Nvidia NVDA Stock Heads Below $200 as Costs, Competition, and Politics Weigh

Nvidia’s retreat from recent highs reflects mounting skepticism that even industry-leading innovation can sustain its valuation amid rising costs, geopolitical friction, and fading AI euphoria.

Quick overview

- Nvidia's stock has declined sharply from recent highs, reflecting growing skepticism about its ability to sustain high valuations amid rising costs and geopolitical tensions.

- Despite the launch of the Vera Rubin platform, market reaction has been muted, indicating a disconnect between product innovation and stock performance.

- Nvidia's expansion into the personal computing market introduces competitive risks, as it faces established players like Intel and AMD in a lower-margin sector.

- Overall, the semiconductor sector is experiencing a valuation reset, with investors increasingly focused on sustainability and profitability rather than just growth.

Nvidia’s retreat from recent highs reflects mounting skepticism that even industry-leading innovation can sustain its valuation amid rising costs, geopolitical friction, and fading AI euphoria.

Nvidia’s Rally Loses Momentum as Sentiment Turns Cautious

Nvidia has seen a notable reversal over the past two weeks, with shares sliding sharply toward the $200 level after failing to sustain momentum above $230. The decline marks a clear shift in investor psychology, as markets increasingly question whether the semiconductor leader can maintain the extraordinary pace of growth that powered its historic rally.

Despite continued technological leadership and headline innovation, sentiment has deteriorated as expectations have moved further ahead of fundamentals. Even major product announcements have failed to generate lasting upside, suggesting that the stock’s valuation is now being judged more harshly against a much higher bar for performance.

Vera Rubin Platform Fails to Sustain Market Optimism

Recent attention centered on Nvidia’s unveiling of its next-generation Vera Rubin platform at the ISC High Performance 2026 conference in Hamburg. The system was positioned as a major leap forward in AI computing infrastructure, described as a foundation for “world-class supercomputers for science,” delivering more than 7 exaflops of AI performance, 5 petaflops of FP64 compute, and support for up to 144 GPUs per rack.

CEO Jensen Huang framed the platform as “a new instrument for science,” reinforcing Nvidia’s ambition to remain at the center of global AI infrastructure development. The company also outlined an extensive ecosystem of partners including Bull, Dell, GIGABYTE, HPE, and Supermicro, signaling a broad supply chain rollout of Vera Rubin NVL4 systems.

However, despite the technical scale of the announcement, market reaction was muted. Rather than driving a sustained rally in Nvidia itself, the announcement triggered a fragmented response across the supply chain, exposing a growing disconnect between product innovation and equity performance.

Supply Chain Winners Mask Underlying Weakness

While Nvidia’s own shares struggled to gain traction, several suppliers initially benefited from the announcement. Super Micro Computer surged double digits after detailing a liquid-cooled infrastructure design capable of scaling to large GPU deployments. Dell Technologies also advanced on server deployment expectations tied to major U.S. government supercomputing projects.

Memory and component suppliers saw similar speculative inflows, with Micron Technology gaining ahead of earnings amid rising expectations for AI-driven memory demand, while SanDisk and Intel also participated in the broader rotation into hardware-linked names.

Yet this rotation highlighted a critical contradiction: Nvidia itself remained flat to lower, while the Nasdaq index weakened, pressured by declines in software and platform leaders such as Alphabet and Microsoft. The result was not a broad tech rally, but a narrow repositioning into infrastructure suppliers at the expense of software-heavy incumbents.

Expansion Into PCs Introduces New Competitive Pressure

Nvidia’s push into personal computing with the RTX Spark processor has added a new dimension to its growth strategy, but also introduces additional competitive risks. Unlike the company’s dominant position in data-center AI accelerators, the PC market is mature, highly competitive, and structurally lower in margins.

This expansion places Nvidia in direct competition with entrenched players such as Intel and AMD, where pricing pressure and cyclical demand patterns are more pronounced. Investors are increasingly questioning whether Nvidia’s data-center dominance can translate into sustained success in consumer computing, or whether it represents a dilution of focus at a critical stage in the AI cycle.

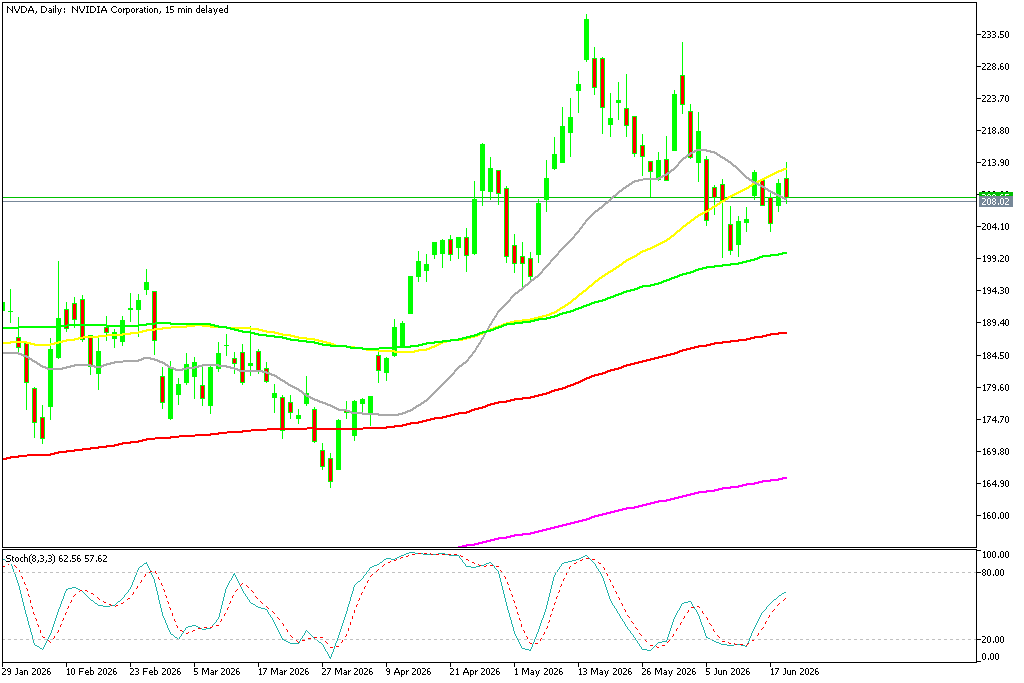

Technical Picture Reflects Volatility

Nvidia’s technical setup mirrors the shifting sentiment. The stock slipped to its 20-day simple moving average (gray) in early May, but reversed back up, so it provided reliable support and NVDA reached a new high of $236 last week before earnings. But then the stock reversed down and sellers tested the 20 SMA again just above $200 but it held, but now the price is heading there again and will likely fall below $200 if the 100 SMA breaks.

NVDA Chart Daily – Failing at the 50 SMA

AI Spending Cycle Under Increasing Scrutiny

Across the semiconductor sector, confidence in the durability of the AI investment cycle is beginning to weaken. Recent cautious commentary from Broadcom regarding AI revenue expectations reinforced concerns that growth rates may be peaking after an extended period of acceleration.

This shift has contributed to a broader reassessment of valuation assumptions across AI-linked equities. Investors are becoming less focused on peak revenue figures and more concerned with whether current capital expenditure levels across hyperscale cloud providers can be sustained.

Strong Earnings No Longer Drive Upside

Despite delivering exceptional financial results, Nvidia’s earnings reports have increasingly failed to generate sustained upside momentum. The company recently reported revenue of $81.6 billion for its fiscal first quarter, driven by continued strength in data-center demand and AI infrastructure investment.

However, the market reaction was subdued, reflecting a structural change in expectations. Strong results are no longer viewed as a catalyst for re-rating but rather as a baseline requirement. This dynamic leaves less room for positive surprises and increases vulnerability to even minor disappointments.

Rising Costs and Geopolitical Constraints Add Pressure

Cost inflation is also becoming a growing concern. Operating expenses have risen as Nvidia continues to invest heavily in advanced chip design, networking infrastructure, and AI platform expansion. While these investments are necessary to maintain technological leadership, they also increase the burden required to sustain future profitability.

At the same time, U.S. export restrictions on advanced semiconductor sales to China continue to limit access to a critical end market. This forces Nvidia to rely more heavily on a concentrated base of North American hyperscale customers, increasing exposure to any slowdown in cloud infrastructure spending.

Valuation Reset Becomes the Dominant Theme

Ultimately, Nvidia’s recent decline reflects a broader valuation reset across high-growth AI equities. After a historic rally driven by accelerating demand expectations, the market is now applying stricter scrutiny to sustainability, profitability, and execution risk.

Even with continued leadership in AI computing, the stock faces a more challenging environment where innovation alone is no longer sufficient. Investors are demanding sustained outperformance across revenue, margins, and demand visibility—leaving significantly less room for disappointment in an already stretched valuation framework.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts