AAPL Stock Revives on Broadcom-Apple Partnership to 2031, but Faces Key Level Above

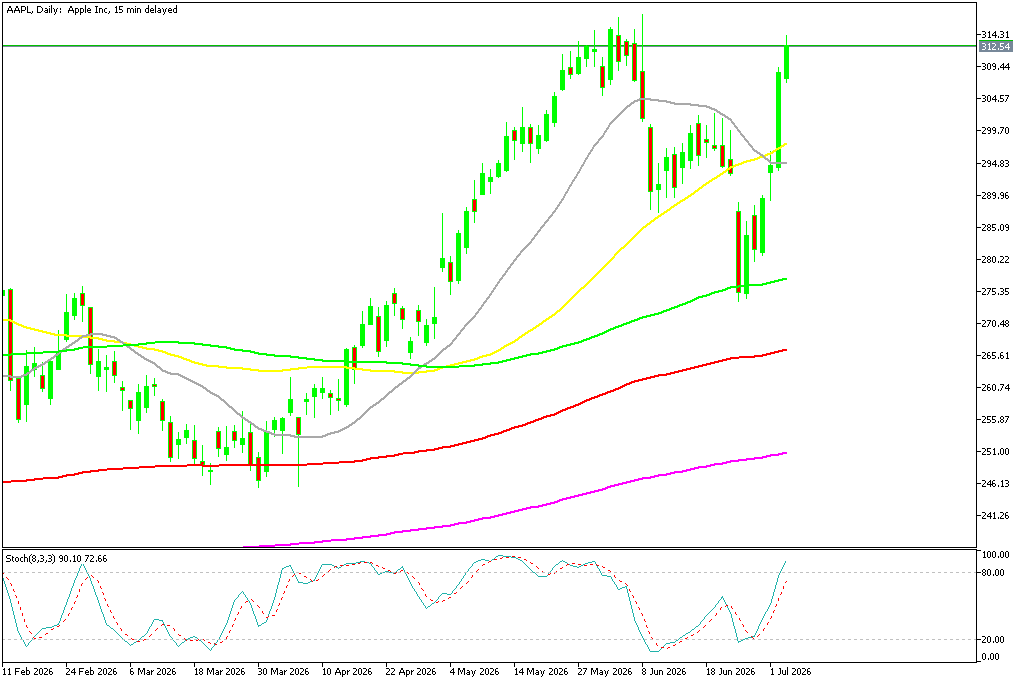

AVGO and Apple shares have rebounded above $300 after a sharp June selloff, but rising costs, shifting sentiment, and technical resistance near $315 are limiting further upside momentum.

Quick overview

- Apple shares have rebounded above $300 after a significant selloff in June, but face resistance near $315 due to rising costs and market sentiment.

- Broadcom's extension of its partnership with Apple through 2031 has provided some stability to Apple's supply chain amid ongoing semiconductor volatility.

- Concerns over pricing adjustments and rising memory costs have led to downward revisions in Apple's gross margin expectations, impacting investor sentiment.

- Despite strong earnings and cash flow, Apple's future growth narrative is under scrutiny as legal risks and competitive pressures in AI intensify.

AVGO and Apple shares have rebounded above $300 after a sharp June selloff, but rising costs, shifting sentiment, and technical resistance near $315 are limiting further upside momentum.

AAPL Rebounds After June Selloff, But Structural Concerns Persist

Apple Inc. experienced a sharp downturn in June as investors reassessed its long-term pricing power, margin durability, and growth trajectory. The selloff reflected a convergence of macro and company-specific concerns, including rising input costs, shifting product pricing dynamics, and broader uncertainty around Apple’s next growth phase.

However, July has delivered a strong rebound, with AAPL pushing back above the $300 level. The recovery has been partly supported by renewed optimism following Broadcom’s extension of its strategic relationship with Apple, which has helped stabilize sentiment across both AAPL and AVGO shares. Despite the rebound, the stock is now approaching a key resistance zone near $315, where selling pressure has begun to re-emerge.

Broadcom Extension Reinforces Supply Chain Stability

Broadcom recently confirmed an extension of its long-standing partnership with Apple through 2031. The agreement covers the development and supply of custom silicon components used in future Apple devices. While financial terms and shipment volumes were not disclosed, the strategic importance of the relationship is significant.

Broadcom remains a critical supplier within Apple’s hardware ecosystem, providing connectivity and networking technologies embedded across iPhones, iPads, and other devices. Analysts estimate that Apple accounts for roughly 20% of Broadcom’s annual revenue, underscoring the depth of interdependence between the two companies.

The announcement has been interpreted as a stabilizing force for Apple’s supply chain outlook, reinforcing continuity in key semiconductor inputs at a time when the broader chip sector remains volatile.

June Selloff Driven by Pricing and Margin Concerns

Apple’s June decline was triggered by a global pricing adjustment across several hardware product lines, including MacBooks and iPads. The initial market reaction was sharply negative, with the stock falling more than 5% in a single session as investors reassessed margin sustainability.

The price increases were implemented across Apple’s online store and affected multiple devices. MacBook Air pricing rose from $1,099 to $1,299, MacBook Pro from $1,699 to $1,999, while iPad Air and iPad Pro also saw notable increases. Although iPhone pricing remained unchanged, the broader adjustments were interpreted as a defensive response to cost inflation rather than evidence of stronger pricing power.

Memory Inflation Intensifies Margin Pressure

A key driver behind the pricing revisions has been rising semiconductor memory costs. DRAM prices reportedly surged by 58–63% sequentially, while NAND flash increased by 70–75%. These increases have significantly impacted Apple’s cost structure, leading to downward revisions in gross margin expectations from 49.3% to a range of 47.5–48.5%.

Markets have increasingly viewed this as a structural margin headwind rather than a temporary cost fluctuation, raising concerns that Apple’s historically high-margin hardware model may face prolonged pressure if memory pricing remains elevated.

Multiple Risk Factors Drive Sentiment Compression

Apple’s recent weakness has not been driven by a single factor, but rather a clustering of risks that have collectively weighed on sentiment.

These include rising input costs, speculation around potential long-term partnerships with legacy semiconductor players, and legal uncertainty stemming from a UK-based class-action lawsuit involving iCloud pricing. In addition, insider selling exceeding $111 million over a three-month period has added to investor caution.

Individually, these issues may appear manageable, but together they have contributed to a broader risk repricing of Apple’s equity narrative.

AAPL Shares Rebound Off the 100 SMA

Apple reported a better-than-expected fiscal Q2 2026, pushing its stock higher above $300, making a new high after breaking its December 2025 peak of $288. The buying momentum continued throughout May and AAPL stock price reached $317.40 in May but has made a steep reversal and slipped to $281 today.

AAPL Chart Daily – Reversing from All Time Highs

Post-WWDC Momentum Fades as Expectations Reset

The selloff also extends from a reversal in sentiment following Apple’s WWDC 2026 event. Initial enthusiasm had driven shares above $317, fueled by incremental improvements to Apple Intelligence, Siri enhancements, and ecosystem-wide software updates.

However, investor reaction quickly shifted as the announcements were viewed as evolutionary rather than transformative. Expectations for a more aggressive artificial intelligence strategy were not met, resulting in a gradual unwind of gains and renewed technical weakness below the $300 level.

Legal Risks and AI Competition Add Uncertainty

Additional pressure has emerged from a newly filed patent dispute related to wearable health technology, adding another layer of legal uncertainty to Apple’s expanding hardware ecosystem.

At the same time, competitive pressure in artificial intelligence continues to intensify. While rivals invest heavily in large-scale infrastructure, Apple’s approach remains focused on integrating AI features within its existing ecosystem rather than pursuing standalone monetization. This divergence has prompted debate over whether Apple’s strategy is sufficient in a rapidly evolving competitive landscape.

Strong Fundamentals Offset by Weaker Growth Narrative

Despite recent volatility, Apple continues to generate strong free cash flow and maintain a highly profitable services segment supported by a vast global installed base. These structural advantages remain intact and continue to provide financial stability.

However, investor attention has shifted decisively toward future growth visibility. Rising costs, legal risks, competitive pressures, and uncertainty over Apple’s next innovation cycle have collectively weakened sentiment.

As a result, Apple’s valuation is increasingly being shaped not by current earnings strength, but by concerns over whether its next phase of growth can justify its premium multiple—particularly as the stock approaches technical resistance near $315.

📉 Margins Stay Strong, but Risks Remain

Gross margins came in at 49.27%, exceeding expectations despite rising manufacturing and component costs. Premium pricing strategies, particularly across higher-end Pro devices, helped offset inflationary pressures.

Still, while Apple’s momentum remains strong, valuation levels, supply chain dependence, and execution risks tied to future product cycles may continue to create volatility even as the broader long-term trend stays positive. The company also boosted its quarterly dividend from $0.26 to $0.27 per share, reinforcing Apple’s reputation for consistent shareholder returns despite broader market volatility.

Apple Earnings Report

- Apple Q2 EPS $2.01 vs est. $1.95;

- revenue $111.2B vs est. $109.5B.

- iPhone $57.0B misses on supply;

- Mac $8.4B beats;

- Services $30.98B beats.

- China $20.5B. $100B buyback.

Summary:

- Apple reported Q2 fiscal 2026 EPS of $2.01, beating the $1.95 consensus, on revenue of $111.2 billion against estimates of $109.45-109.66 billion

- Net income came in at $29.6 billion versus the $28.5 billion expectation; operating income was $35.9 billion against a $34.8 billion estimate

- iPhone revenue of $56.99 billion came in marginally below estimates of $57.21 billion; CEO Tim Cook attributed the shortfall to supply constraints on advanced processor chips rather than weak demand

- Mac revenue of $8.40 billion beat the $8.02 billion estimate, boosted by the new $500 MacBook Neo, which targets the lower-priced laptop market currently dominated by Chromebooks

- Services revenue reached $30.98 billion, ahead of the $30.39 billion estimate, with the App Store continuing to generate robust income despite ongoing regulatory scrutiny in Europe

- Greater China net sales of $20.50 billion significantly outpaced estimates of $19.45 billion, a notable beat given the competitive and geopolitical pressures in that market

- iPad net sales were $6.91 billion versus $6.66 billion estimated; Wearables, Home and Accessories were $7.90 billion versus $7.70 billion estimated

- Gross margins were 49.27%, above the 48.38% consensus, reflecting Apple’s pricing discipline and product mix

- The board authorised an additional $100 billion share buyback, consistent with the prior year’s programme

- Incoming CEO John Ternus, who takes over from Cook in September, is expected to speak on the earnings call; investors are focused on Siri and AI strategy ahead of the June developer conference

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts