Oracle Stock ORCL Slips Below 130 Ahead of Dividend on AI Spending Surge and Rising Debt

Oracle shares remain under pressure as investors grow increasingly uneasy that massive AI infrastructure spending, rising debt burdens, and aggressive cost-cutting efforts are beginning to overshadow the company’s impressive cloud growth story.

Quick overview

- Oracle shares fell nearly 6% following strong earnings, as investors are increasingly worried about rising debt and AI infrastructure spending overshadowing cloud growth.

- Despite reporting earnings that beat expectations, concerns about the sustainability of growth and high capital expenditures led to a selloff in Oracle's stock.

- The company is preparing to distribute a quarterly dividend of $0.50 per share, but this has not improved short-term investor sentiment.

- Investor focus has shifted from growth potential to the financial risks associated with Oracle's aggressive expansion strategy and rising debt levels.

Oracle shares remain under pressure as investors grow increasingly uneasy that massive AI infrastructure spending, rising debt burdens, and aggressive cost-cutting efforts are beginning to overshadow the company’s impressive cloud growth story.

Oracle Stock Extends Decline Despite Strong Earnings Results

Oracle shares continued their retreat on Monday, falling nearly 6% and slipping below the important $130 support level as the stock moved closer toward the $120 region.

The decline is notable because it came immediately after another earnings report that comfortably beat Wall Street expectations. Under normal circumstances, such results would likely have supported another leg higher in Oracle shares.

Instead, investors focused on the growing financial risks associated with the company’s increasingly expensive expansion strategy.

The market reaction highlights a broader shift taking place across the technology sector, where investors are becoming less willing to reward revenue growth if it is accompanied by rapidly rising spending commitments and deteriorating balance sheet metrics.

For Oracle, the debate is no longer whether the company can grow, but whether that growth can justify the enormous financial commitments now being made.

Oracle Prepares to Reward Shareholders With Dividend Payment

Despite recent weakness in the stock price, Oracle is preparing to return capital to shareholders through its upcoming dividend payment.

Oracle is scheduled to distribute its quarterly dividend on Friday, July 24, with shareholders receiving $0.50 per share.

Investors who owned Oracle shares as of the July 10 record date will qualify for the payment, which remains unchanged from previous quarters.

For example, an investor holding 100 Oracle shares will receive $50 in dividend income next week.

While the dividend provides some support for long-term investors, it has done little to improve short-term sentiment surrounding the stock.

Earnings Beat Fails to Impress Investors

Oracle reported quarterly earnings per share of $2.11 on revenue of $19.18 billion, surpassing analyst expectations of $1.97 per share and $19.09 billion in revenue.

The results also represented significant improvements from the same period a year earlier, when Oracle reported earnings of $1.70 per share on revenue of $15.9 billion.

Cloud infrastructure demand remained exceptionally strong while Oracle’s traditional software business continued generating stable cash flow.

However, the market largely ignored those positives.

Instead, investors focused on concerns that Oracle’s future growth could become increasingly expensive to maintain as competition intensifies across the cloud computing industry.

The latest earnings reaction suggests investors are becoming more interested in the quality and sustainability of growth rather than simply rewarding headline earnings beats.

AI Infrastructure Spending Raises Overspending Concerns

The biggest issue weighing on Oracle remains the scale of its investment commitments.

Capital expenditure reached approximately $16.5 billion during the quarter, lifting annual spending to nearly $56 billion and exceeding previous guidance from management.

Looking further ahead, Oracle expects net capital expenditure to increase to roughly $70 billion during fiscal 2027.

Once equipment prepayments and component commitments are included, total spending obligations could approach between $90 billion and $95 billion.

Those figures have become a major source of concern for investors.

The issue is not necessarily a lack of demand for AI infrastructure but rather whether future revenues will ultimately justify today’s extraordinary spending levels.

As virtually every major technology company races to build data centers and expand cloud capacity, fears are growing that the industry could eventually face oversupply and declining returns on investment.

Oracle has become one of the clearest examples of that risk.

Rising Debt Levels Create Additional Pressure

Funding such aggressive expansion plans has required Oracle to significantly increase borrowing.

Over the past fiscal year, the company raised approximately $43 billion through debt issuance while also generating another $5 billion through equity offerings.

Management has indicated that an additional $40 billion in financing could potentially be raised during fiscal 2027 if required.

Although executives argue that these investments are essential to capture long-term opportunities in cloud computing and AI infrastructure, investors are becoming increasingly uncomfortable with the speed at which leverage is rising.

Higher debt levels become particularly concerning in an environment where interest rates remain elevated and financing costs continue increasing.

For many investors, Oracle’s balance sheet is becoming just as important as its earnings performance.

Major Workforce Reductions Raise Questions

Investor concerns have been amplified by Oracle’s decision to reduce its workforce by approximately 21,000 employees, representing around 13% of global staff.

The layoffs form part of a major restructuring effort designed to lower costs and redirect resources toward cloud infrastructure and AI initiatives.

However, large workforce reductions often raise difficult questions about management’s outlook.

Some investors view the cuts as evidence that Oracle is attempting to offset rising infrastructure spending elsewhere in the business or prepare for slower economic conditions.

Oracle expects the restructuring programme to generate approximately $1.8 billion in charges, making it one of the largest operational adjustments in recent company history.

Oracle Selloff Accelerates Despite Strong Headline Results

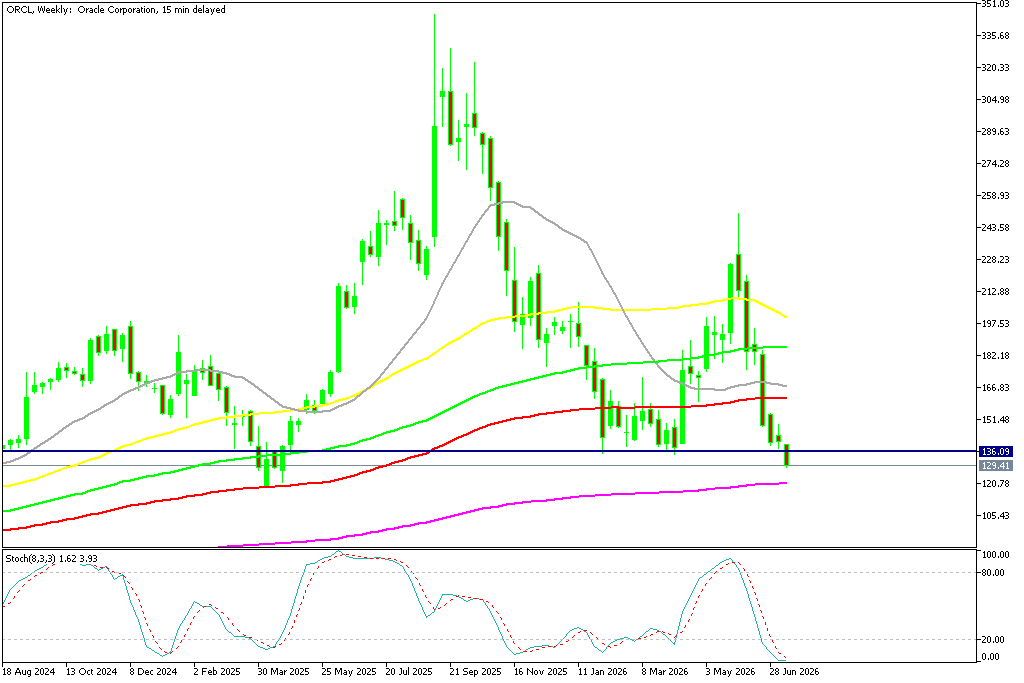

Oracle shares extended their sharp decline following the company’s fiscal fourth-quarter earnings release, with the stock falling below the $130 support zone after investors looked beyond better-than-expected earnings and focused on mounting AI infrastructure costs and slowing cloud momentum. Although Oracle delivered solid revenue and profit growth, concerns that capital spending is rising faster than sustainable returns triggered heavy selling and renewed debate over whether the AI investment boom is becoming too excessive. Now the next target is the 200 weekly SMA at $120.

ORCL Chart Weekly – Breaking the Support

Cloud Growth Remains Strong But Misses Expectations

Oracle’s cloud business remains the centerpiece of its long-term investment story.

Total cloud revenue reached $9.91 billion during the quarter, narrowly missing analyst expectations of $9.99 billion.

Although the difference was relatively small, investors viewed the miss as meaningful given the extraordinary level of investment currently taking place.

Cloud Infrastructure revenue surged 93% year-over-year to $5.8 billion and exceeded forecasts, highlighting continued demand for Oracle’s services.

Even so, the market expected stronger results considering the pace of spending across Oracle’s AI infrastructure programme.

The figures reinforced concerns that capital expenditure may be growing faster than revenues.

Massive Backlog Provides Limited Relief

Oracle attempted to reassure investors by highlighting its growing order pipeline.

Remaining performance obligations climbed to an impressive $638 billion, far exceeding market expectations and reflecting substantial long-term customer commitments.

Management also pointed to progress on major data center projects and highlighted customer contracts that include upfront payments to reduce financing needs.

Under different market conditions, these developments would likely have strengthened investor confidence.

Instead, markets remained focused on execution risks and future funding requirements.

Investors Shift Focus Toward Risk Management

Oracle recently secured additional government cloud contracts and continues to benefit from strong enterprise demand for digital infrastructure solutions.

However, these achievements have largely been overshadowed by concerns surrounding spending, leverage, and execution risk.

The narrative surrounding Oracle has changed significantly over recent months.

Rather than focusing exclusively on the opportunities created by AI infrastructure, investors are increasingly concentrating on the financial risks associated with funding and executing such an ambitious expansion strategy.

Until Oracle can demonstrate that rising investment levels are translating into stronger free cash flow generation and sustainable profitability, the stock may continue to experience elevated volatility.

For now, Wall Street appears far more concerned about the cost of Oracle’s ambitions than the rewards those ambitions may eventually produce.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts