infrastructure and long-term investments. These initiatives, often associated with overhyped automation trends, carry significant costs and uncertain returns.

While Alphabet’s results show it can manage these pressures for now, the sustainability of this balance will remain a key question for investors.

Alphabet Q1 Earnings Report

- Google beat Q1 revenue forecasts with $109.9bn, up from $90.2bn a year ago.

- Google Cloud surged to $20.03bn, well above the $18.41bn estimate.

- Operating income hit $39.7bn.

- EPS 2.82 (exp. 2.63),

- Raises dividend +5% to 0.22/shr

- Total revenue came in at $109.90bn, beating the $107.1bn consensus estimate and representing approximately 22% growth year-on-year from $90.2bn in Q1 2025

- Revenue excluding traffic acquisition costs reached $94.67bn versus a $91.57bn estimate

- Operating income of $39.70bn significantly exceeded the $36.19bn consensus forecast, pointing to margin leverage despite a heavy investment cycle

- Google Services revenue of $89.64bn topped estimates of $88.11bn, with Search and Other at $60.40bn versus a $59.08bn estimate

- Total Google advertising revenue of $77.25bn beat the $76.21bn estimate; YouTube ads were the sole miss at $9.88bn versus a $9.97bn estimate

- Google Cloud revenue of $20.03bn crushed the $18.41bn estimate, continuing the segment’s acceleration from $17.66bn in Q4 2025 and $12.26bn in Q1 2025

- Capital expenditure of $35.67bn came in marginally below the $36.39bn estimate, with full-year 2026 capex guidance of $175-185bn remaining in place

- The report follows Alphabet’s $32bn acquisition of cloud security firm Wiz, which closed on March 11 and is now integrated within Google Cloud

Outlook Balances Strength and Risk

Alphabet’s latest results reinforce its position as a dominant force in cloud and digital advertising. However, with spending levels elevated and expectations high, the path forward may require continued execution discipline to justify current valuations and maintain investor confidence.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts