Google Stock GOOG Heads to $300 as Brain Drain and AI Overspending Concerns Weigh on Shares

Alphabet shares extended their recent decline, falling 5% as the loss of key AI researchers and an $80 billion fundraising initiative intensified concerns that the escalating costs of the AI race are becoming increasingly difficult for investors to justify.

Quick overview

- Alphabet shares fell 5% due to the departure of key AI researchers and concerns over escalating costs in the AI race.

- The company's $80 billion fundraising initiative has raised investor worries about the sustainability of AI investments.

- Despite strong financial results, investor focus has shifted to long-term profitability and the challenges of maintaining competitive advantage.

- Regulatory risks and rising capital expenditures further complicate Alphabet's efforts to justify its significant investments in AI.

Alphabet shares extended their recent decline, falling 5% as the loss of key AI researchers and an $80 billion fundraising initiative intensified concerns that the escalating costs of the AI race are becoming increasingly difficult for investors to justify.

Tech Staff Departures Trigger Fresh Selling Pressure

Alphabet’s stock came under renewed pressure after two high-profile departures reignited concerns about the company’s ability to maintain its leadership position in artificial intelligence. Investors reacted negatively to news that Noam Shazeer, one of the most influential figures behind Google’s Gemini AI models, has left the company to join OpenAI.

The departure is particularly significant given Shazeer’s history with the company. After previously leaving Google to co-found Character.AI, he returned in 2024 through a costly $2.7 billion transaction that was widely viewed as a strategic move to strengthen Alphabet’s AI capabilities. Losing him again raises uncomfortable questions about the company’s ability to retain elite talent despite spending billions to secure it.

Investor concerns were compounded by reports that Nobel Prize-winning DeepMind scientist John Jumper has also departed for rival Anthropic. The loss of two prominent researchers within a short period has fueled fears of a broader talent migration as competition for the world’s leading AI experts reaches unprecedented levels.

The departures have shifted attention away from Alphabet’s technological achievements and toward the growing challenge of defending its position against increasingly aggressive rivals.

Massive Fundraising Plan Raises Questions About AI Economics

Adding to market anxiety is Alphabet’s recently announced $80 billion capital-raising initiative, one of the largest fundraising programs ever proposed by a major technology company.

The plan includes approximately $30 billion in public offerings through multiple securities, a $40 billion at-the-market share sale program, and an additional $10 billion private placement involving Berkshire Hathaway. While management has framed the initiative as a strategic move to strengthen the company’s financial flexibility, investors have interpreted the announcement less favorably.

Rather than inspiring confidence, the fundraising effort has highlighted the extraordinary costs associated with the artificial intelligence arms race. Building advanced AI models requires massive investments in data centers, specialized processors, networking infrastructure, and energy-intensive computing resources.

For many investors, the sheer size of the capital raise suggests that future spending requirements may be far greater than previously expected. The announcement has intensified concerns that even the largest technology companies may struggle to generate attractive returns on the enormous sums now being committed to AI development.

Strong Financial Results Fail to Impress Investors

Ironically, Alphabet’s recent share price weakness comes despite exceptionally strong financial performance.

The company reported first-quarter revenue approaching $110 billion, representing growth of more than 20% year-over-year. Net income surged by more than 80%, driven by continued strength in search advertising, cloud computing, and AI-related services.

Under normal circumstances, such results would likely have propelled the stock higher. Instead, investors largely ignored the earnings beat and focused on future spending obligations.

The market’s attention has shifted away from current profitability and toward long-term return on investment. Investors are increasingly asking whether the enormous capital being directed toward AI infrastructure will ultimately generate enough revenue and earnings growth to justify the expense.

As a result, Alphabet’s strong financial performance has been overshadowed by concerns about future margins and capital efficiency.

Regulatory Risks Add Another Layer of Uncertainty

Beyond talent retention and spending concerns, Alphabet continues to face mounting regulatory challenges.

European regulators have recently intensified antitrust discussions after reportedly rejecting previous proposals aimed at addressing competition concerns. The renewed scrutiny has revived fears that Google’s search dominance, advertising business, Android ecosystem, and future AI offerings could face additional restrictions.

For investors already worried about escalating costs, regulatory uncertainty introduces another significant risk factor. Potential fines, operational changes, or restrictions on product deployment could complicate Alphabet’s efforts to monetize its AI investments effectively.

The timing is particularly problematic as the company attempts to defend its competitive position while simultaneously increasing spending at an unprecedented pace.

Technical Levels in Focus

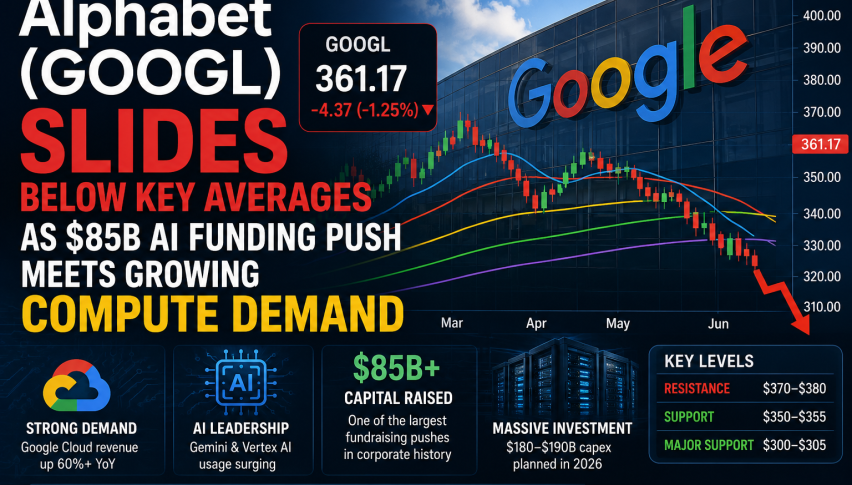

From a chart perspective, Alphabet slipped below its 50-day moving average (yellow) near $320 in February and the 100 SMA (green) at $300 was broken too, which opened the door for further losses toward $270. That’s where the 200 SMA (red) stood and it provided support, holding the decline and we saw a rebound from there, sending GOOGL above $408 on in May but reversed in June and is heading lower again, slipping below $350 today and risking to fall below $300 as investors turn cautious.

GOOGL Chart Daily – The 200 SMA Held As Support

Cloud Growth Continues, But Costs Keep Rising

One of Alphabet’s strongest business segments remains Google Cloud, which continues to benefit from growing enterprise demand for AI services and advanced computing infrastructure.

The division generated more than $20 billion in quarterly revenue and maintains a substantial backlog approaching $460 billion. These figures demonstrate that customer demand remains robust and that Alphabet remains a major player in the enterprise AI ecosystem.

However, investors are increasingly focused on the cost side of the equation. Expanding cloud infrastructure, developing advanced AI models, and maintaining competitive computing capacity require extraordinary levels of capital investment.

As these costs continue to rise, profitability becomes increasingly dependent on flawless execution and sustained demand growth.

Expectations Leave Little Room for Disappointment

Perhaps the biggest challenge facing Alphabet is the enormous expectations embedded in its valuation.

Investors continue to assume the company will remain a dominant force in artificial intelligence while simultaneously expanding its cloud business and protecting its highly profitable advertising franchise. Any signs of weakness—whether through talent departures, rising costs, regulatory setbacks, or slower growth—can quickly trigger sharp market reactions.

The recent selloff reflects growing concern that the economics of the AI race may be becoming less attractive than originally anticipated. With spending accelerating, competition intensifying, and key personnel departing, Alphabet’s margin for error is narrowing.

While the company remains one of the most powerful technology businesses in the world, investors are increasingly questioning whether the future rewards of AI leadership will be sufficient to justify the rapidly growing financial commitments required to maintain it. For now, concerns over costs, competition, and talent retention are overshadowing strong earnings and weighing heavily on sentiment toward the stock.

Strong Growth, but Costs Are Rising

Despite robust fundamentals, concerns are building around spending. Alphabet’s core businesses—search, advertising, and cloud—continue to perform strongly, but the cost of maintaining that growth is increasing.

Estimates suggest capital expenditures could reach $175 billion to $185 billion in 2026, driven by infrastructure buildout and AI development.

- Higher capex may pressure margins

- Monetization of AI products remains uncertain

- Returns on investment could take time to materialize

This shift has prompted investors to look beyond revenue growth and focus more closely on profitability.

-

- Total Revenue: $109.9 billion, exceeding analysts’ predictions of $107.2 billion.

- Net Income: $62.58 billion, up 81% from $34.54 billion in Q1 2025.

- Earnings Per Share (EPS): $5.11, significantly beating the estimated $2.62.

- Google Search & Other: Revenue grew 19% to $77.25 billion, driven by high search usage.

- Google Cloud: Revenue jumped 63% to $20.03 billion, with a backlog exceeding $460 billion, highlighting intense demand for AI infrastructure.

- YouTube Advertising: Reported $9.88 billion, missing some analyst expectations.

- Capital Expenditure (CapEx): Raised 2026 guidance to $180B–$190B, signaling aggressive AI investment.

- Dividend: Announced a 5% increase to $0.22 per share quarterly.

- AI Growth: CEO Sundar Pichai noted that AI investments are enhancing all business areas, with AI-driven search experiences pushing query volume to all-time highs.

- Stock Surge: Following the report, Alphabet stock saw a strong positive reaction in after-hours trading, with many analysts highlighting the “earnings crush”.

- Growth Outlook: Total paid subscriptions, including YouTube and Google One, reached 350 million, and Gemini Enterprise saw 40% quarter-over-quarter growth in paid users

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts