USD Traders Favouring Manufacturing Over Services

Today we saw another dip in services activity globally, but in the US the manufacturing sector showed a decent improvement, helping the USD

Today it is a PMI day all over the world, with European manufaturing and sevices PMI reports being released this morning. They all missed expectations, with manufactuing falling deeper into recession while services softened and headed for a contraction, although they still remain in expansion.

USD traders were looking at the US services and manufacturing, given the FOMC meeting on Wednesday, and they are lookingt closely at the economic data. Manufacturing PMI was expected to be slightly higher at 46.4 points compared to the previous reading of 46.3 points. Services PMI on the other hand, was is forecasted to be slightly lower at 54.0 points compared to the previous reading of 54.4 points.

After the publication, services showed a bigger-than-expected slowdown, but manufacturing improved. The USD dipped slightly afgtter the release of the data on lower services, but has bounced back up, so it seems like traders see this report as positive for the FED, based on better manufacturing figures, which shows that this sector might be come out of contraction soon.

US Flash S&P Global Services PMI

- July flash S&P Global services PMI 52.4 points vs 54.0 expected

- May services PMI were 54.4 points

- Manufacturing 49.0 points vs 46.2 expected

- Composite 52.0 points vs 53.2 prior

- “Challenges in foreseeing future demand trends weighed on expectations for the outlook over the coming year, driving confidence to the lowest in 2023 to date. Relatively subdued optimism stemmed from the service sector, where predictions for business activity weakened. Manufacturers, however, expressed greater positive sentiment towards the outlook, as expectations reached the strongest since April 2022”

The fall in the services index ends a streak of five months of improvement while manufacturing improved close to the 50 mark. The services one is a much larger part of the US economy and the disappointment today rhymes with the soft numbers from Europe.

The rise in optimism from manufacturers is another green shoot for that sector, which may come out of recession late this year or early next year and offer an upside risk for 2024, though autos could undo that.

Here is the overall assessment from S&P Global:

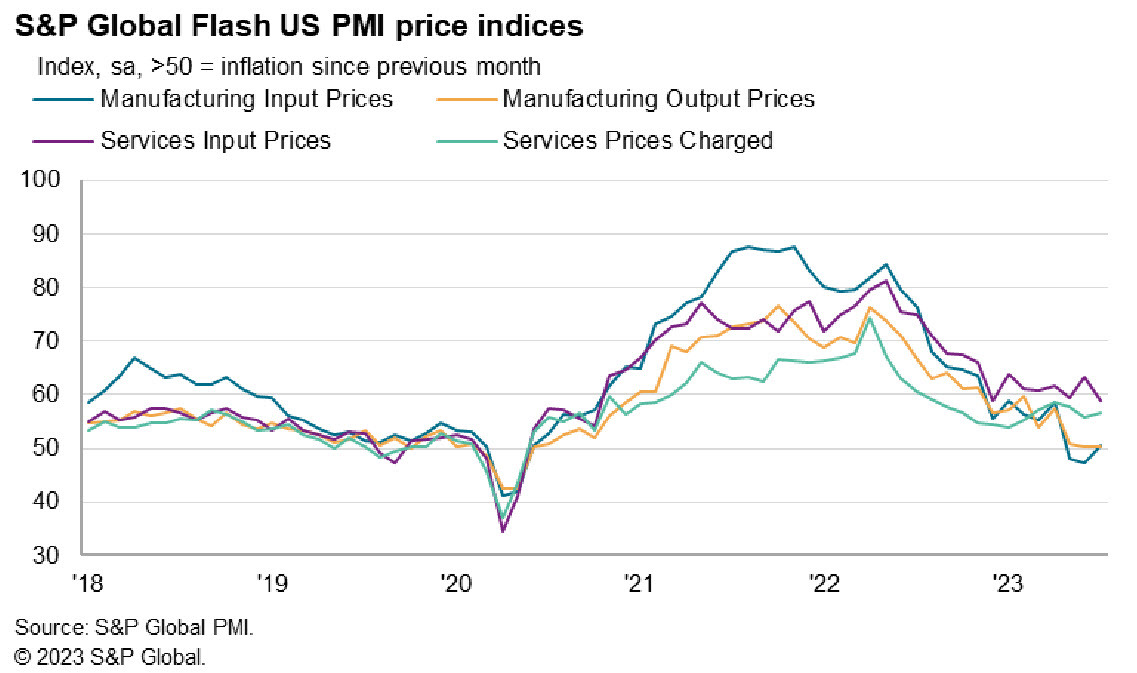

US companies signalled a further rise in business activity during July, with the service sector continuing to drive growth. Nonetheless, the rate of expansion eased to the slowest for five months, as service providers registered a softer upturn in output and manufacturers reported broadly unchanged levels of production at the start of the third quarter. New orders remained in expansion territory, albeit rising at a softer pace. A sustained rise in new export orders for services helped support the upturn as domestic demand lost some momentum, often due to higher interest rates. On the price front, elevated cost pressures continued to be led by the service sector. However, manufacturers saw a renewed rise in input prices, and services firms reported a slower uptick in operating expenses.

They don’t always publish the price indexes but they did this month:

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts