NFLX Stock Tests $70 Support as Netflix Earnings Put Ad Growth and Engagement Fears in Focus

Netflix stock NFLX holds near $74 before Q2 earnings as ad growth and strong FCF battle engagement fears and weak technicals.

Quick overview

- Netflix shares are under pressure ahead of Q2 earnings, trading near 52-week lows amid concerns over engagement and competition.

- Analysts remain broadly positive, with average price targets around $113, but recent declines have made investors cautious.

- The company's advertising business is seen as a potential growth driver, with over 250 million monthly active users, but engagement trends need to stabilize.

- Investors are focused on Q2 revenue and guidance, as a strong report could lead to a rebound, while any shortfalls may keep the stock near recent lows.

Netflix shares remain under pressure ahead of Q2 earnings as investors weigh strong free cash flow and ad-tier growth against weakening engagement trends.

Netflix Nears 52-Week Lows Ahead of Q2 Earnings

Netflix will report second-quarter earnings after the market close on Thursday, July 16, in one of the most important updates for the stock this year.

NFLX has fallen sharply from its April highs and is now trading near $74, only slightly above its 52-week low of $70.86. The decline reflects growing concern that the company’s growth story is shifting from clear streaming dominance toward a more complicated debate around engagement, advertising, pricing and competition.

Wall Street still remains broadly positive. Analyst price targets cited in the supplied notes sit around $113 on average, implying significant upside from current levels. However, the market has become less willing to give Netflix the benefit of the doubt after the stock fell following each of its last four earnings reports.

Engagement Concerns Replace Growth Optimism

The biggest concern heading into earnings is engagement.

Recent reports suggested Netflix executives have discussed adding live, continuously streamed TV channels and bundling third-party apps, including Peacock, to keep viewers spending more time on the platform.

That discussion has raised questions about whether Netflix’s core engagement trends are weakening. Nielsen data cited in the supplied material showed Netflix’s U.S. TV viewing share recently slipped to 7.8%, a multi-year low.

Investors are also watching whether the FIFA World Cup, rising competition from YouTube, and price increases have pressured subscriber activity during the quarter.

Netflix is still the leading global streaming platform, but the market is increasingly asking whether user growth and pricing power can continue without stronger engagement.

Advertising Business Could Offset Subscriber Pressure

The bullish case remains focused on advertising.

Netflix’s ad tier now has more than 250 million monthly active users, giving the company a large and growing base for monetization. Several analysts argue that the ad business is becoming large enough to support both revenue growth and margin expansion, even if subscriber growth slows.

Wedbush has argued that Netflix’s ad business is “outrunning the engagement story,” with better targeting, higher ad load, live sports pricing and international expansion all supporting future growth.

Netflix is also expected to expand its ad tier into additional markets, which could help offset slower paid membership growth and pressure from price-sensitive consumers.

For investors, the key question is whether management can show that advertising is becoming a real profit driver rather than just a defensive response to slower engagement.

Free Cash Flow Keeps NFLX Valuation Debate Alive

Netflix’s free cash flow remains a major support for the stock.

The company has raised its 2026 free cash flow outlook to roughly $12.5 billion, partly helped by termination-fee proceeds tied to its exit from the Warner Bros. Discovery process. Even excluding one-time benefits, Netflix continues to generate strong cash flow relative to many media peers.

Some valuation-focused investors now argue that the stock looks too cheap after the pullback. NFLX is trading around the low-to-mid 20s on forward earnings, a level not seen often since the 2022 bear market.

That valuation reset is attracting buyers, especially with Netflix still expected to generate double-digit revenue growth and operating margins above 30%.

However, the stock may need a clean earnings report and reassuring guidance before investors fully reward the free cash flow story again.

Netflix Earnings: Q2 Numbers and Guidance in Focus

Consensus estimates call for Q2 revenue of about $12.57 billion, representing 13.5% annual growth. EPS is expected around $0.79, while Netflix has guided for an operating margin near 32.6%.

The company has also reaffirmed full-year revenue guidance of $50.7 billion to $51.7 billion and an operating margin target of 31.5%.

Still, Q3 guidance may matter more than Q2 results. Investors want to know whether engagement softness, World Cup-related viewing competition, recent price increases and content amortization costs will pressure the second half of the year.

If Netflix maintains or raises its full-year framework, the stock could rebound sharply. But any shortfall in revenue, engagement commentary or margin outlook could keep NFLX stuck near recent lows.

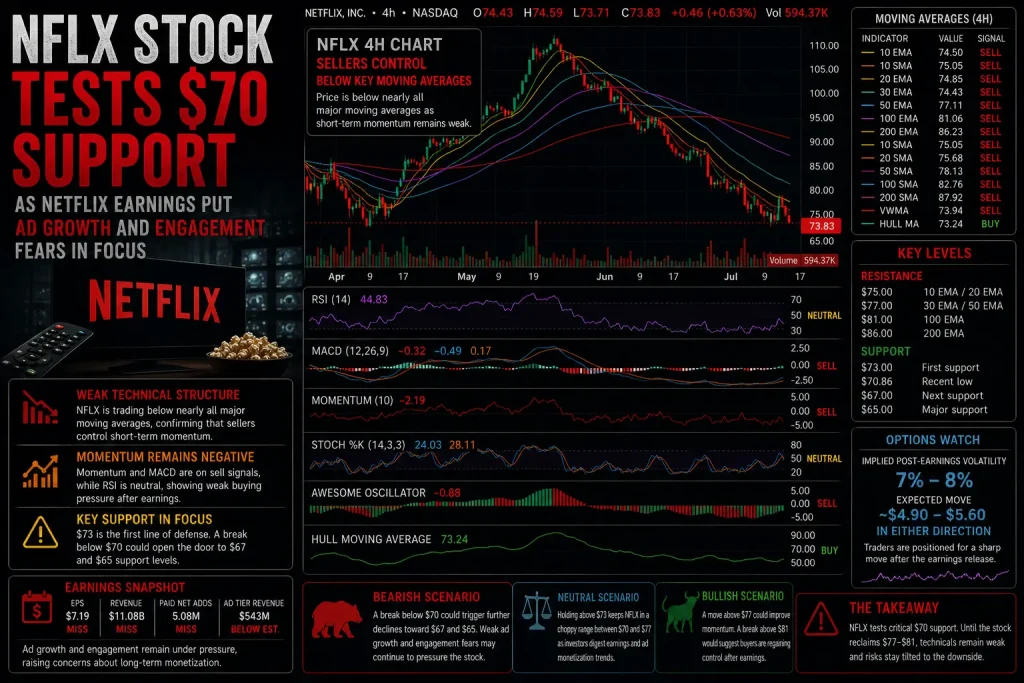

NFLX Technical Analysis: Sellers Control Below $75

NFLX closed at $73.83 on July 13, up 0.63%, before rising slightly to $74.12 in after-hours trading.

NFLX Chart 4H – Stock Struggles Below Key Moving Averages

The 4-hour chart remains technically weak. Netflix is trading below nearly all major moving averages, confirming that sellers still control short-term momentum.

The 10-period EMA sits near $74.50, while the 20-period EMA stands around $74.85. These levels form immediate resistance. Above that, the 30-period EMA near $75.43 and the 50-period EMA near $77.11 create the next recovery zone.

Longer-term resistance remains much higher, with the 100-period EMA near $81.06 and the 200-period EMA around $86.23. Until NFLX reclaims at least the $77-$81 area, the broader technical structure remains fragile.

Oscillators are mostly neutral but soft. RSI stands at 44.83, while Stochastic %K is at 24.03, suggesting the stock is weak but not deeply oversold. Momentum and MACD both remain on sell, confirming that upside pressure has not yet returned.

The Hull Moving Average near $73.24 is the only major indicator showing a buy signal, suggesting buyers are trying to defend the current area.

Key Levels to Watch

The first support level is $73, followed by the recent low zone near $70.86. A decisive break below $70 would be technically damaging and could open the door toward $67 and $65.

On the upside, buyers need to reclaim $75 first. A move above $77 would improve the short-term setup, while a break above $81 would suggest that earnings have helped shift momentum back toward the bulls.

Options traders are also positioning for a sharp move, with implied post-earnings volatility near 7%-8%. That means the stock could quickly test either the $70 support area or the $80 resistance zone after results.

Netflix Has Strong Cash Flow, But Engagement Must Stabilize

Netflix enters earnings with a divided setup.

The company still has scale, strong margins, major free cash flow, a growing advertising business and broad analyst support. At current levels, valuation has become more attractive after the steep decline.

However, investors remain cautious because the engagement debate has not been resolved. If management cannot convincingly explain how advertising, live programming, pricing and content strategy will sustain growth, the stock may struggle to recover even with solid financial results.

For now, NFLX remains vulnerable below $75-$77. Holding the $70-$73 support zone would keep the rebound case alive, but a break below $70 could trigger another leg lower. A strong Q2 report with confident ad and margin commentary could put $80-$81 back in play quickly.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts

Ava