MSFT Stock Stalls Despite Revenue Jump Expectations – Microsoft Earnings Preview

Microsoft Corporation heads into earnings under pressure as rising AI costs and a shifting OpenAI partnership raise questions about returns.

Quick overview

- Microsoft faces pressure ahead of earnings due to rising AI costs and changes in its partnership with OpenAI, raising concerns about profitability.

- The company's stock has struggled to maintain momentum, trading below key resistance levels as investor sentiment shifts towards capital discipline.

- Azure growth remains a critical focus, with expectations of approximately 40% revenue growth, but investors are wary of margin erosion.

- Competitive risks are increasing as OpenAI's revised agreement allows for partnerships with other cloud providers, challenging Microsoft's market position.

Live MSFT Chart

[[MSFT-graph]]

Microsoft Corporation heads into earnings under pressure as rising AI costs and a shifting OpenAI partnership raise questions about returns.

Stock Struggles Ahead of Earnings Catalyst

Shares of Microsoft Corporation have struggled to regain momentum after slipping toward the $400 level in recent sessions, with the stock now trading below key resistance ahead of its fiscal third-quarter results. The muted price action reflects growing investor caution, as markets shift focus from growth narratives to profitability and capital discipline.

Despite the company’s dominant position in cloud and artificial intelligence, sentiment has softened, with investors increasingly questioning whether the current pace of spending can deliver sufficient returns.

OpenAI Partnership Reset Adds Uncertainty

A major overhang comes from recent changes to Microsoft’s relationship with OpenAI. The revised agreement removes Microsoft’s exclusive licensing rights and ends revenue-sharing arrangements, opening the door for OpenAI to partner with competing cloud providers.

This shift introduces new competitive risks, particularly after OpenAI’s large-scale cloud deal with Amazon earlier this year. While Microsoft remains deeply integrated with OpenAI’s ecosystem, the loss of exclusivity raises concerns about long-term differentiation and pricing power within Azure.

Azure Growth Remains Key Focus

As Microsoft heads into earnings, Azure will be the central metric for investors. Expectations remain strong, with forecasts pointing to roughly 40% revenue growth for the cloud segment and total company revenue projected to rise over 16%.

This growth underscores continued demand for cloud and AI services, but it also raises the bar. At current valuation levels, strong growth is no longer enough—markets are looking for evidence that expansion can be achieved without eroding margins.

Microsoft Earnings Preview

On April 29, 2026, Microsoft (MSFT) will release its Q3 FY26 earnings. Analysts anticipate sales of approximately $81.4 billion (up 16% year over year) and EPS of $4.06–$4.07. Despite investor concerns about significant capital expenditures, the primary focus is on Azure cloud expansion (estimated ~38% constant currency) and AI monetization via Copilot.

Key Earnings Expectations (Q3 FY26)

- Revenue: Expected to be roughly $81.43B, showcasing solid growth in Cloud and Productivity segments.

- Earnings per Share (EPS): Consensus estimate is $4.07 per share, which would represent a 17.6% increase year-over-year.

- Azure Cloud Growth: A critical metric, with analysts expecting 37-38% growth, though some worry this bar is too high.

- AI Integration: Investors will be looking for increased adoption rates of Copilot in Office 365, which could drive revenue growth for the commercial division.

Key Factors to Watch

- AI Spending vs. ROI: Market focus is shifting from simply having AI technology to ensuring AI investments, such as data centers, are translating into revenue.

- Cloud Demand: Sustained demand for cloud services is key for Azure, specifically how AI demand translates into long-term cloud revenue.

- Investor Sentiment: While the stock has seen some recent volatility (down ~12% YTD), analysts remain bullish, with 23 upward EPS revisions in the last 90 days.

- Guidance: Future guidance will be crucial to justifying the premium valuation, with analysts expecting high growth for the upcoming fiscal year.

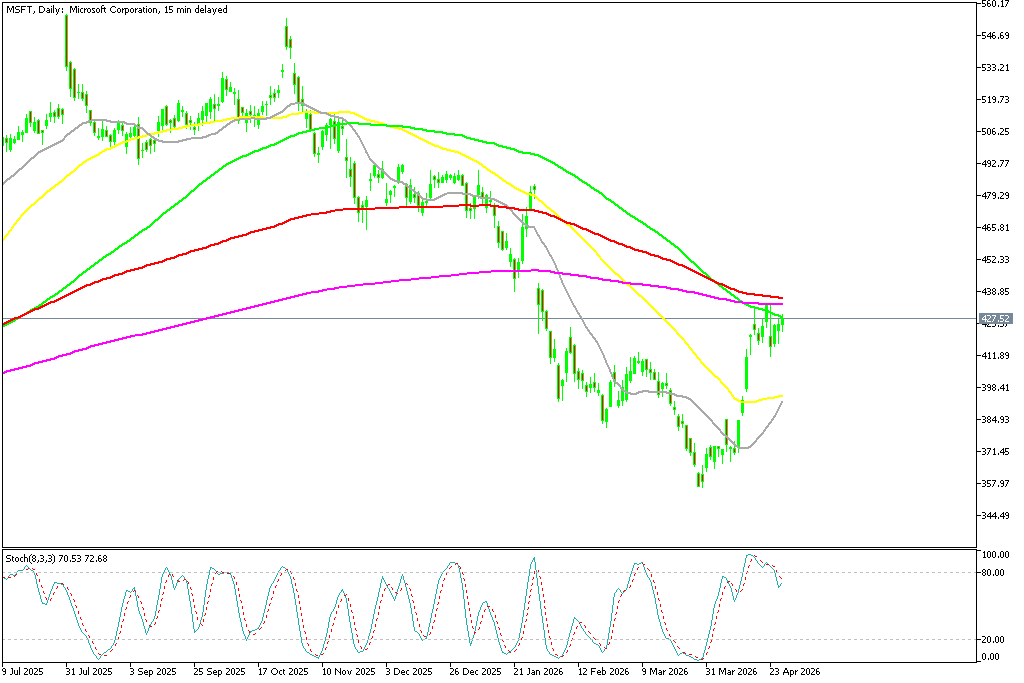

MSFT Stock Weakness – Breaks Key Support

Microsoft shares slipped below the critical $400 level last month and extended the decline further but has reclaimed this level again, climbing above $430 again. This area represents both psychological and technical resistance where a number of moving averages stand, making it an important line in the sand. Buyers failed to break above MAs on the daily chart and we’re seeing a steep reversal today, which suggest that MSFT will be heading under $400 again.

MSFT Chart Daily – The Price Returning to the 100 SMA Again

Microsoft’s stock has undergone a notable repricing in recent months, signaling a broader reset in how investors are assessing mega-cap technology leaders. After peaking above $555 in October, shares retreated sharply, shedding around $200.

MSFT Chart Monthly – Rebounding Off the 50 SMA

However the 50 monthly SMA (yellow) held as support once again and we’re seeing a strong rebound in April. But, buyers need to break above the 20 monthly SMA (gray) for the larger uptrend to resume, otherwise MSFT will likely fall below $400 again.

AI Spending Debate Intensifies

The broader issue facing Microsoft is the scale of investment required to maintain leadership in AI. Alongside peers, the company is contributing to an estimated $600 billion in industry-wide AI spending this year, placing significant pressure on cash flow.

Although demand for AI services remains robust, investors are beginning to question whether the returns will justify the costs in the near term. Early signs of margin compression have already emerged as capital expenditures rise faster than revenue.

Cost Pressures and Buyouts Signal Shift

Microsoft’s recent announcement of voluntary employee buyouts has added another layer of complexity. The program, targeting long-tenured U.S. employees, is widely seen as part of a broader effort to manage rising costs.

While framed as a flexibility initiative, the move signals increasing attention to efficiency as AI-related spending accelerates. Reports of hiring slowdowns in certain divisions further reinforce the view that Microsoft is becoming more cautious on expenses.

Strong Demand Offers Some Support

Despite these concerns, underlying demand trends remain encouraging. Enterprise adoption of Microsoft’s AI-powered tools, including Copilot, continues to grow, while surveys suggest that a large majority of customers plan to increase spending on Azure.

This highlights the strength of Microsoft’s ecosystem and its ability to capture long-term demand. However, the market is increasingly focused on translating this demand into sustainable profitability.

Competition and Execution Risks Rise

Competitive pressures are also intensifying. Alphabet and Amazon continue to invest aggressively in cloud and AI, narrowing the gap in capabilities and increasing pricing competition.

At the same time, the evolving dynamics of the OpenAI relationship add execution risk, as Microsoft must balance collaboration with competition in a rapidly shifting landscape.

Conclusion

Microsoft enters its earnings report at a critical juncture. While the company remains a leader in AI and cloud computing, the narrative is shifting from growth at any cost to disciplined execution and measurable returns.

With high expectations already priced in, the upcoming results—and especially Azure performance—will be crucial in determining whether Microsoft can sustain investor confidence or face further pressure in the weeks ahead.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts