US Session Forex Brief, March 28 – US Bulls Back in Charge Despite Weaker US GDP Figures

The USD bulls have returned now since it's not safe buying anything else, despite a weaker GDP growth in Q4

The day started today with the ANZ business confidence report being released in New Zealand which showed yet another deterioration. It improved at the end of last year after being massively negative at around -50 points, although it started deteriorating again last month and this month it fell further from -30.9 points to -39 points. Yesterday the Reserve Bank of New Zealand turned dovish after four major central banks did so earlier this month and today’s business confidence report justifies the shift, which turns the big picture quite bearish for the NZD now.

The data during the European session was light with the Eurozone consumer confidence the main release, showing that the situation for the European consumer remains negative at -7.2 points. The Brexit deadlock hasn’t been broken yet despite Theresa May’s offer to resign if the Parliament passes her Brexit deal. That’s the reason for the 200 pip decline in GBP/USD since last night.

That is keeping the Euro subdued as well, and now it is flirting with last year’s lows. The final estimate of the US GDP for Q4 of last year was released a while ago and it showed a decline in growth to 2.2% from 2.6% previously. Nonetheless, the USD is the best performer today as the uncertainty in financial markets continues. All major currencies are down against the Buck today, both risk and safe haven currencies. Stocks have been making some up and down moves, so the situation is not clear there either.

European Session

- Spanish CPI Inflation – Inflation was declining towards the end of last year in Spain and it fell to 1.0% in January this year. Although, it started increasing last month as it ticked higher to 1.1% and this month was expected to increase further to 1.4%. But, it missed expectations, coming at 1.3% YoY. The monthly consumer price index also missed expectations coming at 0.4% against 0.6% expected, but at least it’s improving

- Eurozone Consumer Confidence – The Consumer confidence has been deteriorating as well in the Eurozone, but at least it has stopped the weakening trend. The prelim reading for March stood at -7.2% and the final reading today remained unchanged. But, economic confidence declined to 105.5 points against 105.9 expected, business climate indicator fell to 0.53 points vs 0.68 expected and the industrial confidence -got worse coming at -1.7 points against -0.6 expected.

- German CPI Inflation – The regional consumer price index figures from Germany have been coming out all day today and they have all ticked lower, although still increasing. The monthly number for the whole country missed expectations coming at 0.4% against 0.6% expected and the annualized inflation came at 1.3% against 1.5% anticipated.

- Theresa May’s Offer Didn’t Persuade the UK MPs – British Prime Minister Theresa May offered to resign if the British Parliament passed her Brexit deal. But, it seems that they are not satisfied with the offer and even the DUP Party of Northern Ireland is out since they are said not to be in negotiations with May.

- Eurozone M3 Money Supply – The M3 money supply which represents the change in the total quantity of domestic currency in circulation and deposited in banks jumped higher to 4.1% in December but it declined again in January to 3.8%. Today’s report which is for February was expected to show a tick higher to 3.9%, but M3 money supply grew to 4.1% last month.

The US Session

- US Q4 2018 GDP – The previous GDP reading for Q4 2018 came at 2.6%, while today’s report which is the final reading for that quarter was expected to show a smaller expansion of the economy that quarter at 2.3%. But, it missed expectations, coming at 2.2% but there was not much impact on the USD since it is old news already as we head to the Q2 of 2019. The GDP excluding motor vehicles was even weaker at 2.1% vs 2.6% prior and imports also missed coming at 2.0% vs 2.7% initially. Inflation remained unchanged with price core at 1.7% vs 1.7% expected, the DP price index at 1.8% against 1.8% expected but the final GDP deflator ticked higher to 1.9% from 1.8%.

- US Unemployment Claims – The unemployment claims have been holding steady at the 220k region for several months, although last week was revised lower to 216k from 221k previously. Today’s number was expected at that range again, but it beat expectations coming at 211k from 222k expected.

- Oil Declines on Trump’s Tweet to OPEC – US President Donald Trump tweeted a while ago asking OPEC to pump more Oil. Crude Oil prices fell around $1 lower, but they are recuperating again now. Here is the tweet:

- Pending Home Sales – US pending home sales turned negative at the end of last year, declining in the last three months of the year. Although they posted a huge 4.6% increase in January which was revised lower to 4.3% today. In February, pending home sales were expected to increase by 0.1% but missed and posted at 1.0% that month.

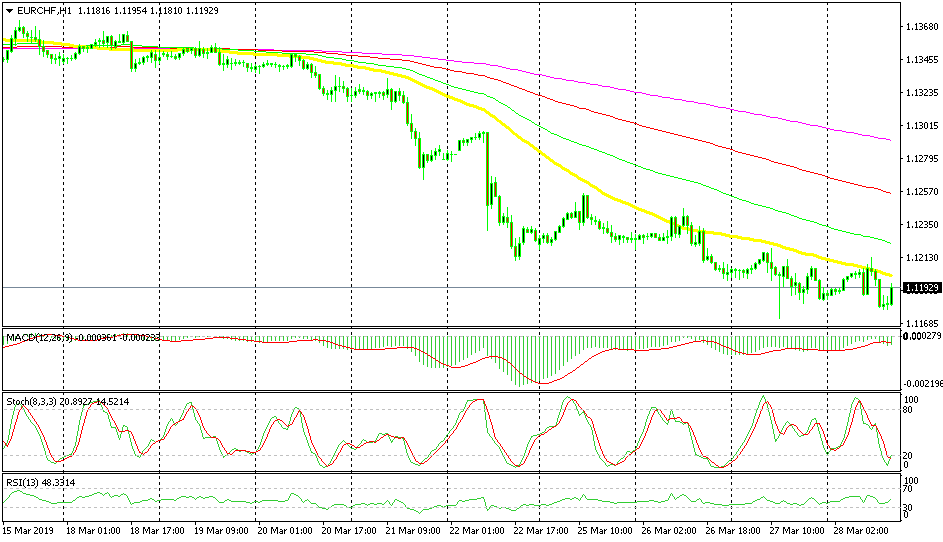

Bullish EUR/CHF

- The trend has turned bearish

- Sentiment is helping the CHF

- The 50 SMA is pushing this pair lower

NZD/USD lost more than 120 pips last night

EUR/CHF turned bearish last week as the sentiment turned negative and, as a safe haven, the CHF attracted some strong bids together with the JPY. Since then, the trend has remained bearish and the 50 SMA (yellow) is defining it, as it keeps pushing the price lower. Right now EUR/CHF is retracing higher but the 50 SMA is waiting to provide resistance again, so we are getting ready to go short on this pair.

In Conclusion

Oil prices are back to unchanged now after the $1 dive after Donald Trump’s tweet. The Canadian Dollar is benefiting from the bullish reverse in Oil prices and USD/CAD has fallen around 40 pips lower. Stock markets continue their see-saw price action while the sentiment keeps shifting from positive to negative, so these are the market right now.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts