MSFT Stock Fails at Resistance, Rising Costs and Competition Trigger Pullback

Growing worries about rising AI-related spending, escalating competition, and growing skepticism about whether future returns will warrant the company's enormous investment commitments have eclipsed Microsoft's recent accomplishments.

Quick overview

- Microsoft's recent stock rally has been dampened by concerns over high AI spending and competitive pressures.

- Despite strong earnings and product launches, investors are questioning the sustainability of Microsoft's valuation amid rising costs.

- The company's aggressive investments in AI and hardware introduce execution risks, particularly as enterprise customers remain cautious.

- Changes in Microsoft's relationship with OpenAI have raised investor uncertainty about the exclusivity and profitability of their partnership.

Growing worries about rising AI-related spending, escalating competition, and growing skepticism about whether future returns will warrant the company’s enormous investment commitments have eclipsed Microsoft’s recent accomplishments.

Microsoft’s Strong Rebound Faces a Reality Check

Shares of Microsoft Corporation surged over the past several trading sessions, climbing toward the $466 level as investors reacted positively to strong earnings, expanding AI initiatives, and new product launches. However, the rally lost momentum quickly, with the stock reversing sharply and falling more than 3.5% in the latest session.

The pullback highlights growing skepticism among investors who are increasingly questioning whether Microsoft’s valuation can continue expanding amid rising costs and growing competitive threats.

Although the company has recovered more than $100 from its earlier 2026 lows, technical resistance remains a significant obstacle, and some market participants believe the recent rally may have moved too far ahead of underlying fundamentals.

AI Expansion Continues Without Consumer Demand, Returns Remain Uncertain

Investor attention is now focused on Microsoft’s upcoming Build developer conference, where the company is expected to unveil a range of internally developed artificial intelligence models.

Reports suggest new products could target coding assistance, speech recognition, transcription, reasoning systems, and image generation capabilities. Microsoft is also expected to deepen integration across its software ecosystem, particularly within GitHub Copilot.

While these announcements reinforce Microsoft’s determination to remain a dominant force in enterprise AI, investors are becoming increasingly concerned about the gap between spending and monetization. The company continues to invest aggressively in infrastructure and development, but questions remain regarding how quickly these investments can generate sustainable profits.

Hardware Expansion Adds More Execution Risk

Microsoft recently introduced updated Surface Pro for Business and Surface Laptop for Business devices powered by Intel’s latest processors.

The company is positioning these devices as premium AI-enabled enterprise products capable of handling more advanced workloads directly on the device. Microsoft has promoted the new systems as powerful alternatives within the professional computing market.

However, the hardware strategy introduces additional risks. Enterprise customers remain cautious about technology spending, and investors are questioning whether premium pricing can be maintained in an increasingly competitive environment. Hardware investments also add another layer of execution complexity at a time when the company is already committing enormous resources to AI development.

OpenAI Relationship Evolves

Another source of investor uncertainty stems from Microsoft’s changing relationship with OpenAI.

Recent reports indicate that the companies have restructured portions of their agreement, reducing revenue-sharing obligations while giving OpenAI greater flexibility to work with competing cloud providers such as Amazon Web Services and Google Cloud.

While the revised arrangement may support OpenAI’s long-term ambitions, some investors view it as a weakening of Microsoft’s previously exclusive position within one of the most important AI partnerships in the industry.

Investors Grow More Cautious

Microsoft remains one of the strongest companies in the technology sector, but investors are becoming increasingly focused on the risks accompanying its ambitious AI strategy. Rising capital expenditures, evolving competitive dynamics, weakening exclusivity advantages, and slowing performance in certain business segments are beginning to overshadow otherwise impressive financial results.

While AI continues to drive optimism, the latest stock reversal suggests that investors are demanding clearer evidence that massive spending today will translate into sustainable profits tomorrow.

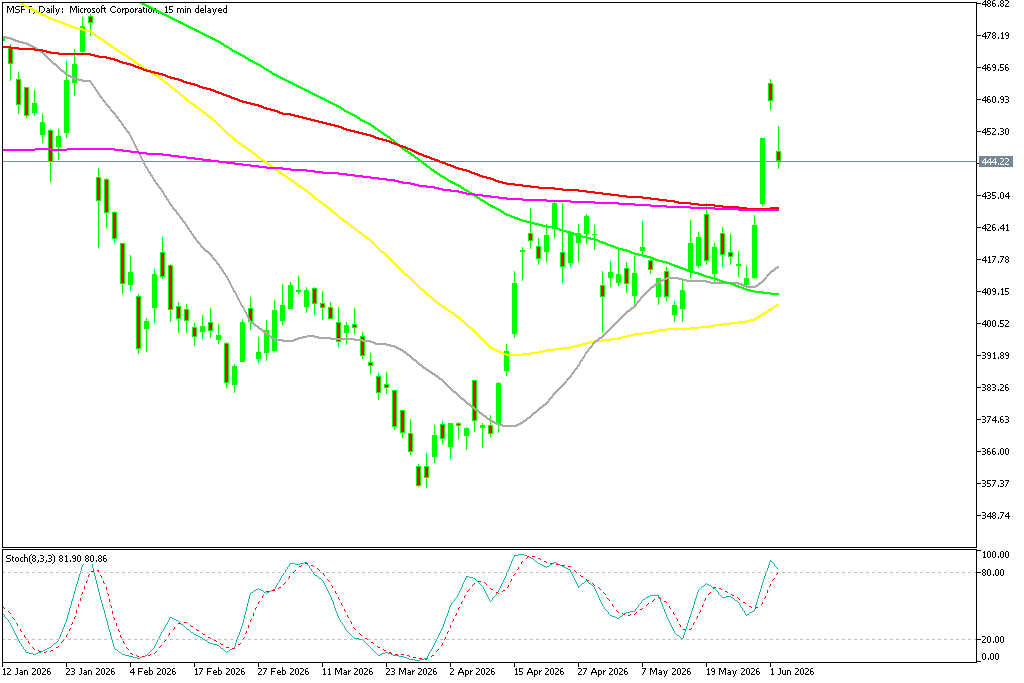

MSFT Stock Weakness – Breaks Key Support

Microsoft shares slipped below the critical $400 level last month but has reclaimed this level again after the surge last week, climb above $465. This area represents both psychological and technical resistance where a number of moving averages stand, making it an important line in the sand. Buyers failed to break above MAs on the weekly chart and we’re seeing a pullback today, with MSFT down to $444.

MSFT Chart Daily – The Price Returns Lower Again

Microsoft’s stock has undergone a notable repricing in recent months, signaling a broader reset in how investors are assessing mega-cap technology leaders. After peaking above $555 in October, shares retreated sharply, shedding around $200.

MSFT Chart Weekly – Failing at the 50 SMA

However the 50 monthly SMA (yellow) held as support once again and we’re seeing a strong rebound in April. But, buyers need to break above the 20 monthly SMA (gray) for the larger uptrend to resume, otherwise MSFT will likely fall below $400 again.

MSFT Chart Monthly – The Rebounding Off the 50 SMA Ran into the 20 SMA

Rising Spending Begins to Overshadow Strong Results

Despite delivering better-than-expected fiscal third-quarter results, Microsoft’s spending plans have become a growing source of concern.

The company now expects quarterly capital expenditures to approach $40 billion, while total fiscal 2026 spending could reach nearly $190 billion. Much of this investment is directed toward AI infrastructure, cloud capacity expansion, and automation initiatives.

Although Azure continues to post strong growth, competition remains intense. Rivals are investing aggressively to capture market share, creating concerns that future profitability could come under pressure even if revenue growth remains strong.

At the same time, Microsoft’s gaming business continues to struggle. Xbox hardware revenue has declined by more than 30% for a second consecutive quarter, highlighting weakness in parts of the company’s broader portfolio.

Microsoft Q3 2026 Earnings Highlights

Revenue beats expectations:

- Microsoft Corporation reported $82.9 billion in revenue, up 18% year-over-year, marking a record quarter and surpassing forecasts.

Profitability strengthens:

- Operating income rose 20% to $38.4 billion, while net income increased 23% to $31.8 billion, reflecting strong margin performance.

Earnings growth remains robust:

- Diluted earnings per share came in at $4.27, up 23% on a GAAP basis, signaling consistent bottom-line expansion.

Cloud Segment Drives Growth

Cloud revenue surges:

- Microsoft Cloud generated $54.5 billion, up 29% year-over-year, remaining the key growth engine.

Azure leads momentum:

- Azure and other cloud services grew 40%, highlighting strong enterprise demand for cloud infrastructure and advanced computing services.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts

Ava