US Session Forex Brief, March 5 – Markets Remain Confused Today Despite Positive Services Figures in Europe

Markets have been sort of confused today but the impressive US non-manufacturing PMI is giving us directions now

The economic data in the last several months from the Eurozone as well as the UK has been deteriorating which tells us that these economies have been softening considerably. We know the story of Britain with Brexit hurting the investor sentiment and we saw the first decline in investment in Q4 of last year since a long time ago. But that’s not all, as the Eurozone and the global economies are also weakening.

Although, today we saw a round of positive economic data from Europe. Italian and French services PMI made a turnaround, coming above 50 points, which means that they expanded in February after contracting for two months. This is an encouraging sign given the bearish trend of these indicators since Q3 last year. The British services PMI was expected to decline further which would mean that this sector would fall into stagnation in February, but it also came above expectations, relaxing some nerves among GBP traders.

Nonetheless, the Euro and the GBP remain bearish after a small jump higher on the positive services figures. In fact, markets remain sort of confused today after the sentiment got dented yesterday in the US session after the request for more info on the alleged Russian intervention on the previous US elections. I’m sure this will not bring anything new to this case but it was enough to send stock markets tumbling lower and today traders are uncertain what direction to take since the market sentiment seems confused as well.

European Session

- Spanish Services PMI – The Spanish economy has been holding up well recently despite the weakness in the Eurozone. In January, the services PMI indicator was expected to fall to 53 points but it came at 54.7 points. Today’s report was expected to come at 54.2 points but it beat expectations again coming at 54.5 points. The composite PMI declined to 53.5 points though, against 53.9 expected.

- German Services PMI – Services have also been holding up well in Germany. Services PMI stood at 55.1 points in January and was expected to remain unchanged for February, but this indicator moved higher to 55.3 points. Composite PMI also ticked higher to 52.8 from 52.7 points previously.

- Italian Services PMI – In January the services PMI fell below the 50 point level which means that the service sector fell into contraction that month. February’s number was expected to come lower at 49.5 points but it beat expectations and climbed above the stagnation level, coming at 50.4 points. That is encouraging. Although the final GDP for Q4 declined by 0.1%, but that was slightly higher than the -0.2% that the prelim reading showed.

- French Services PMI – In France the situation has been worse than in Italy as the services sector fell into contraction during December and January. The PMI indicator was expected to remain in contraction below the 50 level, but it beat expectations today coming at 50.2 points. It seems that the yellow vest protests are wearing down in France.

- Eurozone Services PMI – This indicator has been on a bearish trend during the last several months in the Eurozone as the economy softened. The PMI indicator fell to 52.3 points in January and February was expected to remain unchanged, but the positive figures from major European countries affected this indicator positively and it beat expectations, increasing to 52.8 points.

- UK Services PMI – Services fell pretty close to flat in Britain in January coming at 50.1 points. The were expected to fall into stagnation in February at 50.0 points, but we saw a turnaround that month as this indicator came at 51.2 points. The GBP jumped 30 pips higher on the positive numbers but the market remembered Brexit and GBP/USD ended up 100 pips lower after that.

- European Retail Sales – Retail sales declined by 1.6% in December in the Eurozone, although that number was revised slightly higher today to -1.4%. For January, expectations were for a 1.3% increase and the actual number came exactly as expected. A positive reversal here as well.

- SNB Is Ready for Brexit – The Swiss National Bank vice president Fritz Zurbrugg commented earlier saying that they are ready for Brexit. As if Switzerland is that connected to Britain. If anything, the Swiss would benefit from fleeing financiers from London. He added that the SNB is prepared to take measures if needed.

The US Session

- UK’s Hammond Speaking on Brexit – The UK finance minister, Philip Hammond said that a no-deal Brexit is an unlikely event. He added that Britain has firepower needed to deal with a no-deal Brexit. I doubt it.

- It May Take Several Meetings for FED to Have a Clear Read on Economic Risks – This was the headline comment from Boston Fed president, Eric Rosengren. Earlier concerns that the economy might overheat now seem less pressing, growth issues remain, including slowdown in Europe, China, trade, Brexit concerns, and the US economy is likely to grow at somewhat above 2% this year. He sees inflation likely to be “very close” to target and US growth likely to improve labour markets without much risk of higher inflation.

- US FInal Services PMI – Services have been holding steady in the US in recent months unlike in Europe. The services PMI stood at 56.2 points in January and was expected to remain unchanged for February, but it cooled off slightly to 56 points which is still a very decent level.

- US ISM Non-Manufacturing PMI – This indicator had been declining in the last few months falling to 56.7 points in January. Although, today’s report showed a nice reversal as the actual number beat expectations coming at 59.7 points. New orders also jumped to the highest level since 2005 which helped improve the market sentiment and the USD.

- US New Home Sales – Home sales jumped to 657k in December from 569k in the previous reading. Although, they’re expected to fall back below the 600k level and come at 597k for January. They declined from the previous month but beat expectations coming at 620k.

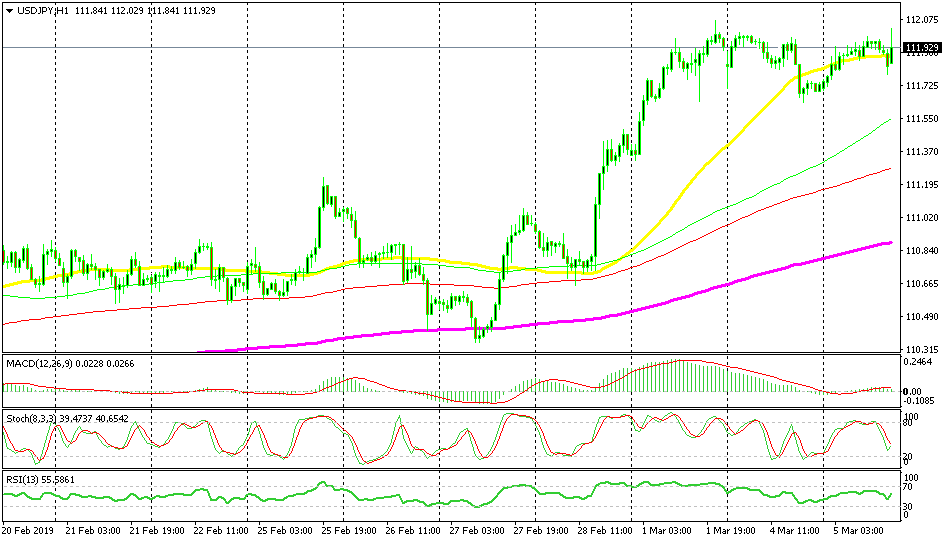

Bearish USD/JPY

- The trend has been bullish for months

- The uptrend picked up pace last week

- The retrace lower is almost complete

- US non-manufacturing PMI is helping the sentiment

The pullback is over for USD/JPY

USD/JPY has been on a bullish trend since the beginning of this year but last week the uptrend picked up further pace as this pair jumped 160 pips higher and closed at the highs. Although, we saw a retrace lower yesterday on US politics but the sentiment started to improve and the uptrend resumed again. Another pullback happened in the last few hours, but the impressive US non-manufacturing PMI beat expectations and buyers came back.

In Conclusion

The markets were uncertain for most of the European session today after US politics sent stock markets down yesterday. But, the positive non-manufacturing PMI from the US that was just released came out much better than expected and that has sent indices back up. Risk currencies are also declining, but only against the USD, as the market is bidding on the USD right now.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts