Will INTC Stock Break Below $108 as AI Chip Selloff Tests Intel Foundry Bulls?

Intel stock INTC plunges 9.7% as AI chip profit-taking hits, with $108 support and July 23 earnings now critical.

Quick overview

- Intel shares fell nearly 10% as profit-taking affected semiconductor stocks amid concerns over CPU price hikes and yield issues.

- The decline followed a significant rally, leaving Intel vulnerable to valuation concerns after reaching a high of $140 in late June.

- Analysts remain optimistic, with HSBC raising its price target to $200, citing long-term potential in Intel's foundry business despite current challenges.

- Intel's upcoming earnings report on July 23 is critical, as it will determine the stock's direction amidst ongoing concerns about profitability and market competitiveness.

Intel shares tumbled nearly 10% as profit-taking spread across semiconductor stocks, while investors weighed 18A yield concerns, CPU price hikes, and bullish analyst targets ahead of Q2 earnings.

Intel Slides 9.2% as Semiconductor Rally Cools

Intel suffered another sharp decline as semiconductor investors continued taking profits from AI-linked chip stocks. The selloff follows a powerful rally that had pushed INTC up nearly 286% year to date, leaving the stock vulnerable once valuation concerns returned.

Samsung Selloff Triggers AI Hardware Reset

Intel’s decline came as a broader semiconductor selloff accelerated after Samsung Electronics issued strong preliminary results that still failed to impress investors.

The reaction was telling. Rather than rewarding record profits, traders focused on whether AI-related chip expectations had become too high. Samsung shares dropped sharply in South Korea, while weakness spread to memory, processor, and AI hardware names.

For Intel, the pressure was amplified by its recent run. After moving above $140 in late June, the stock quickly reversed as investors questioned whether the AI infrastructure trade had become overcrowded.

Foundry Execution Becomes the Central Risk

The biggest company-specific concern remains Intel’s foundry turnaround.

Reports suggesting Intel’s 18A process may not reach profitable yields until late 2026 or 2027 have increased pressure on the stock. Intel’s foundry business is central to the bull thesis, but it remains early-stage and capital intensive.

In Q1 2026, Intel Foundry generated only $174 million in external customer revenue while posting a large operating loss. Investors now want proof that 18A can attract meaningful production volume from external customers and improve manufacturing economics.

That makes the July 23 earnings report especially important.

CPU Price Hikes Add Another Layer

Intel also confirmed price increases on select consumer and server CPUs.

The company cited rising supply-chain costs and strong demand, especially in higher-end Core Ultra and Xeon products. Some consumer chips rose by $30-$50, while several high-end Xeon processors saw much larger price changes.

The price hikes could support margins if demand holds, but they also raise questions about competitiveness against AMD and other rivals. For enterprise customers, negotiated pricing may soften the headline impact, but investors will still watch whether higher ASPs help offset foundry losses and manufacturing costs.

HSBC Stays Bullish With $200 Target for INTC Stock

Despite the selloff, several analysts remain constructive.

HSBC doubled its Intel price target to $200 from $100 while maintaining a Buy rating, citing the long-term potential of Intel’s foundry business, advanced packaging, and domestic semiconductor manufacturing support.

Bank of America also lifted its target to $160, while New Street Research raised its target to $122.

The bullish argument is that Intel is one of the few companies capable of becoming a major Western foundry alternative at scale. The bearish argument is that the stock has already priced in a turnaround before execution has been fully proven.

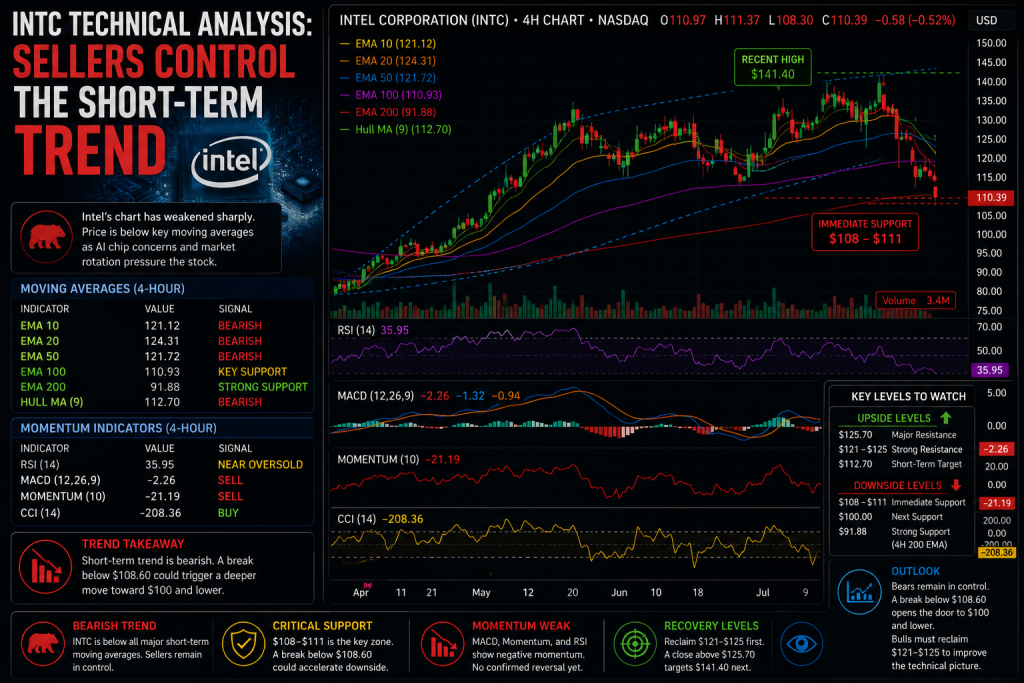

INTC Technical Analysis: Sellers Control the Short-Term Trend

From a technical perspective, Intel’s 4-hour chart has weakened sharply.

INTC is trading below the 10 EMA at $121.12, 20 EMA at $124.31, and 50 EMA at $121.72, showing that short-term momentum has shifted decisively bearish. The stock is also just below the 100 EMA at $110.93, making the current level critical.

Momentum signals remain negative. MACD shows a sell signal at -2.26, while Momentum is at -21.19. RSI sits at 35.95, close to oversold but not yet showing a confirmed reversal.

The CCI at -208.36 flashes a buy signal, suggesting the selloff may be stretched, but buyers still need confirmation.

Key Levels: $108, $125 and $141

The immediate support zone is $108-$111.

A sustained break below $108.60 would weaken the chart and could expose Intel to a deeper pullback toward $100, followed by the 4-hour 200 EMA near $91.88.

On the upside, the first recovery target is $112.70, near the Hull Moving Average. A stronger rebound would require reclaiming $121-$125, where multiple moving averages now act as resistance.

A close above $125.70 would improve the technical setup and could open the door toward $141.40, the next major upside target from the recent channel structure.

Intel’s Earnings on July 23 Will Decide the Next Move

Intel’s long-term turnaround story remains alive, but the stock is now entering a critical test.

Bullish analysts are focused on foundry potential, AI server demand, and government-backed domestic chip manufacturing. Bears are focused on valuation, delayed 18A profitability, foundry losses, and the risk that the AI hardware trade has overheated.

For now, $108 is the key support level. If Intel holds it, the stock could stabilize before earnings. If it breaks, the recent correction may deepen before management gets a chance to reset expectations on July 23.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts

Ava