WFC Stock Slips Toward $85 as Wells Fargo Profit Beat Fails to Ease Margin Concerns

Wells Fargo WFC stock slips despite Q2 profit beat as NIM pressure and unchanged guidance offset trading and loan-growth strength.

Quick overview

- Wells Fargo's shares declined despite reporting stronger-than-expected Q2 earnings, as investors were concerned about net interest margin compression and unchanged full-year guidance.

- The bank's net income reached $6.41 billion, with a 9% revenue increase to $22.62 billion, but investors were looking for more optimistic forward guidance.

- Loan growth improved significantly after the removal of the Federal Reserve's asset cap, with average loans rising 12% year over year.

- While credit quality remains stable, investors are cautious about the potential impact of inflation and interest rates on future earnings.

Wells Fargo shares fell despite stronger Q2 earnings, as investors focused on net interest margin compression and unchanged full-year guidance.

Wells Fargo Pulls Back as Strong Earnings Meet Higher Expectations

Wells Fargo delivered a stronger-than-expected second-quarter report, but the stock still moved lower as investors questioned whether the headline earnings beat fully reflected improving fundamentals.

WFC closed at $85.29, down 2.71%, before recovering slightly to $85.80 in after-hours trading. The decline came even after the bank reported net income of $6.41 billion, or $2.00 per diluted share, beating consensus expectations near $1.72.

Revenue rose 9% to $22.62 billion, also ahead of estimates around $21.87 billion. Return on equity reached 15.0%, while return on average tangible common equity came in at 17.7%.

The numbers showed meaningful progress, but the market was looking for stronger forward guidance after Wells Fargo’s regulatory asset cap was lifted last year.

Loan Growth Improves After Asset Cap Removal

One of the strongest parts of the report was loan growth.

Average loans increased 12% year over year to $1.03 trillion, reflecting Wells Fargo’s renewed ability to expand after years of operating under the Federal Reserve’s asset cap. The bank has been focusing on growing credit cards, auto loans, commercial lending and broader client relationships.

Average deposits also rose 10% to $1.47 trillion, helping support balance sheet expansion.

CEO Charlie Scharf said consumer and business fundamentals remain resilient, supported by lower delinquencies, rising savings and solid corporate cash flows. That commentary helped reinforce the view that Wells Fargo’s core customer base remains stable despite inflation and geopolitical uncertainty.

Net Interest Margin Compression Weighs on Sentiment

The main investor concern was margin pressure.

Net interest income rose 5% to $12.32 billion, but management maintained full-year 2026 NII guidance around $50 billion. Investors had hoped that stronger loan growth would translate into a more upbeat outlook.

Management also guided for modest net interest margin compression in Q3 before stabilization in Q4. That cautious commentary limited enthusiasm around the earnings beat.

Scharf explained that some new business activity carries narrower margins, but can still help Wells Fargo attract clients and expand relationships. Investors, however, remain focused on whether the bank can grow earnings without sacrificing returns.

Investment Banking and Trading Show Strong Momentum

Wells Fargo benefited from the same capital markets recovery that lifted Goldman Sachs and JPMorgan.

Investment banking fees increased 35% to $939 million, supported by major transactions including SpaceX’s blockbuster IPO and NextEra Energy’s large deal for Dominion Energy.

Equity capital markets were particularly strong as large IPOs, AI-linked follow-on offerings and renewed dealmaking boosted fee activity across Wall Street.

Markets revenue rose 24% to $2.21 billion, as Wells Fargo deployed more balance sheet into trading and markets activity after years of constraint under the asset cap.

This is an important shift. Wells Fargo has historically been viewed as more of a traditional lending and deposit franchise than a capital markets powerhouse. Stronger performance in banking and trading could improve its earnings mix over time.

Credit Quality Remains Supportive for WFC Stock

Credit trends were also constructive.

Net loan charge-offs declined 10 basis points year over year to 0.34% of average loans, while provision for credit losses was $914 million. The bank also reported a CET1 ratio of 10.3%, within its 10.0%-10.5% target range.

Those figures suggest credit quality remains manageable even as loan growth accelerates.

Still, management warned that inflation, interest rates and affordability pressures remain risks. If inflation rises again or the labor market weakens, consumer credit could become a bigger concern later in the year.

Capital Returns Add Support

Wells Fargo also continues to return capital to shareholders.

The bank expects to raise its quarterly dividend to $0.50 per share in Q3, pending board approval. TradingView lists WFC with an indicated dividend yield around 2.07%, a market capitalization near $266.7 billion and a P/E ratio of 13.46.

That valuation is not demanding compared with many large-cap financials, but investors are still waiting for evidence that post-asset-cap growth can translate into sustainably higher returns.

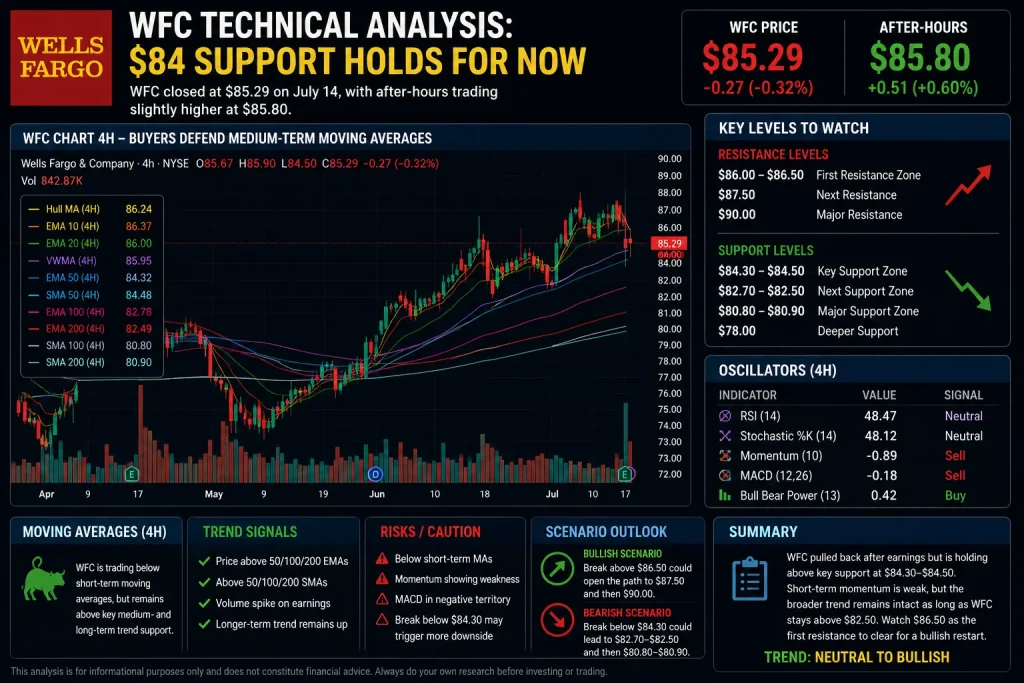

WFC Technical Analysis: $84 Support Holds for Now

WFC closed at $85.29 on July 14, with after-hours trading slightly higher at $85.80.

WFC Chart 4H – Buyers Defend Medium-Term Moving Averages

The 4-hour technical setup is mixed. Wells Fargo is trading below several short-term moving averages, showing that near-term momentum has weakened after earnings.

The 10-period EMA sits near $86.37, while the 20-period EMA is around $86.00. The Hull Moving Average at $86.24 and VWMA at $85.95 also sit above the current price, making the $86.00-$86.50 area the first resistance zone.

However, WFC remains above important medium- and long-term trend support. The 50-period EMA stands near $84.32, while the 50-period SMA is around $84.48. This makes the $84.30-$84.50 area the first key support zone.

Below that, the 100-period EMA near $82.78 and the 200-period EMA near $82.49 form a deeper support band. The 100-period and 200-period SMAs near $80.80-$80.90 mark the larger downside level if selling accelerates.

Oscillators are mostly neutral. RSI is at 48.47, while Stochastic %K is at 48.12, suggesting neither bulls nor bears have full control. Momentum and MACD are flashing sell signals, confirming short-term weakness, but Bull Bear Power is showing a buy signal, suggesting buyers are still defending the pullback.

Key Levels to Watch

The first upside level is $86.50. A move above that area could bring $88 back into focus, followed by the $90 psychological level.

On the downside, $84.30-$84.50 is the key near-term support zone. If that level fails, WFC could fall toward $82.50-$82.80. A deeper break below $80.80 would damage the broader recovery structure.

For now, the stock remains in a consolidation phase rather than a full technical breakdown.

Wells Fargo Posted a Strong Quarter, But Guidance Must Improve

Wells Fargo’s Q2 results showed real progress. Loan growth improved, investment banking rebounded, trading revenue strengthened, credit quality remained stable and capital returns are increasing.

However, investors wanted more from guidance. Unchanged full-year NII expectations and modest NIM compression kept the market focused on profitability quality rather than headline EPS strength.

The stock’s next move may depend on whether Wells Fargo can prove that post-asset-cap growth will lift returns without pressuring margins.

For now, WFC remains vulnerable below $86.50, but the broader technical structure stays constructive as long as $84.30 and $82.50 hold. A break above $88 would help restore confidence, while a drop below $82.50 could signal that investors are losing patience with the recovery story.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts