MSFT Stock Heads to $400 as US Govt Investigation and AI Spending Weigh

Rising AI-related expenses, pressure from competitors, and uncertainty about long-term profits have caused Microsoft's recent surge to stop, resulting in fresh selling and a second session of declines in the stock.

Quick overview

- Microsoft's stock has declined for two consecutive sessions, falling below $430 as investor sentiment shifts from enthusiasm to caution.

- Ongoing regulatory scrutiny and rising AI-related costs are contributing to market uncertainty and investor concerns about future profitability.

- Despite strong fiscal third-quarter results, Microsoft's aggressive spending on AI infrastructure is overshadowing its revenue growth.

- The evolving relationship with OpenAI raises questions about the durability of Microsoft's competitive advantages in the AI ecosystem.

Rising AI-related expenses, pressure from competitors, and uncertainty about long-term profits have caused Microsoft’s recent surge to stop, resulting in fresh selling and a second session of declines in the stock.

Rally Fades as Sentiment Turns More Defensive

Shares of Microsoft Corporation have reversed sharply after a brief surge that pushed the stock toward recent highs near $466 earlier in the week. The initial advance was driven by optimism around strong earnings, expanding artificial intelligence initiatives, and continued product innovation across cloud and enterprise software.

However, that momentum has quickly faded. The stock has now fallen for two consecutive sessions, slipping below the $430 level as investor sentiment shifts from enthusiasm to caution. The reversal reflects growing unease that recent gains may have outpaced near-term fundamentals.

Regulatory Scrutiny Adds to Market Uncertainty

Sentiment has also been dampened by ongoing regulatory pressure. The U.S. Federal Trade Commission continues to expand its investigation into Microsoft Corporation, focusing on cloud services, artificial intelligence integration, and software bundling practices.

Although the outcome remains uncertain, the scope of the inquiry introduces the possibility of future operational constraints or structural changes. Investors are increasingly wary that regulatory action could limit Microsoft’s ability to fully capitalize on its integrated software and cloud ecosystem.

In parallel, broader government attention on artificial intelligence development—including voluntary model review frameworks—has added another layer of uncertainty for large-scale AI developers.

Rising AI Costs Fuel Investor Concern

A major driver of the pullback is increasing concern over Microsoft’s aggressive spending on artificial intelligence infrastructure. The company is committing substantial capital to expand data center capacity, integrate advanced AI systems across its product suite, and maintain competitiveness in a rapidly evolving sector.

While these investments are positioned as essential for long-term leadership, they are beginning to weigh on short-term financial expectations. Investors are increasingly questioning whether the scale of spending will translate into proportionate returns, particularly as capital intensity rises across the entire technology sector.

The result is a growing disconnect between strong revenue momentum and pressure on margins and free cash flow projections.

Evolving OpenAI Relationship Raises Questions

Another factor weighing on sentiment is the evolving relationship between Microsoft and OpenAI. Recent restructuring efforts have reportedly reduced certain exclusivity features and adjusted revenue-sharing arrangements, while giving OpenAI greater flexibility to work with competing cloud providers.

Although the changes may support OpenAI’s long-term strategic independence, they also dilute one of Microsoft’s most important competitive advantages in the AI ecosystem. Investors who previously viewed the partnership as a locked-in growth engine are now reassessing its durability and long-term value contribution.

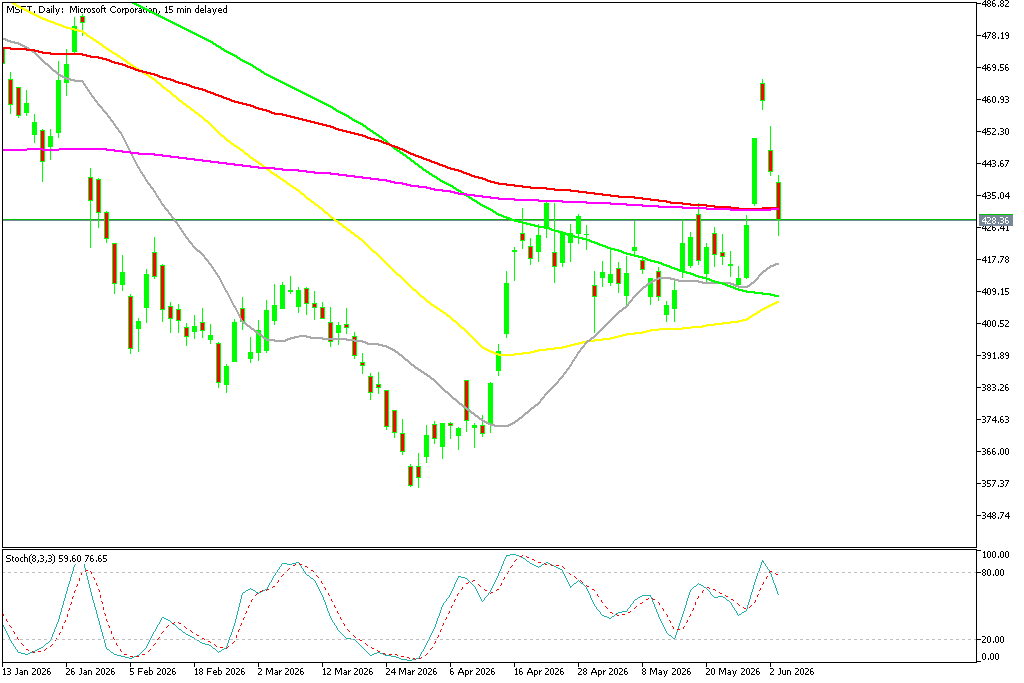

MSFT Stock Weakness – Breaks Key Support

Microsoft shares slipped below the critical $400 level last month but has reclaimed this level again after the surge last week, climb above $465. This area represents both psychological and technical resistance where a number of moving averages stand, making it an important line in the sand. Buyers failed to break above MAs on the weekly chart and we’re seeing a pullback today, with MSFT down to $444.

MSFT Chart Daily – The Price Returns Lower Again

Microsoft’s stock has undergone a notable repricing in recent months, signaling a broader reset in how investors are assessing mega-cap technology leaders. After peaking above $555 in October, shares retreated sharply, shedding around $200.

MSFT Chart Weekly – Failing at the 50 SMA

However the 50 monthly SMA (yellow) held as support once again and we’re seeing a strong rebound in April. But, buyers need to break above the 20 monthly SMA (gray) for the larger uptrend to resume, otherwise MSFT will likely fall below $400 again.

MSFT Chart Monthly – The Rebounding Off the 50 SMA Ran into the 20 SMA

Competition and Valuation Pressures Build

At the same time, competition in cloud computing and enterprise AI is intensifying, with rivals expanding aggressively and narrowing differentiation in key segments. This is making it more difficult for Microsoft to maintain the premium growth expectations embedded in its valuation.

Despite strong fundamentals, the combination of higher spending, regulatory uncertainty, and shifting partnership dynamics has created a more cautious market tone.

Rising Spending Begins to Overshadow Strong Results

Despite delivering better-than-expected fiscal third-quarter results, Microsoft’s spending plans have become a growing source of concern.

The company now expects quarterly capital expenditures to approach $40 billion, while total fiscal 2026 spending could reach nearly $190 billion. Much of this investment is directed toward AI infrastructure, cloud capacity expansion, and automation initiatives.

Although Azure continues to post strong growth, competition remains intense. Rivals are investing aggressively to capture market share, creating concerns that future profitability could come under pressure even if revenue growth remains strong.

At the same time, Microsoft’s gaming business continues to struggle. Xbox hardware revenue has declined by more than 30% for a second consecutive quarter, highlighting weakness in parts of the company’s broader portfolio.

Microsoft Q3 2026 Earnings Highlights

Revenue beats expectations:

- Microsoft Corporation reported $82.9 billion in revenue, up 18% year-over-year, marking a record quarter and surpassing forecasts.

Profitability strengthens:

- Operating income rose 20% to $38.4 billion, while net income increased 23% to $31.8 billion, reflecting strong margin performance.

Earnings growth remains robust:

- Diluted earnings per share came in at $4.27, up 23% on a GAAP basis, signaling consistent bottom-line expansion.

Cloud Segment Drives Growth

Cloud revenue surges:

- Microsoft Cloud generated $54.5 billion, up 29% year-over-year, remaining the key growth engine.

Azure leads momentum:

- Azure and other cloud services grew 40%, highlighting strong enterprise demand for cloud infrastructure and advanced computing services.

Outlook: Strong Business, Weaker Conviction

Microsoft Corporation remains one of the most dominant players in global technology, but investor conviction is weakening in the near term. The latest pullback suggests that markets are increasingly focused on the cost of AI leadership rather than just its potential.

As a result, even strong execution is no longer enough to sustain momentum when uncertainty around returns, regulation, and competition begins to dominate the narrative.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts

Ava