Adobe is set to report its fiscal second-quarter results on June 11, with a focus on AI revenue growth amid a challenging market environment.

The company recently acquired Semrush for $1.9 billion to enhance its digital marketing capabilities and integrate AI tools into its existing ecosystem.

Adobe has authorized a $25 billion share repurchase program, signaling management's confidence in the stock despite ongoing investment in AI.

Investors are closely watching key metrics related to AI monetization, as the upcoming earnings report could significantly impact Adobe's stock valuation.

Adobe enters one of its most important earnings weeks in years.

The software giant reports fiscal second-quarter results on June 11 amid mounting pressure to prove that its artificial intelligence investments can translate into meaningful revenue growth. Investors are also assessing Adobe’s $1.9 billion acquisition of Semrush, a new $25 billion share repurchase authorization, and an ongoing CEO succession process.

The stakes are high.

Adobe shares have fallen roughly 25% year-to-date and nearly 40% over the past 12 months, making it one of the weakest-performing large-cap software companies despite aggressive AI product launches.

Adobe’s AI Monetization Story Faces a Critical Test

Wall Street expects:

Revenue: $6.46 billion

Adjusted EPS: $5.83

Earnings release: June 11 after market close

Adobe has consistently beaten earnings expectations, surpassing EPS estimates for eight consecutive quarters.

This time, however, investors want more than another modest beat.

The market is looking for evidence that Adobe’s AI products are becoming significant revenue drivers rather than simply improving user engagement.

Key metrics to watch include:

AI-first ARR growth

Firefly monetization

Digital Media ARR growth

Subscription revenue trends

Full-year guidance

Enterprise adoption of GenStudio and Acrobat AI Assistant

A strong report could help restore confidence in Adobe’s AI strategy.

A disappointing ARR update could reinforce concerns that AI adoption is growing faster than monetization.

Semrush Acquisition Expands Adobe’s AI Marketing Ambitions

Adobe recently agreed to acquire Semrush in a transaction valued at approximately $1.9 billion.

The deal gives Adobe deeper exposure to:

Search marketing

SEO analytics

Performance advertising

Digital marketing intelligence

Enterprise marketing workflows

Management appears to be positioning Adobe as an end-to-end content creation and marketing platform.

The acquisition complements products such as:

Firefly

GenStudio

Experience Cloud

Creative Cloud

Acrobat AI Assistant

The strategy is designed to connect content creation directly with campaign performance and customer acquisition data.

However, integration risks remain.

Investors will closely monitor how Adobe combines Semrush’s marketing tools with its existing ecosystem while navigating a leadership transition.

Adobe’s Massive Buyback Signals Confidence

Adobe also authorized a new $25 billion multi-year share repurchase program.

The announcement surprised many investors given ongoing AI investment requirements and the Semrush acquisition.

The move sends a clear signal that management believes the stock is undervalued after its prolonged decline.

Supporters view the buyback as an efficient use of capital.

Critics argue the company may eventually need more financial flexibility if AI competition intensifies.

AI Commercialization the Key Investment Debate for Adobe Stock

Adobe has spent the past year embedding AI capabilities across its product portfolio.

Firefly is now integrated into:

Photoshop

Illustrator

Premiere Pro

Acrobat

Adobe Express

The company previously disclosed:

AI-first ARR more than doubled year-over-year

Firefly ARR exceeded $250 million

Creative Cloud monthly active users surpassed 80 million

Yet investors continue to question whether those figures are large enough relative to Adobe’s overall business.

The next phase is monetization.

If AI products begin driving higher subscription tiers, enterprise spending, and stronger ARR growth, Adobe’s valuation could improve substantially.

If not, competitive concerns involving Microsoft, Salesforce, Alphabet, and OpenAI could continue weighing on sentiment.

How to trade Adobe earnings this week

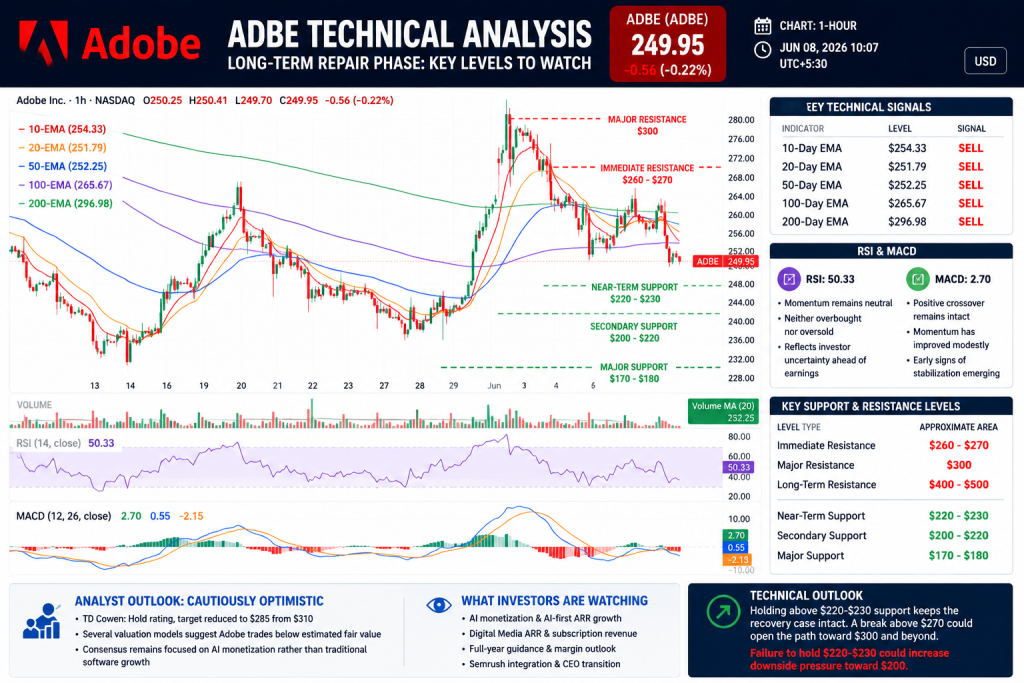

ADBE Technical Analysis: Stock Remains in a Long-Term Repair Phase

Adobe’s technical picture remains mixed.

The stock has stabilized after months of selling pressure but continues trading below several important long-term trend indicators.

Key Technical Signals

Indicator

Level

Signal

10-Day EMA

$254.33

Sell

20-Day EMA

$251.79

Sell

50-Day EMA

$252.25

Sell

100-Day EMA

$265.67

Sell

200-Day EMA

$296.98

Sell

Unlike many AI-linked software peers, Adobe remains below its 100-day and 200-day moving averages.

This suggests the stock is still attempting to establish a durable bottom rather than participating in a fully confirmed uptrend.

RSI and MACD

RSI: 50.33

Momentum remains neutral

Neither overbought nor oversold

Reflects investor uncertainty ahead of earnings

MACD: 2.70

Positive crossover remains intact

Momentum has improved modestly

Early signs of stabilization are emerging

The combination suggests Adobe is consolidating rather than breaking down, but earnings will likely determine the next major move.

Key Support and Resistance Levels

Level Type

Approximate Area

Immediate Resistance

$260-$270

Major Resistance

$300

Long-Term Resistance

$400-$500

Near-Term Support

$220-$230

Secondary Support

$200-$220

Major Support

$170-$180

A sustained move above $270 could strengthen the case for a broader recovery. Failure to hold the $220-$230 area could increase downside pressure.

Analysts Remain Divided on Adobe (ADBE) Stock

Wall Street remains cautiously optimistic.

Recent analyst actions include:

TD Cowen: Hold rating, target reduced to $285 from $310

Several valuation models suggest Adobe trades below estimated fair value

Consensus remains focused on AI monetization rather than traditional software growth

The market appears willing to reward evidence that Adobe can convert AI engagement into durable revenue growth.

Long-Term Outlook: Adobe Still Owns Valuable Assets, But Execution Matters

Adobe remains one of the most dominant software franchises in digital creativity and document management.

Its ecosystem spans creative tools, enterprise marketing, digital documents, and now search marketing through Semrush.

The challenge is no longer product innovation.

The challenge is proving that AI can accelerate revenue growth enough to offset competitive pressures and justify a higher valuation.

The June 11 earnings report may provide the clearest indication yet of whether Adobe’s AI strategy is becoming a meaningful financial engine—or whether investors will need to wait longer for that transformation to materialize.

Lead Markets Analyst – Multi-Asset (FX, Commodities, Crypto)

Arslan Ali Butt serves as the Lead Commodities and Indices Analyst, bringing a wealth of expertise to the field. With an MBA in Behavioral Finance and active progress towards a Ph.D., Arslan possesses a deep understanding of market dynamics.

His professional journey includes a significant role as a senior analyst at a leading brokerage firm, complementing his extensive experience as a market analyst and day trader. Adept in educating others, Arslan has a commendable track record as an instructor and public speaker.

His incisive analyses, particularly within the realms of cryptocurrency and forex markets, are showcased across esteemed financial publications such as ForexCrunch, InsideBitcoins, and EconomyWatch, solidifying his reputation in the financial community.