AAPL Stock Tests Record Highs as Apple AI Strategy and Citi’s $365 Target Fuel Breakout

Apple stock AAPL holds near record highs as Citi’s $365 target, AI optimism and iPhone catalysts keep buyers in control.

Quick overview

- Apple shares are nearing record highs due to strong iPhone demand, advancements in on-device AI, and a leadership transition to John Ternus.

- Citi has upgraded Apple's price target to $365, citing the company's premium brand and ability to raise prices to offset rising costs.

- Apple's focus on on-device AI and privacy is seen as a competitive advantage, potentially enhancing user engagement and services revenue.

- Despite the positive outlook, Apple faces legal and regulatory risks, and investors are awaiting confirmation of strong earnings to justify the stock's premium valuation.

Apple shares remain near fresh highs as investors price in stronger iPhone demand, on-device AI progress, and a major leadership transition under incoming CEO John Ternus.

Apple Rally Extends as Buyers Defend Breakout Momentum

Apple has staged one of the strongest reversals among major technology stocks, climbing to fresh 52-week highs even as parts of the broader tech sector remain under pressure.

The stock briefly traded above $323 on Monday before closing at $317.31, keeping AAPL close to record territory. TradingView data shows Apple is now up more than 16% year to date and more than 50% over the past year, while its market capitalization stands around $4.63 trillion.

The rally marks a sharp change in sentiment. Earlier this year, investors questioned whether Apple had fallen behind in artificial intelligence while competitors committed enormous sums to cloud infrastructure and generative AI data centers.

Now the market appears to be rewarding Apple’s different approach: less capital-intensive, more device-focused, and built around its installed base of more than 2 billion users.

Citi Upgrade Strengthens Apple’s Bullish Narrative

The latest catalyst came from Citi, which raised its Apple price target to $365 from $315 while maintaining a Buy rating.

The firm argued that Apple’s premium brand, loyal customer base and design-driven demand should help the company continue gaining share even in a weaker smartphone and PC market. Analysts also pointed to Apple’s ability to raise prices selectively to offset higher memory and component costs.

That pricing power matters because Apple recently increased prices on several products to protect margins from rising DRAM and NAND costs. Investors now appear more confident that demand can withstand those price increases, especially if new AI features and hardware upgrades support another product cycle.

Citi also highlighted Apple’s September launch event as a major catalyst, with the next iPhone lineup and AI-enhanced Siri features expected to shape investor sentiment into the second half of 2026.

John Ternus Transition Adds Product-Focused Upside

Apple’s leadership transition is also becoming part of the bull case.

Tim Cook is expected to hand over the CEO role to John Ternus, Apple’s hardware engineering chief, while staying on as chairman. Investors increasingly view this structure as a potential “best of both worlds” setup.

Cook’s continued presence may help Apple navigate tariffs, regulatory pressure, supply-chain risk and geopolitical uncertainty. Meanwhile, Ternus brings deep product and hardware experience at a time when Apple is trying to define its role in the AI era.

The timing is important. Apple’s next product cycle could include major iPhone 18 Pro upgrades, a foldable iPhone, AI glasses, upgraded iPads, camera-equipped AirPods and broader on-device AI features.

If Apple can combine hardware innovation with improved Siri and Apple Foundation Models, the company may convince investors that it can build an AI cycle without matching the spending intensity of Microsoft, Amazon, Meta or Alphabet.

On-Device AI Becomes Apple’s Differentiator

Apple’s AI strategy remains very different from the rest of the Magnificent 7.

Instead of leading with massive cloud infrastructure spending, Apple is focusing on privacy, silicon efficiency, on-device models and deeper integration across hardware, software and services. Recent reports around Apple Foundation Models and possible work with AI model-compression technology have strengthened the view that Apple may pursue a more efficient path.

The market is beginning to treat this as an advantage rather than a weakness.

If AI features run effectively on Apple devices, the company could improve user engagement, support services revenue, and encourage upgrades across iPhone, Mac, iPad and wearables. That would allow Apple to monetize AI through its ecosystem rather than through large external cloud spending.

This is why investors are watching Siri closely. A meaningful AI Siri upgrade could become one of the most important product catalysts in Apple’s next cycle.

Services Growth Supports AAPL’s Premium Valuation

Apple’s Services business remains a major reason investors are willing to pay a premium valuation.

TradingView lists Apple’s trailing P/E ratio near 38, reflecting a valuation that is no longer cheap. However, the company’s high-margin services engine continues to support that multiple.

Recent data cited in supplied notes showed Services revenue near $31 billion for the quarter, with very high gross margins. This recurring revenue base gives Apple a more stable earnings profile than many hardware-dependent companies.

The company also benefits from a dividend yield near 0.34%, strong cash generation, deep ecosystem loyalty and a global installed base that keeps feeding App Store, iCloud, payments, licensing, subscriptions and other services revenue.

Apple’s Legal and Regulatory Risks Remain

The rally is not without risks.

Apple recently filed a federal complaint against OpenAI, io Products and former Apple employees, alleging trade-secret misappropriation tied to hardware design, manufacturing and unreleased intellectual property. OpenAI has denied interest in other companies’ trade secrets, but the lawsuit adds another complication to Apple’s broader AI push.

Regulatory pressure also remains a concern, particularly in Europe, where Apple continues to face scrutiny over App Store rules and iOS ecosystem control.

At the same time, valuation leaves less room for error. Apple is trading near record highs, and analyst consensus targets are not far above the current price, even after Citi’s more bullish $365 target.

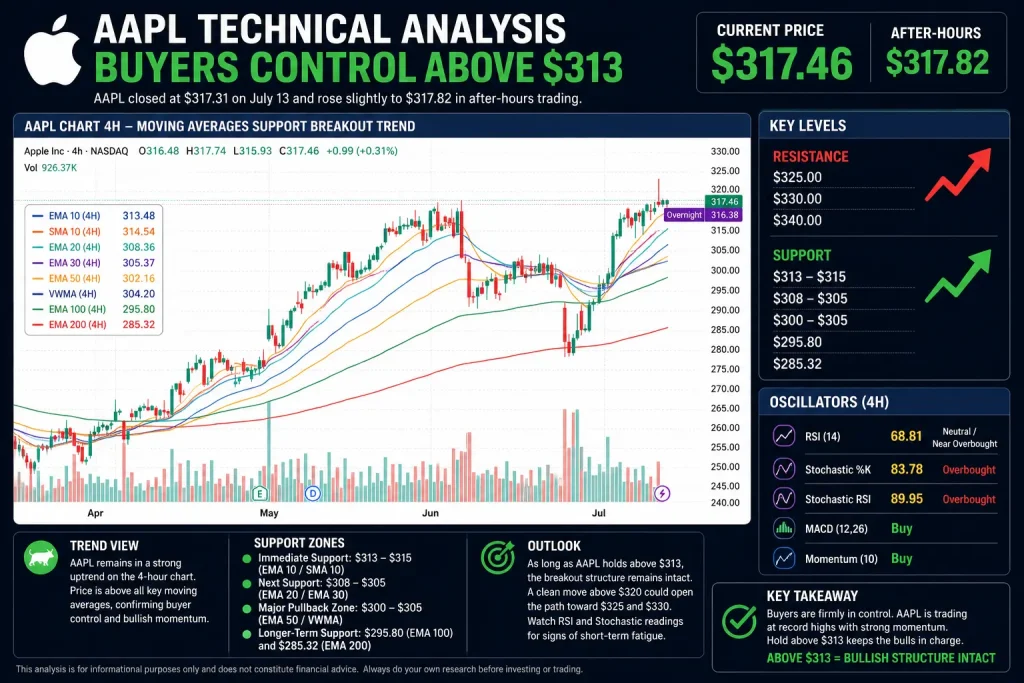

AAPL Technical Analysis: Buyers Control Above $313

AAPL closed at $317.31 on July 13 and rose slightly to $317.82 in after-hours trading.

AAPL Chart 4H – Moving Averages Support Breakout Trend

The 4-hour chart remains firmly bullish. Apple is trading above every major moving average listed, confirming that buyers remain in control.

The 10-period EMA sits near $313.48, while the 10-period SMA is around $314.54. These levels form immediate support. As long as Apple holds above the $313-$315 zone, the short-term breakout structure remains intact.

Below that, the 20-period EMA near $308.36 and the 30-period EMA near $305.37 create the next support band. The 50-period EMA near $302.16 and VWMA near $304.20 reinforce the broader $300-$305 area as a major pullback zone.

Longer-term support remains much lower, with the 100-period EMA at $295.80 and the 200-period EMA at $285.32.

Oscillators show strong momentum but also warn that the stock is becoming extended. RSI is at 68.81, just below overbought territory, while Stochastic %K is at 83.78 and Stochastic RSI is near 89.95. Momentum and MACD both remain on buy, confirming that upside pressure is still active.

Key Levels to Watch

The first upside level is the recent high near $323.45. A clean break above that area could open the door toward $330, followed by $345 if earnings and September product expectations continue improving.

Above that, Citi’s $365 target becomes the longer-term bullish reference point.

On the downside, $313-$315 is the first support zone. A break below that area could bring $308 into focus, followed by the important $300-$305 moving-average cluster.

A deeper pullback toward $296 would still leave the broader uptrend intact, but it would suggest that investors are no longer willing to chase Apple near record highs without fresh earnings confirmation.

Apple Set for a Strong Breakout, But Earnings Must Confirm It

Apple has regained investor confidence by combining strong iPhone demand, pricing power, services growth, AI optimism and a product-focused leadership transition.

The company’s decision to avoid the heaviest parts of the AI infrastructure spending race is now being viewed as a potential advantage, especially while other mega-cap tech names face scrutiny over capex returns.

However, the stock’s strength also raises the bar. With AAPL trading near record highs and at a premium valuation, investors will need confirmation from July 30 earnings that revenue growth, margins, services momentum and product demand remain strong.

For now, Apple’s technical setup remains bullish above $313-$315. A breakout above $323.45 could extend the rally toward $330 and $345, while a failure to hold $308-$313 would suggest the stock needs a pause before the next catalyst.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts