Tesla Stock Forecast: TSLA Slides Toward $368 Ahead of Earnings—Can Robotaxi Hype Rescue the Week?

Tesla stock ended the week under pressure despite record Q2 deliveries. Here is what investors should watch in earnings, including margins..

•

Last updated: Sunday, July 19, 2026

Quick overview

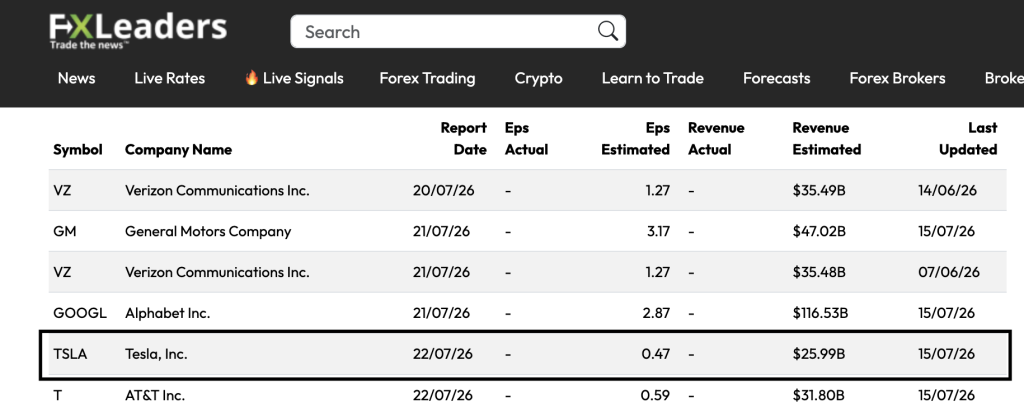

- Tesla is trading near $380 after losing the $391 support level, despite reporting record second-quarter deliveries of 480,126 vehicles.

- Investors are focused on whether Tesla can maintain profitability while pursuing ambitious AI projects, as margins are under pressure from competition and rising costs.

- The upcoming earnings report will be crucial, with attention on automotive gross margins, free cash flow, and updates on the robotaxi program.

- A strong earnings report could reverse recent declines, while weak margins or vague updates may heighten concerns about Tesla's valuation.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

ABOUT THE AUTHOR

See More

Arslan Ali Butt

Lead Markets Analyst – Multi-Asset (FX, Commodities, Crypto)

Arslan Ali Butt serves as the Lead Commodities and Indices Analyst, bringing a wealth of expertise to the field. With an MBA in Behavioral Finance and active progress towards a Ph.D., Arslan possesses a deep understanding of market dynamics.

His professional journey includes a significant role as a senior analyst at a leading brokerage firm, complementing his extensive experience as a market analyst and day trader. Adept in educating others, Arslan has a commendable track record as an instructor and public speaker.

His incisive analyses, particularly within the realms of cryptocurrency and forex markets, are showcased across esteemed financial publications such as ForexCrunch, InsideBitcoins, and EconomyWatch, solidifying his reputation in the financial community.

Related Articles

Sidebar rates

Related Posts

Ava