Forex Signals US Session Brief, Oct 31 – USD Declines on Dovish FED, Safe Havens Rally on Trade Pessimism

The USD turned bearish yesterday after Powell's comments, while safe havens are rallying today on China comments on trade

Yesterday the FED cut interest rates for the third time in the last three meetings, bringing them down to 1.75%. As I predicted, the USD jumped higher immediately after the rate cut announcement, since markets knew already that it was coming. So, the statement and the press conference were going to be more important, letting us know where the FED is headed for the coming months. FED chairman, Jerome Powell said that the monetary policy is in a good place now, meaning that they are done with rate cuts for the time being. But then he added that inflation needs to pick up substantially for them to start hiking rates again. With Crude Oil prices falling and the global economy slowing, it will take along time for inflation to increase, which leaves the FED more likely to cut rates again then to increase them. So, the USD turned bearish and it is continuing to slide lower today as well.

Safe havens moved higher yesterday after Powell’s press conference and they received another boost today after comments from China that a long-term trade deal with the US is impossible as long as Donald Trump is in office. This doesn’t mean that “Phase One” deal is off the table, but it will be difficult to move ahead with “Phase Two” and “Phase Three”. China wants the US to remove all tariffs before going ahead with the deal, but they haven’t really committed to tackling IP theft and currency manipulation, which have been the main requests from Trump. So, things don’t look good and safe havens are taking advantage of the situation. In Europe, headline inflation moved lower to 0.7% today, but core inflation picked up at least.

The European Session

- German Retail Sales – Retail sales have been declining during four out of the last five months in Germany. Last month’s report showed a 0.5% increase for August, but that was revised lower again today to -0.1%. For September, today’s report was expected to show a 0.3% increase, but sales missed expectations, increasing by 0.1% only, which might be revised lower as well next month.

- French CPI Inflation – French economy slowed down in Q2 and in Q3, with inflation softening. In the last four months, we have seen CPI (consumer price index) decline three times, including this month. Inflation was expected to increase by 0.3% in October, but it remained negative, declining by 0.1%, after the 0.3% decline we saw last month.

- Eurozone CPI Inflation – Inflation has been weakening in the Eurozone considerably, but in recent months, core CPI has shown some sign of life. Headline CPI fell below 1.0% last month to 0.9%, which was revised lower to 0.8% today. For October, inflation was expected to cool off further to 0.7%, which it did. But, core CPI which was expected to remain unchanged at 1.0% this month after ticking higher from 0.9% last month, beat expectations, coming at 1.1% which is a positive sign.

- Eurozone Flash GDP – The global economy has been weakening for more than a year and the economy of the Eurozone is where the weakness is more evident. The manufacturing and industrial sectors have been in recession for quite some time and the recession is getting deeper, instead of improving. Eurozone GDP in Q2 increased by only 0.2%. For Q3, today’s report was expected to show another slowdown to 0.1%, but it beat expectations, expanding by 0.2%. Italian Q3 GDP was expected to have fallen flat at 0.0%, but it too beat expectations, increasing by 0.1% and Q2 was revised higher as well to 0.1% from 0.0% previously estimated.

- China Doesn’t Feel Optimistic About the Trade Deal – Bloomberg reported earlier that China is casting doubts about reaching a comprehensive long-term trade deal with the US, blaming Trump’s impulsive nature and the risk that he may back out of even the limited deal that both sides are about to sign in the coming weeks. Adding that Chinese officials have warned that they won’t budge on structural issues either, citing people familiar with the matter. Further noting that China is demanding an end to tariffs in order to begin any talks for “Phase Two”.

The US Session

- Canadian GDP Report – The GDP report from Canada was released a while ago and it showed that the Canadian economy returned to growth again in August, after falling flat in July. The GDP increased by 0.1%, missing expectations of 0.2%. GDP YoY remained unchanged at 1.3%, same as in the previous month. Goods producing sector increased by +0.2%. Services-producing by +0.1% which is the 6th consecutive rise. Construction came at +0.3% from -0.7% prior, manufacturing increased by +0.5% vs 0.0% prior. The raw materials price index RPI was much softer at 0.0% against +2.5% expected. Wholesale trade turned negative at -1.3% from +1.1% in July, retail trade increased by +0.3% from +0.1% prior.

- US Personal Spending and Income – Personal income has been strong in the US but it softened in July to just 0.1%. But it returned strong in August, showing a 0.4% increase, which was revised higher to 0.5% today. The income was expected to come at 0.3% for September and it came at 0.3% indeed. Personal spending was revised higher to 0.2% for August as well, from 0.1%. But, today’s report which was for September missed expectations of 0.3% and came at 0.2%.

- Chicago PMI Falls Deeper in Contraction – US Chicago PMI indicator fell into contraction in June and the contraction deepened further in July. It resurfaced in August for a short period but it fell in contraction again to 47.1 points. This month, Chicago PMI was expected to increase slightly to 48.3 points, but it missed expectations and fell deeper into contraction to 43.2 points, justifying Powell’s dovish remarks yesterday.

Trades in Sight

Bullish NZD/USD

- The trend has turned bullish

- The retrace down is complete on the H1 chart

- The 200 SMA has turned into support on the H4 chart

- Fundamentals point up

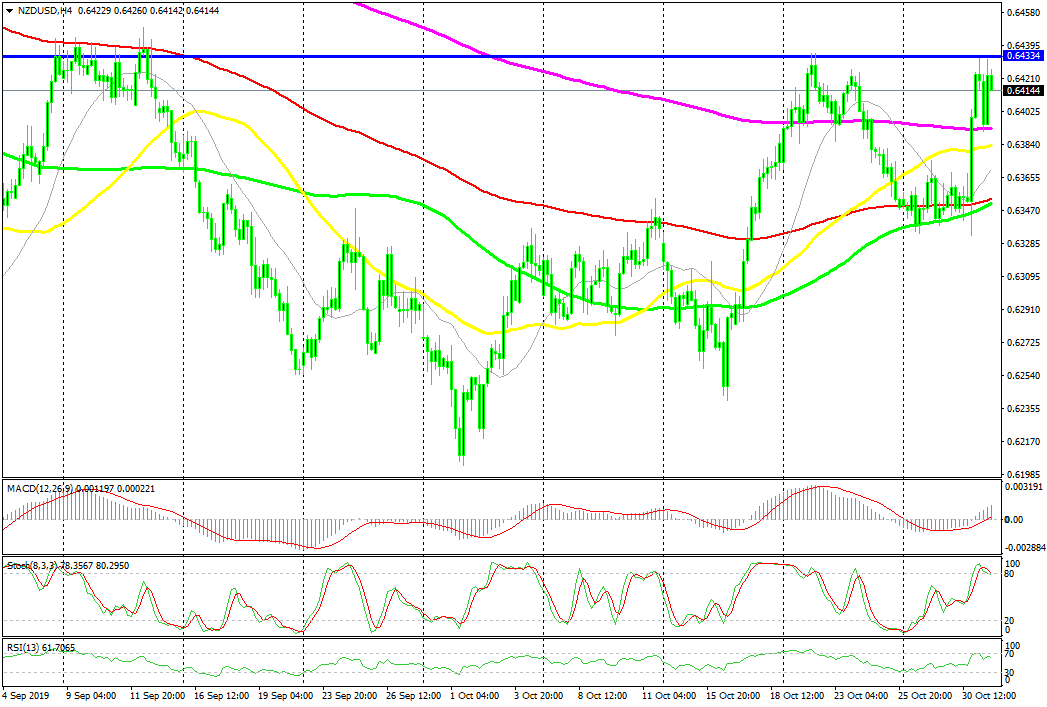

The 200 SMA is providing solid support for this pair

NZD/USD has been bearish for a long time, but it turned higher in the third week of this month after comments that US and China were reaching a partial trade deal. As a result, this pair climbed around 200 pips higher. Although, it retreated lower last week, but the bullish trend resumed again this week. Then, we saw a surge yesterday after Powell’s press conference. Today we saw another pullback lower on the H1 chart, but the retrace was compete earlier on that time-frame, with stochastic being oversold. The 200 SMA (purple) also provided solid support today after the retrace lower this morning and we decided to go long from there.

In Conclusion

The USD turned pretty bearish after the FED press conference yesterday and it continued declining today as well. But, it has turned higher in the last few hours, especially against the Euro. Safe havens on the other hand continue to climb higher as the sentiment remains negative after the comments from China today.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts