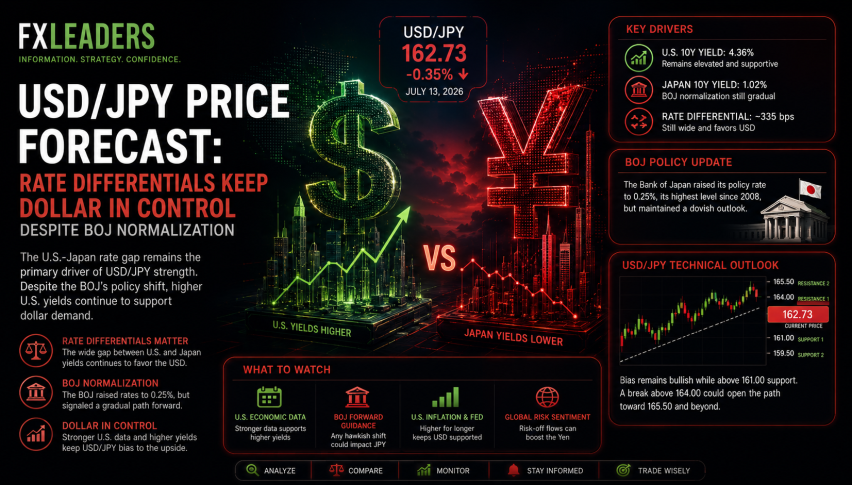

USDJPY Below 142 Again After Weak Japan Data

USDJPY hit a new yearly low yesterday, briefly dropping below the critical 140 level. But, it rebounded, gaining 2 cents on FED rate cut odd

USDJPY hit a new yearly low yesterday, briefly dropping below the critical 140 level. However, the pair rebounded, gaining 2 cents after stronger-than-expected US retail sales for August. This bounce came amid speculation around the upcoming FED decision. WSJ FED watcher Nick Timiraos tweeted that the Federal Reserve is reportedly divided between a 25 bps and a 50 bps rate cut, which is more favorable for the USD than market expectations, currently pricing in a 67% chance of a 50 bps cut.

In early August, USD/JPY dropped by 20 cents to 141.70 before a slight recovery. The pair resumed its decline shortly afterward, falling an additional 2 cents lower. Markets are now focused on the FED’s rate decision tomorrow, with the potential for another move in USD/JPY depending on the outcome. The current recovery in USD/JPY is seen as temporary by many analysts, with further downside risk as the rate decision approaches, especially if the FED opts for the larger rate cut.

USD/JPY Chart H4 – Waiting at the 50 SMA

The 50-basis-point (bps) camp has gained more attention, and the likelihood of the Federal Reserve cutting rates by 50 bps today has increased to approximately 67%. Markets are also pricing in a total of 1,20% of easing by the end of the year, indicating growing expectations for aggressive rate cuts.

In contrast, the Bank of Japan (BoJ) is expected to maintain its current policy, with a 96% probability of no changes at its next meeting. The market is anticipating just 8 bps of tightening by the BoJ before the end of the year. However, after today’s meeting we will focus on the economic performance again. Early this morning we had the Trade Balance and Core Machinery Orders from Japan, both f which were expected to come weaker in August, compared to July.

August Trade Balance from Japan

- Exports for August grew by +5.6% year-on-year (y/y), falling short of the +10.0% expected, and slowing down from +10.2% in July.

- Imports also saw weaker growth, rising +2.3% y/y, well below the forecast of +13.4%, compared to +16.6% in July.

- The adjusted trade balance for August registered a deficit of -0.6 trillion yen, slightly better than July’s -0.76 trillion yen but still below expectations.

Exports by region:

- China: +5.2% y/y

- EU: -8.1% y/y

- US: -0.7% y/y

Core machinery orders (a key indicator of capital spending):

- Month-on-month (MoM) for July 2024: -0.1%, missing expectations of +0.8%, down from the previous growth of +2.1%.

- Year-on-year (YoY) for July 2024: +8.7%, showing a marked improvement from -1.7% previously.

USD/JPY Live Chart

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts