Investors Eye Inflation as Gold Slips Toward $4,000 Amid Strong NFP and Middle East Uncertainty

Gold prices came under heavy selling pressure after stronger-than-expected U.S. employment data reinforced expectations of a more hawkish Federal Reserve, while geopolitical developments further strengthened the U.S. dollar and Treasury yields.

Quick overview

- Gold prices fell sharply last week, losing over $200 due to stronger-than-expected U.S. employment data and rising Treasury yields.

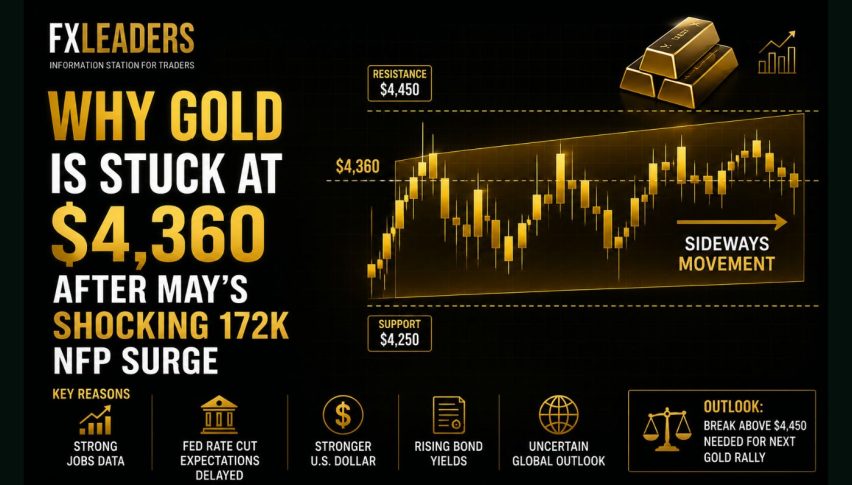

- The U.S. labor market showed unexpected strength with non-farm payrolls increasing by 172,000 jobs in May, leading to reassessed Federal Reserve interest rate expectations.

- Geopolitical tensions, particularly involving the U.S. and Iran, remained high but were overshadowed by the strength of the U.S. dollar.

- Investor focus now shifts to upcoming U.S. inflation reports, which could significantly impact interest rate expectations and gold prices.

Live GOLD Chart

Gold prices came under heavy selling pressure after stronger-than-expected U.S. employment data reinforced expectations of a more hawkish Federal Reserve, while geopolitical developments further strengthened the U.S. dollar and Treasury yields.

Gold Suffers Sharp Weekly Decline

Gold ended last week with significant losses, falling more than $200 as investors reacted to a combination of stronger-than-expected U.S. economic data and shifting geopolitical developments. The decline accelerated on Friday after the May U.S. non-farm payrolls report surprised to the upside, sending the U.S. dollar and Treasury yields sharply higher while reducing demand for non-yielding assets such as gold.

The stronger dollar made gold more expensive for overseas buyers, while rising bond yields increased the opportunity cost of holding bullion, resulting in broad selling pressure across precious metals.

U.S. Labor Market Shows Unexpected Strength

The latest employment report painted a much stronger picture of the U.S. economy than markets had anticipated. Non-farm payrolls increased by 172,000 jobs during May, comfortably exceeding consensus expectations that had generally pointed to gains closer to 125,000.

Adding to the positive surprise, previous months were revised substantially higher. March payroll growth was revised up to 214,000, while April increased to 179,000, representing a combined upward revision of 93,000 jobs. The revisions reversed the recent trend of downward adjustments and reinforced confidence that the labor market remains resilient.

The unemployment rate remained broadly stable at 4.3%, while average hourly earnings rose 0.3% during the month. The average workweek held steady at 34.3 hours, indicating continued stability in labor demand.

Hiring was strongest across leisure and hospitality, local government, and healthcare, while only a handful of sectors, including financial activities and manufacturing, showed modest weakness.

Overall, the report suggested that the U.S. labor market continues to expand despite elevated interest rates, reducing expectations that the Federal Reserve will need to ease monetary policy in the near future.

Markets Reprice Federal Reserve Expectations

The stronger labor market data prompted investors to reassess the outlook for U.S. monetary policy.

Markets have increasingly shifted away from expectations of imminent interest rate cuts, with traders now assigning higher probabilities that the Federal Reserve could keep policy restrictive for longer if inflation remains elevated. The combination of resilient employment and persistent inflation raises concerns that policymakers may have limited room to begin easing monetary policy.

The resulting rise in Treasury yields and the U.S. dollar placed additional pressure on gold, which typically performs better during periods of lower real interest rates and a weaker dollar.

Geopolitical Tensions Continue to Influence Markets

Geopolitical uncertainty also remained firmly in focus, although its traditional support for gold was largely overshadowed by the strength of the U.S. dollar.

Negotiations between the United States and Iran appeared to remain at an impasse over sanctions relief, frozen Iranian assets, and nuclear-related issues. President Trump reiterated that the United States would not unfreeze Iranian assets or lift sanctions before meaningful progress is achieved, while Iranian officials maintained that key demands must be addressed before any broader agreement can move forward.

Meanwhile, tensions in the Middle East remained elevated following renewed military exchanges involving Israel and Hezbollah. Israeli strikes in Beirut’s southern suburbs prompted renewed warnings from Iranian officials, underscoring the fragile regional security environment.

Although geopolitical risks often support safe-haven demand for gold, last week’s stronger U.S. economic data proved to be the dominant market driver.

Technical Analysis—The Support Held

Technically, the correction early in 2026 was severe. Gold broke decisively below its 20-day simple moving average, ending a streak of consistent trend support. Attention quickly shifted to the 50-day moving average near $5,000 which was also broken and in late March we saw a decline below the early February low of $4,400, and XAU bottomed at $4,100.

Gold Chart Daily – Gold Rebounds Off the 100 SMA

Gold found support at the 100 SMA (red) which was broken as support last seek. Gold slipped to $4,318 on Friday, closing below the 100 SMA for the first time since 2023. However the decline stalled at the 50 SMA on the weekly chart (red).

Gold Chart Weekly – The 50 SMA Held As Support

The ability to hold above $4,000 carries psychological importance. Reclaiming such a major round-number threshold often stabilizes sentiment, especially after a period of forced liquidation. While volatility remains elevated, the ability to defend longer-term trend support suggests that structural buyers remain active.

Inflation Data Becomes the Next Major Catalyst

Investor attention now shifts toward this week’s U.S. inflation reports, which could determine whether the recent move in interest rate expectations continues.

The Consumer Price Index (CPI) is expected to show monthly inflation easing to 0.3% in May from 0.6% previously, while annual headline inflation is projected to edge up to 4.2%. Core inflation is expected to increase 0.5% during the month, lifting the annual core rate to 2.9%.

Producer Price Index (PPI) data due later in the week will also be closely monitored, with economists expecting producer prices to remain elevated.

While some analysts believe underlying inflation pressures may begin to moderate, markets remain sensitive to any upside surprises that could reinforce expectations for higher interest rates over an extended period.

Outlook

Gold enters the new trading week under pressure as investors weigh resilient U.S. economic data against persistent geopolitical uncertainty. The stronger labor market has shifted attention back toward inflation and Federal Reserve policy, making this week’s CPI and PPI releases particularly important.

Should inflation remain stubbornly high, expectations for prolonged restrictive monetary policy could continue supporting the U.S. dollar and Treasury yields, limiting gold’s recovery potential. However, any signs of softer inflation or renewed geopolitical escalation could quickly revive safe-haven demand and provide support for bullion prices.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts