Can ORCL Stock Rebound From $140 as Oracle’s AI Cloud Backlog Tests Bearish Chart?

Oracle stock ORCL nears oversold levels as $638B backlog and AI cloud demand clash with capex and bearish 4-hour averages.

Quick overview

- Oracle's stock is under pressure despite a $638 billion revenue backlog and strong demand for AI infrastructure.

- The company's Q4 FY2026 revenue rose significantly, driven by cloud and AI contracts, but concerns about capital spending and cash flow persist.

- Piper Sandler remains optimistic about Oracle's cloud capacity growth, projecting substantial revenue increases in fiscal 2027.

- Investors are cautious, focusing on the need for Oracle to convert its backlog into profitable revenue without excessive debt.

Oracle shares remain under pressure despite massive cloud demand, as investors weigh a $638 billion revenue backlog, rising AI infrastructure capacity, and heavy capital spending.

Oracle Pullback Tests AI Cloud Bulls

Oracle has become one of the most important AI infrastructure companies in the market, but its stock is still trading like investors are worried about the cost of that growth. The key debate now is whether Oracle’s enormous cloud backlog can turn into profitable revenue fast enough to justify the buildout.

Oracle’s $638 Billion Backlog Changes the Story

Oracle is no longer just a legacy software company migrating customers to the cloud.

In Q4 FY2026, Oracle’s remaining performance obligations rose by $85 billion sequentially to $638 billion. That scale of contracted demand puts Oracle in a different category, closer to a cloud-capacity platform than a traditional enterprise software vendor.

The growth is being driven by AI infrastructure contracts, hyperscale cloud commitments, and demand for Oracle Cloud Infrastructure capacity. Investors are increasingly focused on how quickly that backlog converts into recognized revenue.

Defense AI Partnerships Add Another Growth Layer

Oracle has also been expanding its defense and government AI ecosystem through new cloud and AI partnerships.

That matters because defense customers often value secure cloud infrastructure, sovereign data control, and long-duration contracts. If Oracle can pair OCI scale with mission-critical government and defense workloads, it could further strengthen its backlog and differentiate itself from cloud rivals.

The opportunity is large, but execution timelines and procurement cycles can be long.

OCI Growth Becomes the Main Engine

Oracle’s latest numbers show how quickly the business mix is changing.

Q4 FY2026 total revenue reached $19.2 billion, up 21% year over year. Total cloud revenue rose 47% to $9.9 billion, while cloud infrastructure revenue jumped 93% to $5.8 billion.

For the full year, Oracle reported $67.4 billion in revenue, up 17%, while total cloud revenue rose 39% to $34 billion. OCI revenue for FY2026 climbed 77% to $18.1 billion.

That makes infrastructure the center of the investment case. Oracle is now being valued less on database migration alone and more on whether it can monetize AI cloud demand at scale.

Piper Sandler Sees More OCI Upside

Piper Sandler remains bullish on the cloud-capacity thesis.

The firm estimates Oracle could bring around 2,400 megawatts of new cloud capacity online in fiscal 2027, potentially lifting OCI revenue above earlier expectations. Piper sees OCI revenue reaching roughly $41.1 billion in fiscal 2027 and maintained an Overweight rating with a $225 price target.

That supports the argument that Oracle’s near-term revenue estimates may still be too low if capacity deployment proceeds on schedule.

Capex and Cash Flow Remain the Main Risk

The bear case is not demand. It is funding.

Oracle generated $32 billion in operating cash flow in FY2026, up 54%, but free cash flow was negative $23.7 billion because of heavy infrastructure investment. Management has also guided toward another major capital spending cycle and additional financing needs in FY2027.

That is why investors remain cautious. A $638 billion backlog is powerful, but only if Oracle converts it into high-margin revenue without excessive debt, dilution, or margin pressure.

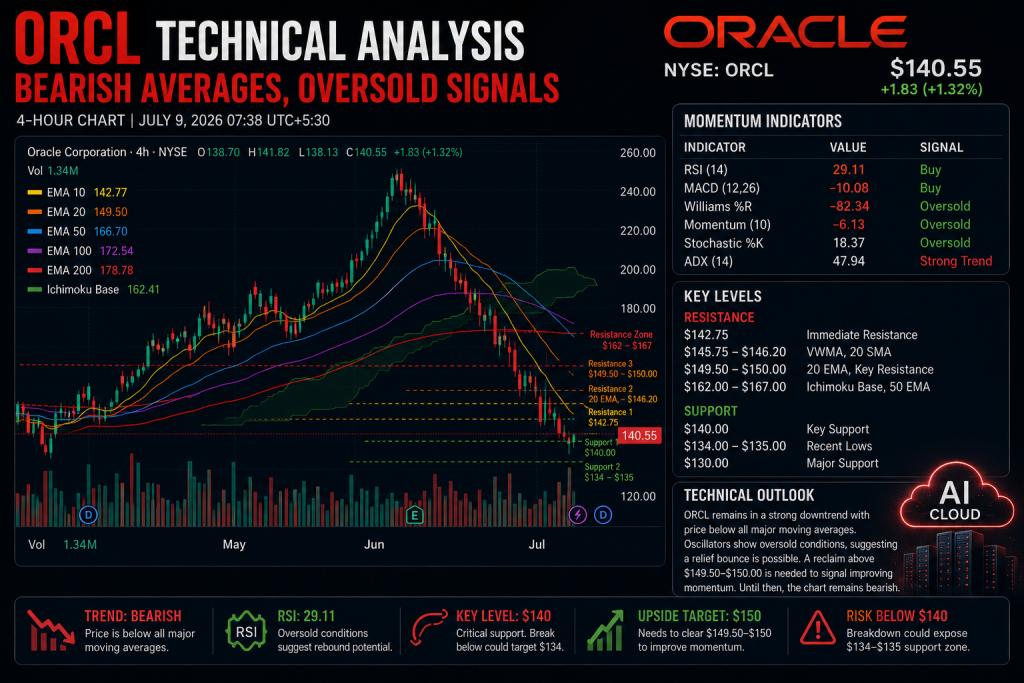

ORCL Technical Analysis: Bearish Averages, Oversold Signals

From a technical perspective, Oracle’s 4-hour chart remains weak.

ORCL is trading below the 10 EMA at $142.77, 20 EMA at $149.50, 50 EMA at $166.70, and 200 EMA at $178.78. All major moving averages are flashing sell signals, showing that sellers still control the trend.

However, oscillators are beginning to show oversold conditions. RSI stands at 29.11, which is a buy signal, while Williams %R at -82.34, Momentum at -6.13, and MACD at -10.08 also point to a possible rebound attempt.

The ADX at 47.94 shows the current trend has strength, so buyers need confirmation before calling a bottom.

Key Levels: $140, $146 and $150

The immediate support level is $140. If Oracle breaks below that area, the next downside zone sits near $134-$135, close to recent lows.

On the upside, buyers need to reclaim $142.75, followed by $145.75-$146.20, where the VWMA and 20 SMA sit. A stronger recovery would require a move above $149.50-$150, which would signal that short-term momentum is improving.

The bigger resistance zone remains $162-$167, where the Ichimoku base line and 50 EMA are located.

Oracle’s Backlog Is Bullish, But Cash Conversion Must Improve

Oracle’s long-term AI cloud story remains compelling. The company has a massive contracted revenue base, strong OCI growth, and rising demand from hyperscalers, enterprise customers, and government workloads.

But the market is demanding proof that this infrastructure buildout will translate into free cash flow and earnings power. Until cash conversion improves, ORCL may continue trading at a discount to its cloud potential.

For now, $140 is the key level to defend. A rebound above $150 would improve sentiment, but Oracle needs stronger evidence of profitable backlog conversion before the stock can regain its former highs.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts

Ava