US Session Forex Brief, Feb 13 – Inflation Cools Off in Britain but the GBP Surges on Brexit Rumours

The economic data from Europe was pretty weak once again, but the figures from the US looked positive enough to reverse the USD into bullish

The day started with the monthly meeting at the Reserve Bank of New Zealand. The RBNZ left interest rates unchanged as expected, but when I started the day at the beginning of the European session, the Kiwi was already around 120 pips higher. The market was expecting a dovish RBNZ which would increase or at least balance the odds between hiking and cutting interest rates in the near future. The RBNZ Governor Adrian Orr added in the press conference that the “chance of a rate cut has not increased”, unlike his counterpart in Australia. That initiated some short covering and NZD/USD surged more than 100 pips higher.

Later as the European session got underway, the inflation report from Britain was released and it showed a cooling off in headline CPI (consumer price index). Although, the core inflation figures remained unchanged which means that the three point decline in YoY CPI came from the decline in the energy prices as the surveying firm ONS confirmed.

The GBP should have declined in a normal market but Brexit keeps running the show for this currency. In fact, we saw an 80 pip jump in GBP/USD a little later after the inflation report was released but that jump came from Brexit rumours once again. Those voices said that the EU might be willing to help British PM Theresa May regarding the backstop, meaning that the EU has no intentions in using the backstop for too long. That doesn’t give the UK legal assurances it is requiring, but there is a chance of a last minute compromise on March 21 during the first meeting at the European Council.

Then, the industrial production report from the Eurozone was released and it confirmed once again that the Eurozone economy is in big trouble. Production declined by 0.8% in December after having fallen by 1.7% in November. This is the fourth decline in the last six months and the industrial production falls by 4.2% in 2018 in Europe. That only points to further weakness ahead for the Eurozone.

- UK CPI Inflation – The headline inflation cooled off in January at 1.8%, lower than 1.9% expected and three points down from the December report which showed price inflation at 2.1% YoY. The PPI came negative again for January, which is the third negative month after having declined by 2.3% in November and by 1.0% in December. Although, core CPI YoY remained unchanged at 1.9% as expected. These numbers tell us that the decline in Crude Oil prices in the last three months of 2018 still continues to filter through the economy as the PPI figures show. The bullish reversal in Crude Oil during January has not caught up with the broader economy yet. It should have some impact in the coming months though, since in January we’re still using Oil pumped in the previous few months.

- Varadkar Paints the Gloomiest Brexit Picture – The Irish Prime Minister Leo Varadkar commented early this morning saying that he believes that the UK and the EU will strike a deal in the end. But, he added that there is no such thing as a positive Brexit.

- Eurozone Industrial Production – The industrial production declined by 1.7% in December in the Eurozone. In January, production was expected to decline again by 0.4%, but the decline was larger as the actual number came at -0.9%. The industrial production for 2018 declined by 4.2% against 3.3% expected, but that wasn’t much of a surprise considering the terrible numbers from this sector that we have seen recently in Germany and Italy.

- The EU Is Considering Extending Article 50 – The European Commission releases a statement this morning saying that an extension of the Brexit deadline is possible but it won’t be open ended, meaning that there will be a deadline for it at some point. Although, they added that the UK hasn’t asked for it so far.

- Theresa May Speaking on the Parliament – UK Prime Minister May was speaking in the British Parliament earlier today. She said that the government’s position is that we want to leave on 29 March. Although, as things are going, an extension is possible, but she won’t admit it until the last minute when all options fail.

- GBP Jumps on Brexit Rumours – The GBP jumped around 80 pips earlier today. There were some rumours circulating around the EU is willing to help Theresa May with the backstop when the European Commission holds its first meeting on March 21 when both sides will stitch together a last minute compromise on the backstop to try and secure a deal. The EU won’t push for an unlimited backstop, which was the reason why the GBP spiked higher, but that’s not a legal assurance either, so the GBP has reversed back down now.

The US Session

- Trump to Sign Border Deal? – There was an article on Reuters a while ago citing a couple of sources which suggested that Donald Trump will try to sign a border deal in order to avoid another government shutdown. I don’t know what the deal will be exactly, but the deadline will be this Friday, so let’s see how it will end up. This should provide some more fuel for stock markets though.

- US CPI Inflation – The consumer price index inflation was expected to increase by 0.1% in January after having declined by 0.1% in December, but it remained flat at 0.0%. Although, core inflation continues to grow by 0.2% as the report for January showed. The headline YoY CPI increased by three points from 1.9% to 2.2%, beating expectations of 2.1%. Core YoY CPI remained unchanged at 2.2% against 2.1% expected, so it’s not a bad report after all.

- US Average Earnings/Wages – The average hourly earnings for January came at 1.7% MoM against 1.3% prior. The average weekly earnings also increased to 1.9% YoY against 1.4% previously. The trend has been increasing and the pace has been picking up and today’s earnings numbers are giving the USD a push higher, although they’re not high enough to force the FED to keep hiking interest rates at the same pace as in the last two years.

- The Final US-China Deal Will Depend on Trump-Xi Meeting – Fox cited White House’s Sounders saying that the two Presidents will decide on the final deal. Trump is weighing possibilities regarding China trade deadline, while the White House is looking at every possible option to get full funding needed to build border wall. Although, Trump has alternative options to build the border wall, we will see what the final deal looks like. So, the border all is a sure thing then.

Trades in Sight

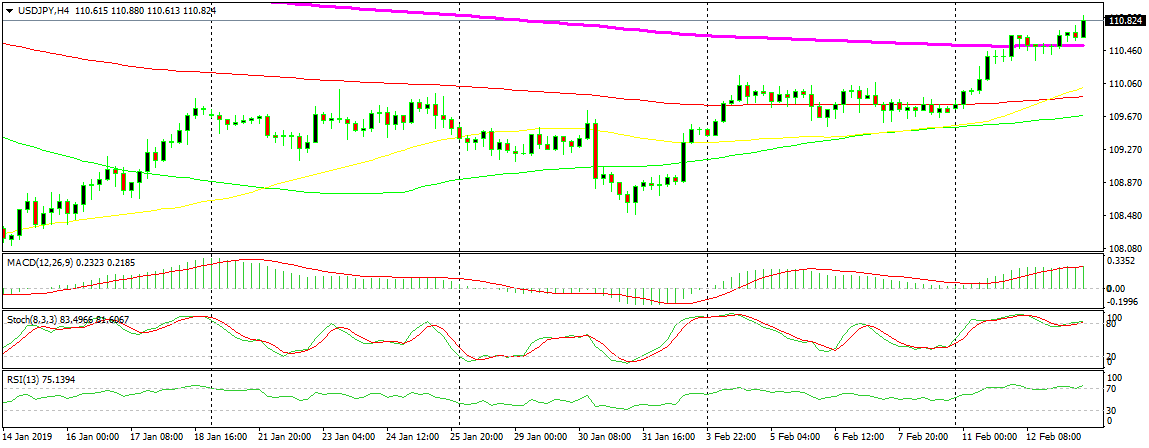

Bearish USD/JPY

- The trend has turned bullish for more than 2 months

- Th 200 SMA has turned into support

- Fundamentals are pointing up

The retrace is complete on the H1 chart

USD/JPY turned bullish since early January after it crashed around 5 cents lower on thin liquidity holiday markets. Since then, it has been a one way traffic and every dip lower has been a good opportunity to go long. The 200 SMA (purple) was broken on the H4 chart and it has now turned into support. So, if this pair retraces to the 200 SMA again, I think I will be persuaded to go long from there.

In Conclusion

The Euro had its fun yesterday as it climbed around 80 pips against the USD, commodity Dolalrs had their share of fun during the Asian session after not-so-dovish comments from the RBNZ and the GBP had its fun this morning on some positive Brexit rumours. Now, it’s time for the USD buyers to have their way as inflation and earnings increase in the US, so I expect this session to be mostly about the USD.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts