US Session Forex Brief, Jan 30 – Hanging on the Sidelines Ahead of the FED Meeting

Markets are waiting for the FED meeting this evening, although we are seeing some position adjustment from traders right now

Today is that time of the month again when the Federal Reserve meets to discuss the economic outlook and they decide on interest rates. For this reason, the financial markets have been pretty quiet today. Although, Brexit doesn’t let things get too boring. Yesterday, the British Parliament passed some of the amendments which diminish the chances of a no-deal Brexit.

On the other hand, it means that the UK government will ask for an extension of Article 50. This seems like a positive outcome, but it also stretches the period of uncertainty further which is bad for the British economy and for investment. Hence the 150 pip decline in GBP/USD yesterday in the evening. Although, the European and Irish officials repeated today that the Brexit deal won’t be renegotiated, so no one knows how this will end up.

But the price action overall has been pretty quiet as the FED meeting approaches. The FED sounded less hawkish in their last statement in December after hiking interest rates for the fourth time last year. That gave the market a reason to think that the FED will be less aggressive with interest rates this year.

The press conference from chairman Powell, as well as comments from other FED members, have assured markets that the FED will slow the pace of rate hikes this year and right now the markets are pricing in two rate hikes for this year. But, nothing is too certain in forex, and traders are staying on the sidelines today to see if the FED will confirm this view or whether they will sound less dovish today, which would give the USD some support in the near term.

- French Flash GDP – The economy grew by 0.4% in Q3 last year in France as expected, although it was revised lower today to 0.3%. The GDP was expected to grow by 0.2% in Q4, but it beat expectations, coming at 0.3% which was a bit of a surprise.

- German GfK Consumer Climate – This consumer climate indicator has been steady at around 10.5 points in Germany. This month. the GfK consumer climate was expected to cool off to 10.3 points but it became stronger coming at 10.8 points. But, this will surely weaken in the coming months as manufacturing slows down in Germany and across Europe.

- German Import Prices – Import prices turned negative in November declining by 1.0% that month as Oil prices had tumbled during the last two months. Import prices were expected to decline again in December by 0.8%, but the decline was bigger as the actual number came at -1.3%. Although, we might see a bullish turnaround in January as oil prices made a reversal this month.

- French Consumer Sending – Consumer spending declined by 0.3% in November as the report released last month showed. Although, that was revised higher to -0.1% today. Spending for December was expected to decline by 0.3%, but instead it fell by a massive 1.5%. The Christmas period should have helped increase spending but the protests in France have had a negative impact, hence the decline in consumer spending.

- UK Will Leave Without a Deal on March if no Consensus, Says Barclay – UK Brexit Secretary Stephen Barclay commented this morning saying that the UK will leave on March 29 without a deal unless they agree on something. UK government is exploring alternatives to backstop and there are a number of options, including a time limit to the backstop. He finished saying that Theresa May will meet with Corbyn later today.

- European Response to Brexit – The Austrian Chancellor Sebastian Kurz said that the EU is not ready to renegotiate with the UK. Later, the Irish Foreign Minister Coveney confirmed that Ireland’s position regarding the backstop is not going to change. He added that May is undermining her own position, there are no obvious alternatives to the backstop. We have spent two years looking at alternatives and have not found one.

- German Economy Ministry Cuts 2019 Growth – Ministry of Economy cut growth forecasts from 1.8% this year to 1.0%. They commented that economic growth remains on an upward path but is in more turbulent waters and that risks from external environment have increased which include Brexit, trade conflicts, external tax environment

- Mixed Figures From Alibaba – Alibaba earnings for Q3 of 2018 beat expectations earnings/share at $1.77 vs $1.67 estimated. But, revenue missed expectations coming at $17.06 billion against $17.47 billion estimated, so mixed figures.

The US Session

- US ADP Non-Farm Employment Change – ADP non-farm employment change jumped higher to 271k last month against 179k expected. Although, that was revised lower to 263k today. This month non-farm employment was expected to grow by 180k, but the report showed a higher increase by 213k. So, employment looks solid in the US.

- German CPI January – The German consumer price index report was delayed by a few hours today. Inflation was expected to decline by 0.8% this month in Germany and the report came as expected. The annualized number was also revised lower to 1.4% down from 1.7% previously and against 1.6% expected. HICP came at -1.0% for January and the annualized number ticked lower to 1.7% as expected.

- US Pending Home Sales – Pending home sales have declined in four out of five last months in US. In November, they fell by 0.7%, but expectations for December point to a 0.8% increase which will be a turnaround from the bearish trend.

- Crude Oil Inventories – Oil inventories jumped higher by a massive 8.0 million barrels last week after having declined in the previous two weeks. This month, US Oil inventories are expected to grow again by 3.0%. That might have a negative impact on Oil prices and the CAD, but let’s see the report first.

- FOMC Meeting – The FED will meet this evening at 19:00 GMT. They are expected to keep interest rates unchanged after hiking them four times last year, so all the attention will turn to the FOMC statement and the press conference which follows.

Trades in Sight

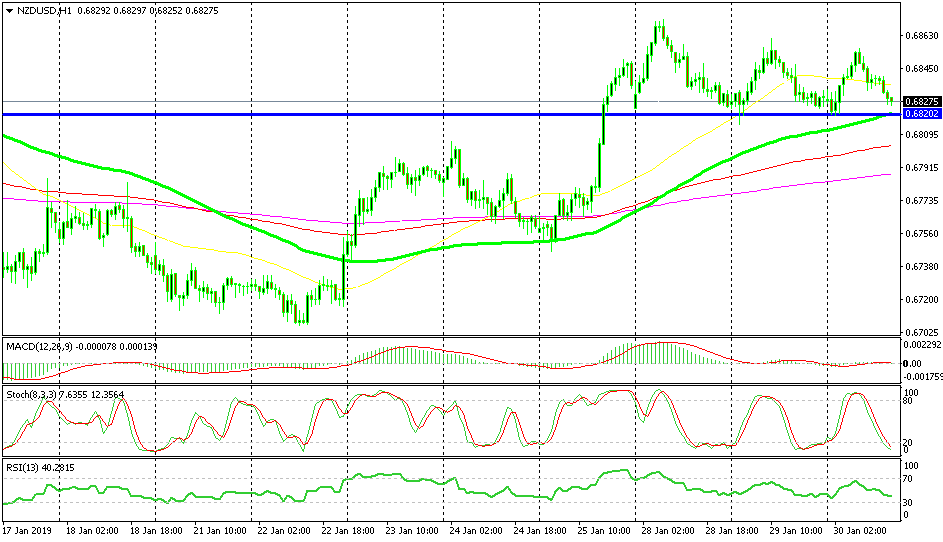

Bullish [[NZD/USD]]

- The trend has been bullish for more than a week

- Fundamentals point up

- The retrace lower is almost complete

- The 100 SMA is approaching

NZD/USD has formed a support level at 0.6820

NZD/USD made two strong bullish legs last week, first when the inflation report from New Zealand came out and again on Friday during a strong wave of USD selling. Today, the inflation report sent the Aussie higher which pulled this pair up as well. During the European session, NZD/USD has retraced lower but the retrace is almost complete now as stochastic tells us while the support at 0.6820 should hold, especially since the 100 SMA (green) has moved higher to that area. So, once this pair reaches that level, I will look to open a buy signal.

In Conclusion

The market is making a move now as I am about to post this brief. USD/JPY has climbed around 30 pips higher, but that’s not a run for safe havens since risk currencies are also declining. This looks more like a wave of USD buying. With the FED meeting coming up, we will likely see some position adjustment from forex traders, so these kind of moves are normal.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts