AVGO Stock Breaks Below $400 Ignoring JPMorgan Analysts Buy Rating for Broadcom

Broadcom’s sharp reversal below $400 highlights growing investor fatigue with AI-driven valuations, where even strong results are no longer enough to sustain stretched expectations.

Quick overview

- Broadcom's stock has fallen over 20% from recent highs, dropping below $400, as investor optimism around AI-driven valuations wanes.

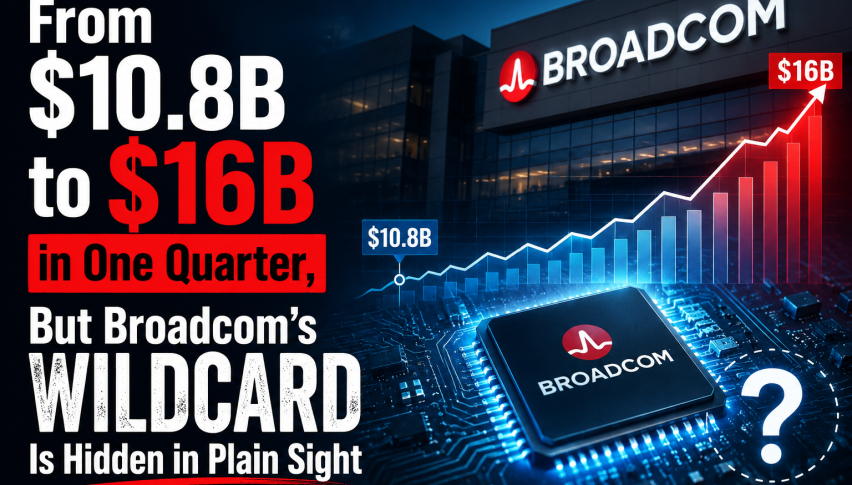

- Despite strong earnings, the company's forward guidance of $16 billion in AI-related revenue for the upcoming quarter disappointed analysts and contributed to the selloff.

- Concerns about financing constraints for large-scale AI infrastructure projects and geopolitical tensions are adding pressure to Broadcom's market sentiment.

- The recent decline reflects a broader market trend of valuation resets across high-multiple AI infrastructure stocks, where even strong results are met with skepticism.

Broadcom’s sharp reversal below $400 highlights growing investor fatigue with AI-driven valuations, where even strong results are no longer enough to sustain stretched expectations.

Broadcom’s Rally Unwinds as AI Narrative Loses Momentum

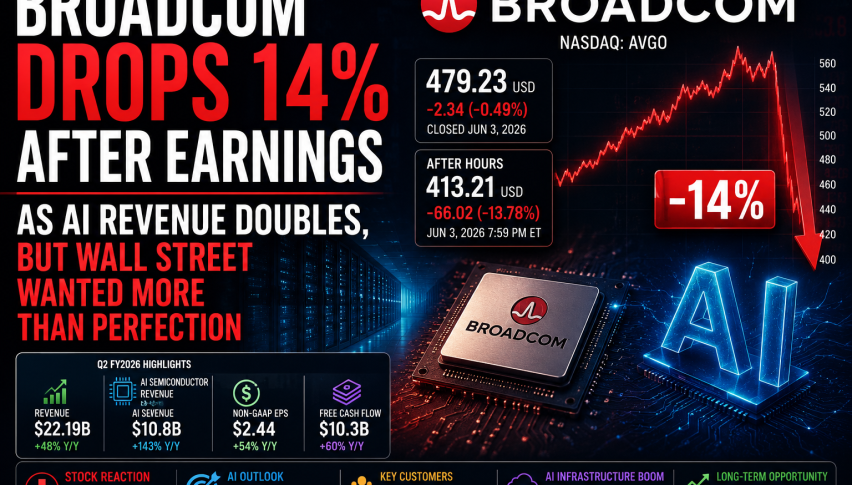

Broadcom has undergone a sharp reversal following its post-earnings reaction, with shares falling more than 20% from recent highs and slipping below the $400 level on Monday. The decline underscores how quickly AI-driven optimism can unravel when forward expectations are no longer supported by incremental upgrades or clearer acceleration in guidance.

Despite reaffirmations from JPMorgan Chase & Co. analysts maintaining a buy rating and defending the company’s position in artificial intelligence infrastructure, sentiment has remained weak. Analysts Harlan Sur and Mayur Ramdhani reiterated that reports suggesting delays or cancellations in Broadcom’s collaboration with Google on next-generation TPU programs were inaccurate, emphasizing that development efforts remain on track with “no delays” and “no cancellations.” However, the market reaction suggests investors are increasingly discounting even high-conviction analyst defenses.

Post-Earnings Breakdown Exposes Elevated Expectations

The selloff marks a dramatic reversal from Broadcom’s earlier rally, which had pushed the stock toward the $495 region before earnings. Initially supported by strong results, the momentum quickly collapsed as investors reassessed whether AI-related growth assumptions had become overly aggressive.

Although the company reported earnings that exceeded Wall Street estimates, the reaction revealed a widening gap between operational performance and investor expectations. What was once viewed as a high-quality beat was instead interpreted as insufficient to justify already stretched valuations.

The decline accelerated as positioning unwound, highlighting how concentrated optimism had become across semiconductor and AI infrastructure names.

Technical Analysis – The 50 SMA Acting as Resistance

Broadcom entered the new year on uncertain footing, with its share price dipping below $300 as confidence across the semiconductor complex began to fray. But we saw a strong surge inn April and after a consolidation above the 20 daily SMA for a few weeks, AVGO stock resumed the uptrend and approached $500 in early June before reversing down and falling below the 50 daily SMA and below $400. We saw a weak attempt to rebound last week but today’s reversal confirms the selling bias in AVGO.

AVGO Chart Daily – Returning to the 100 SMA

Guidance Disappointment Drives Sentiment Reset

The core trigger for the reversal was Broadcom’s forward guidance, which failed to meet elevated expectations. The company projected approximately $16 billion in AI-related revenue for the upcoming quarter, below consensus forecasts of roughly $17.3 billion.

While still reflecting strong underlying demand, the figure signaled that near-term acceleration may be more gradual than the market had priced in. Management also maintained its long-term AI revenue target of over $100 billion by fiscal 2027 without raising it further, reinforcing the perception that expectations had peaked for now.

This lack of upward revision became a focal point for investors, prompting immediate profit-taking after a period of aggressive multiple expansion.

Supply Constraints and Macro Headwinds Add Pressure

Analysts have suggested that Broadcom’s constraints are largely supply-driven rather than demand-related, but this distinction has done little to stabilize sentiment. In a market increasingly conditioned for accelerating growth, steady execution is no longer sufficient to support elevated valuations.

At the same time, broader semiconductor sentiment has weakened amid rising geopolitical friction. Escalating U.S.-China tensions and tightening export restrictions continue to cloud visibility for chipmakers exposed to global AI infrastructure demand. These pressures are particularly relevant for companies like Broadcom that sit at the center of advanced semiconductor supply chains.

Financing Uncertainty Raises Additional Concerns

Further unease has emerged from reports that large-scale AI infrastructure initiatives, including projects linked to OpenAI, may be facing financing constraints tied to multibillion-dollar chip development programs. These concerns have raised broader questions about the sustainability of the current AI capital expenditure cycle.

If funding conditions tighten, the ripple effect could slow hardware demand growth and delay deployment timelines across the broader ecosystem, adding another layer of uncertainty to an already fragile sentiment backdrop.

Valuation Reset Becomes the Dominant Force

Ultimately, Broadcom’s reversal reflects a broader repricing across high-multiple AI infrastructure stocks. After a powerful run-up driven by expectations of uninterrupted AI acceleration, the bar for earnings has shifted dramatically higher.

Even strong results are now being met with skepticism if they fail to materially exceed already aggressive forecasts. The latest decline below $400 highlights a market increasingly focused on valuation compression rather than narrative expansion, where execution is no longer enough to sustain prior enthusiasm.

Broadcom Q1 Earnings Report

-

- Revenue: $22.19 billion, 48% year-over-year growth

- Earnings: Adjusted $2.44 per share vs. $2.39 expected

- Semiconductor Solutions: $15.01 billion

- Infrastructure Software: ($7.18 billion

- AI Revenue: ($10.8 billion, 143% increase year-over-year

Forward Guidance & Analyst Sentiment

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts