AMD Stock Hits $240 on HSBC Downgrade After Record High – Earnings Preview

Advanced Micro Devices pulled back after reaching record highs as a downgrade, rising expectations, and upcoming earnings increased investor caution.

Quick overview

- AMD experienced a pullback after reaching record highs, influenced by a downgrade from HSBC and rising investor caution.

- Despite the decline, strong earnings from Intel indicate robust demand in the data center and AI sectors, benefiting AMD's market position.

- AMD's upcoming Q1 2026 earnings report is critical, with analysts expecting revenue around $9.8 billion and earnings per share between $1.24 and $1.30.

- Investor sentiment remains bullish, but concerns about high valuations and potential earnings misses could lead to significant market reactions.

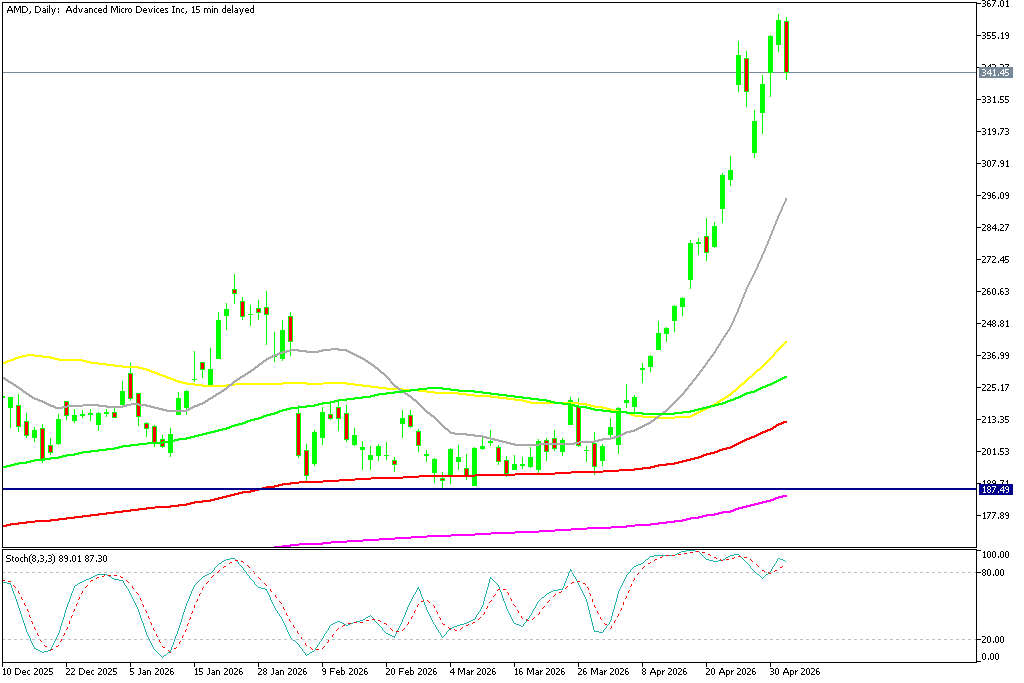

Live AMD Chart

[[AMD-graph]]

Advanced Micro Devices pulled back after reaching record highs as a downgrade, rising expectations, and upcoming earnings increased investor caution.

Record High Followed by Sharp Pullback

AMD recently climbed to an all-time high, supported by strong sector momentum and optimism around AI-driven demand. However, the rally quickly lost traction as the stock fell around 5% on Monday.

The decline followed a downgrade from HSBC, which cut its rating to “hold” from “buy,” warning that AMD may struggle to exceed already elevated expectations. Although the price target was raised slightly to $340, it still implied downside from recent levels near $360, a move that largely played out as shares dropped toward that range.

Intel Results Highlight Strong Demand

Despite the pullback, broader industry signals remain supportive. Strong earnings from Intel Corporation pointed to robust demand in data center and AI-related processors.

For AMD, this is viewed less as a competitive threat and more as confirmation of underlying market strength. Its EPYC server chips compete in the same space, meaning continued demand growth benefits multiple players across the sector.

Earnings Now a Critical Test

AMD is set to report Q1 2026 results, with analysts expecting revenue of roughly $9.8–$9.9 billion and earnings per share between $1.24 and $1.30.

Investor attention will center on data center performance, AI-related product demand, and forward guidance. With expectations already high, the results will need to be strong across multiple areas to sustain the stock’s elevated valuation.

- Revenue Consensus: ~$9.88B (approx. 33% YoY increase), despite a predicted 3.6% sequential dip.

- EPS Consensus: $1.24–$1.30 (vs. $0.96 in Q1 2025).

- Data Center Growth: Investors are looking for continued strength in MI300/MI308 GPU shipments and EPYC CPU demand to justify high valuations.

- Market Sentiment: Extremely bullish, with shares up nearly 60% this year, largely driven by AI optimism and strong rival results (Intel).

- AI Infrastructure Demand: Can AMD prove that demand is expanding beyond just GPUs into comprehensive AI infrastructure?

- Guidance vs. Expectations: Following previous disappointments, guidance will be crucial to justify the high stock price

- China Exposure: Impact of China-specific MI308 sales (approx. $100M guided).

- Upcoming Tech: Updates on “Venice” CPUs and MI500 GPUs.

- Rating: Strong Buy/Buy consensus.

- Price Targets: Recent upgrades, including D.A. Davidson, show targets as high as $375, indicating a potential upside of over 10% from pre-earnings levels

Share Price Reacts Swiftly

Following the earnings release, AMD shares fell sharply, sliding roughly 20% in January and pushing the stock below the $200 level. But the 100 SMA (red) acted as support on the daily chart. The price moved above and below $200 many times so the market was trying to decide which way to go, but decided on the upside in late March, breaking above the 50 daily SMA (yellow) and reaching a new record high of $353 late last week. The stock has reversed on Monday but AMD held above $300 nonetheless and rebounded strongly for three days reaching a new record.

AMD Chart Daily – Rebounding Off the 100 SMA

AI Narrative Faces Short-Term Pressure

While long-term growth tied to advanced computing remains intact, near-term sentiment is becoming more cautious. Weakness across semiconductor peers, including Broadcom Inc., suggests investors are reassessing how quickly demand will expand.

As workloads diversify beyond GPUs into CPUs and other architectures, growth may become more gradual, challenging assumptions of rapid expansion.

Valuation and Spending Concerns

AMD’s strong rally has pushed valuations higher, leaving limited room for disappointment. Even minor misses in earnings or guidance could trigger outsized market reactions.

At the same time, questions are emerging around the pace of large-scale infrastructure spending tied to companies like OpenAI. While long-term investment plans remain substantial, rising costs and tighter budgets are creating uncertainty about how quickly demand will materialize.

Conclusion

AMD’s long-term growth story remains supported by strong demand for high-performance computing and AI infrastructure. However, the combination of elevated expectations, valuation pressure, and near-term uncertainty creates a more fragile setup.

With earnings approaching, the stock faces a critical test where strong execution will be required to justify recent gains and sustain momentum.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts