NBIS Stock Breaks Below $200 as $1B Reflection AI Deal Fails to Calm Cash Burn Fears

Nebius Group stock NBIS falls below $200 as a $1B Reflection AI deal fails to ease cash conversion and capex concerns.

Quick overview

- Nebius shares fell 7.8% despite announcing a $1 billion AI compute contract with Reflection AI, indicating investor skepticism about future profitability.

- The company is aggressively expanding its AI infrastructure, raising its capital expenditure guidance to $20-$25 billion for 2026, but investors are concerned about cash conversion and returns.

- Demand for Nebius's services remains strong, yet investors are seeking clearer evidence of higher-margin revenue generation from its expanding offerings.

- With a market capitalization near $53 billion and a high P/E ratio, the stock is under scrutiny as the market differentiates between AI demand and infrastructure economics.

Nebius shares dropped sharply despite another major AI compute contract, as investors focused on capital spending, cash conversion and slowing enthusiasm for AI cloud lessors.

Nebius Slides 7.8% as AI Contract Wins No Longer Guarantee Upside

Nebius Group shares came under heavy pressure on Tuesday, falling 7.80% to $194.09 before rebounding slightly to $198.17 after hours.

The decline came despite the company announcing a computing agreement worth more than $1 billion with Reflection AI, a U.S. startup developing open-source artificial intelligence models and autonomous coding agents.

Under the agreement, Reflection AI will gain access to Nvidia’s latest GB300 AI chips through Nebius infrastructure through 2029. The deal strengthens Nebius’s position as a major supplier of AI compute capacity for frontier model builders.

However, the market reaction shows that investors are becoming harder to impress. After a huge rally earlier in the year, large contract headlines alone are no longer enough to support NBIS shares.

Market Wants Cash Conversion, Not Just Backlog

The Reflection AI contract adds to Nebius’s already impressive list of AI infrastructure wins.

Earlier this year, Nebius signed a five-year infrastructure deal with Meta worth up to $27 billion, including $12 billion of dedicated capacity and up to $15 billion of additional available compute. Last year, the company also secured a Microsoft agreement valued at up to $19.4 billion.

Together, those deals have helped turn Nebius into one of the most visible challengers in AI cloud infrastructure.

But investors are now asking a different question: how much cash will Nebius need to spend before those contracts become revenue and profit?

The Reflection agreement is large in absolute terms, but if spread evenly through 2029, it may contribute less than $300 million per year. That is meaningful, but not enough by itself to change the near-term financial profile of a company that is spending aggressively to build capacity.

Capex Intensity Remains the Main Concern

Nebius is pursuing one of the most aggressive AI infrastructure expansion plans in the market.

The company has expanded contracted power from more than 2 GW at the end of 2025 to more than 3.5 GW in Q1 2026, and now targets at least 4 GW this year. It also announced a new Pennsylvania site that can support up to 1.2 GW of power, marking its second company-owned GW-scale AI campus in the United States.

That growth gives Nebius a credible path toward becoming an AI-native hyperscaler. However, it also requires enormous upfront capital.

Nebius raised its 2026 capital expenditure guidance to $20 billion to $25 billion, with much of that capacity expected to start generating revenue in the first half of 2027. The company also raised more than $6 billion this year, including convertible notes and Nvidia’s equity investment, helping lift cash balances above $9 billion.

That financial flexibility is important, but the stock is now being judged on whether capex can turn into durable returns rather than simply larger capacity.

Nebius AI Demand Remains Strong, but Economics Are Under Scrutiny

Demand for Nebius’s services remains robust.

The company says GPU demand continues to outpace available capacity, while first-quarter pipeline generation grew 3.5 times sequentially. More than 75% of contracted power now comes from company-owned infrastructure, improving control over the platform and potentially supporting margins over time.

Nebius is also expanding beyond raw compute. Its strategy includes bare-metal infrastructure, multi-tenant cloud, inference, agentic AI services and platform tools such as Aether 3.6. Acquisitions including Tavily, Eigen AI and Clarifai are intended to strengthen its software and AI lifecycle offering.

Still, investors want clearer evidence that these platform features can generate higher-margin revenue. Without that proof, Nebius risks being viewed mainly as a capital-heavy GPU capacity provider.

NBIS Valuation Leaves Little Room for Disappointment

TradingView lists Nebius with a market capitalization near $53 billion, a trailing P/E ratio around 73 and a one-year beta above 3, highlighting the stock’s high-risk profile.

The shares remain up more than 150% year to date and more than 300% over the past year, according to TradingView performance data. That means investors have already priced in a large amount of future AI infrastructure success.

The stock’s pullback suggests that the market may now be separating AI demand from AI infrastructure economics. Nvidia can still benefit from chip demand, while companies like Nebius and CoreWeave face greater scrutiny over financing costs, depreciation, utilization and customer concentration.

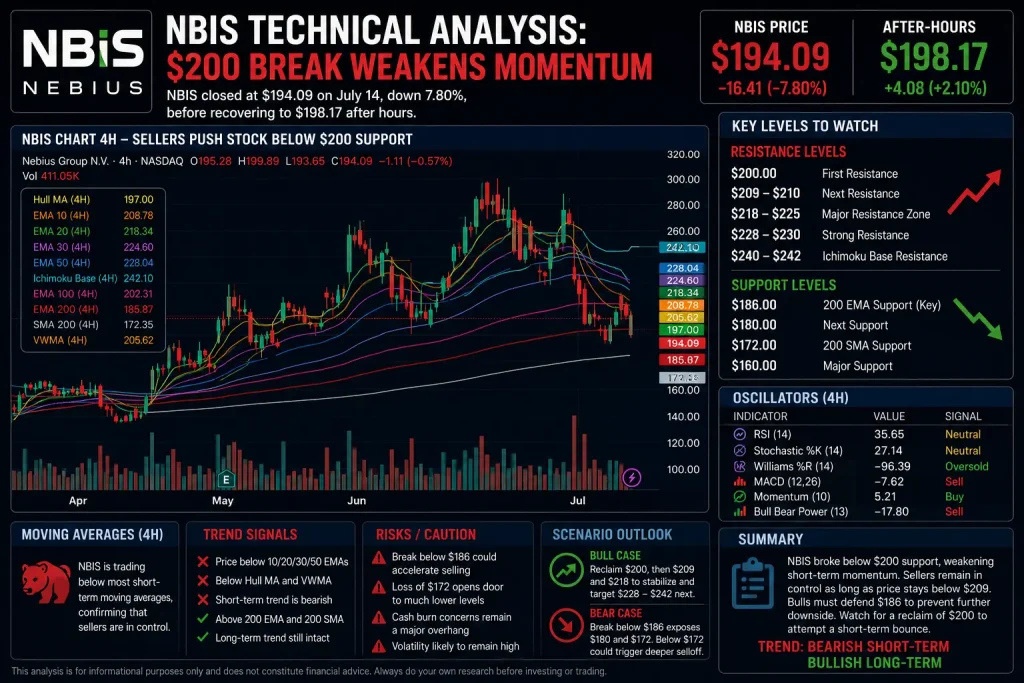

NBIS Technical Analysis: $200 Break Weakens Momentum

NBIS closed at $194.09 on July 14, down 7.80%, before recovering to $198.17 after hours.

NBIS Chart 4H – Sellers Push Stock Below $200 Support

The 4-hour chart shows a clear short-term breakdown. NBIS is trading below most major moving averages, confirming that sellers remain in control after the recent decline.

The 10-period EMA sits near $208.78, while the 20-period EMA is around $218.34. These levels now form the first resistance area. Above that, the 30-period EMA near $224.60 and 50-period EMA near $228.04 create a heavier resistance band.

The Hull Moving Average near $197.00 is close to the after-hours price and may act as the first short-term pivot. If NBIS cannot regain $200 quickly, sentiment may remain fragile.

The most important support is the 200-period EMA near $185.87. Below that, the 200-period SMA sits around $172.35. These longer-term averages are still on buy, meaning the broader trend has not fully collapsed, but they are now the key levels bulls need to defend.

Oscillators show weakness but not a clean reversal. RSI is at 35.65, near oversold territory, while Williams %R near -96.39 suggests the stock is deeply stretched to the downside. Momentum is flashing a buy signal, but MACD remains on sell, confirming that bearish pressure is still active.

Key Levels to Watch

The first upside level is $200. A recovery above that zone would help stabilize sentiment, but NBIS still needs to reclaim $209 and then $218 to repair short-term technical damage.

A move above $228 would suggest the pullback is easing and could bring the $240-$242 Ichimoku base area back into focus.

On the downside, $186 is the key support level. A break below the 200-period EMA would expose NBIS to $180, followed by the 200-period SMA near $172. If selling accelerates below $172, the stock could face a deeper valuation reset.

Nebius Has Strong Demand, Tougher Market Reaction

Nebius remains one of the most important emerging AI infrastructure companies. The Reflection AI deal adds another credible customer, while Microsoft, Meta and Nvidia-linked demand reinforce the long-term growth story.

However, investor expectations have changed. The market no longer wants only large contract announcements. It wants evidence that Nebius can deploy capacity on time, convert deferred revenue into recognized sales, maintain high utilization and reduce capital spending intensity relative to revenue.

Until that happens, NBIS may remain volatile.

For now, the stock is technically vulnerable below $200. A recovery above $218 would improve the near-term picture, but failure to hold $186 could open the door to a deeper correction toward $172.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts