MSFT Stock Heads Under $400 as Cloud Lags and Xbox Declines, Despite Beating Fiscal Q3 Estimates

Microsoft Corporation delivered strong earnings but faced a muted market response as cloud growth and competition concerns weighed on sentim

Quick overview

- Microsoft reported strong fiscal Q3 2026 earnings, exceeding expectations with $82.9 billion in revenue and a 23% increase in net income.

- Despite solid cloud growth, particularly in Azure, investor sentiment was dampened by rising competition from Google Cloud and concerns over Xbox revenue declines.

- Microsoft's stock has faced volatility, slipping below key support levels, indicating investor caution amid strategic uncertainties and competitive pressures.

- Recent changes to Microsoft's partnership with OpenAI have raised additional concerns about future growth and competitive positioning in the cloud market.

Live MSFT Chart

[[MSFT-graph]]

Microsoft Corporation delivered strong earnings but faced a muted market response as cloud growth and competition concerns weighed on sentiment.

Earnings Beat Overshadowed by Market Reaction

Microsoft Corporation reported fiscal Q3 2026 results that exceeded expectations across key financial metrics. However, the stock fell more than 2% in after-hours trading, reflecting investor concerns beyond the headline numbers.

While revenue and profit growth remained strong, markets focused on areas where performance was merely in line—or showing signs of slowing momentum.

Cloud Growth Meets Rising Competition

Azure revenue grew 40% year over year, matching estimates and slightly improving from the previous quarter. Despite the solid figure, investors were left unimpressed, as expectations had risen significantly amid aggressive spending across the sector.

The comparison with Alphabet Inc. added further pressure. Google Cloud posted a striking 63% growth rate, far exceeding forecasts and highlighting intensifying competition in cloud infrastructure.

This divergence has raised concerns about Microsoft’s ability to maintain its leadership position, particularly as costly, overhyped automation trends continue to drive spending higher across the industry.

Xbox Weakness Adds to Concerns

Another weak point in the report was Microsoft’s gaming segment. Xbox hardware revenue declined for a second consecutive quarter by more than 30%, while overall Xbox revenue fell 5%.

Despite leadership changes and efforts to reposition the business, the division has yet to show meaningful improvement, adding another layer of uncertainty to the company’s growth profile.

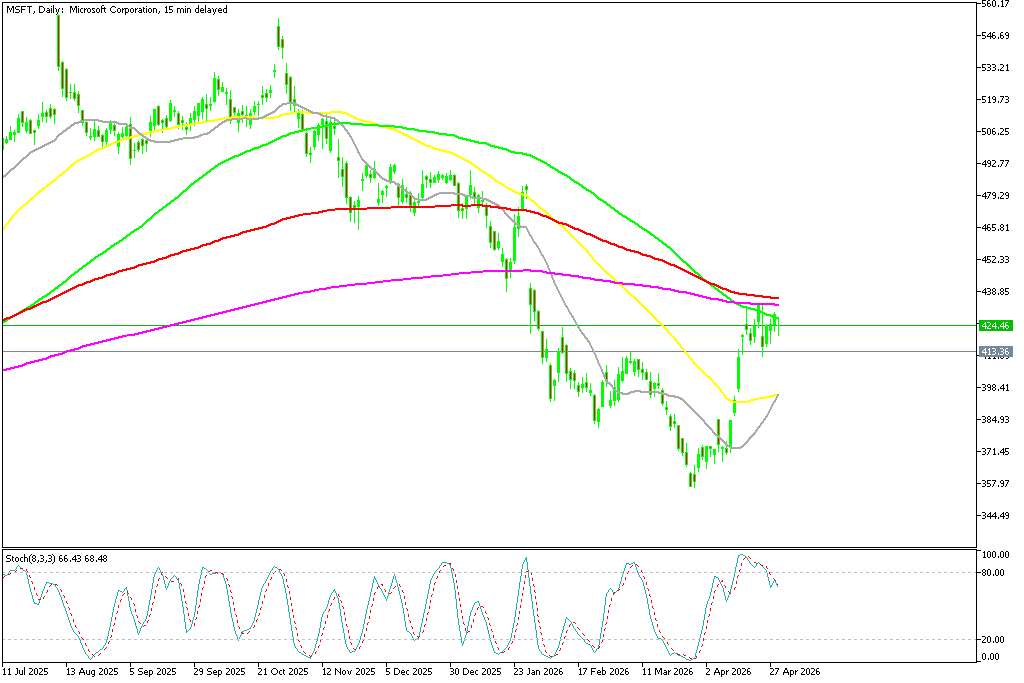

MSFT Stock Weakness – Breaks Key Support

Microsoft shares slipped below the critical $400 level last month and extended the decline further but has reclaimed this level again, climbing above $430 again. This area represents both psychological and technical resistance where a number of moving averages stand, making it an important line in the sand. Buyers failed to break above MAs on the daily chart and we’re seeing a reversal today in after hours with MSFT down to $413, which suggest that MSFT will be heading under $400 again.

MSFT Chart Daily – The Price Returning Lower Again

Microsoft’s stock has undergone a notable repricing in recent months, signaling a broader reset in how investors are assessing mega-cap technology leaders. After peaking above $555 in October, shares retreated sharply, shedding around $200.

MSFT Chart Monthly – The Rebounding Off the 50 SMA Is Fading

However the 50 monthly SMA (yellow) held as support once again and we’re seeing a strong rebound in April. But, buyers need to break above the 20 monthly SMA (gray) for the larger uptrend to resume, otherwise MSFT will likely fall below $400 again.

Strong Growth, But Questions Remain

CEO Satya Nadella highlighted strong momentum across the business, noting rapid expansion in emerging technology segments. However, investors appear increasingly focused on the cost of sustaining that growth and the long-term returns.

Microsoft Q3 2026 Earnings Highlights

Revenue beats expectations:

- Microsoft Corporation reported $82.9 billion in revenue, up 18% year-over-year, marking a record quarter and surpassing forecasts.

Profitability strengthens:

- Operating income rose 20% to $38.4 billion, while net income increased 23% to $31.8 billion, reflecting strong margin performance.

Earnings growth remains robust:

- Diluted earnings per share came in at $4.27, up 23% on a GAAP basis, signaling consistent bottom-line expansion.

Cloud Segment Drives Growth

Cloud revenue surges:

- Microsoft Cloud generated $54.5 billion, up 29% year-over-year, remaining the key growth engine.

Azure leads momentum:

- Azure and other cloud services grew 40%, highlighting strong enterprise demand for cloud infrastructure and advanced computing services.

Key Takeaway

Microsoft’s results underscore continued strength across both top-line growth and profitability, with cloud demand playing a central role in driving performance.

OpenAI Changes Introduce New Risks

Recent adjustments to Microsoft’s partnership with OpenAI have added to investor caution. The revised agreement removes Microsoft’s exclusive access to OpenAI technology and ends revenue-sharing arrangements.

This shift opens the door for OpenAI to work more closely with competitors, including Amazon, increasing competitive pressure within the cloud market.

Outlook Turns More Cautious

Microsoft’s results confirm that demand remains strong, but the reaction suggests markets are raising the bar. With intensifying competition, rising costs, and strategic uncertainties, the company may need to deliver more than just solid growth to sustain investor confidence going forward.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts