Qualcomm Drops 7% as Investors Reassess AI Valuations: Automotive and Edge AI Key Growth Drivers

Qualcomm stock QCOM falls 7% after a 62% rally as AI optimism cools, but automotive, IoT, and edge AI growth remain intact.

Written by:

Arslan Ali Butt•Thursday, June 11, 2026•3 min read

•Last updated: Thursday, June 11, 2026

Quick overview

Qualcomm shares fell nearly 7% amid a broader semiconductor selloff, despite the company's strong AI diversification strategy.

The stock's decline follows a significant rally earlier this year, with investors locking in profits due to rising bond yields and concerns about AI spending sustainability.

Qualcomm's AI strategy focuses on edge AI and automotive computing, with recent partnerships and a growing IoT business contributing to its expansion.

The company's valuation remains conservative compared to AI-focused peers, which could be advantageous if its new growth engines gain traction.

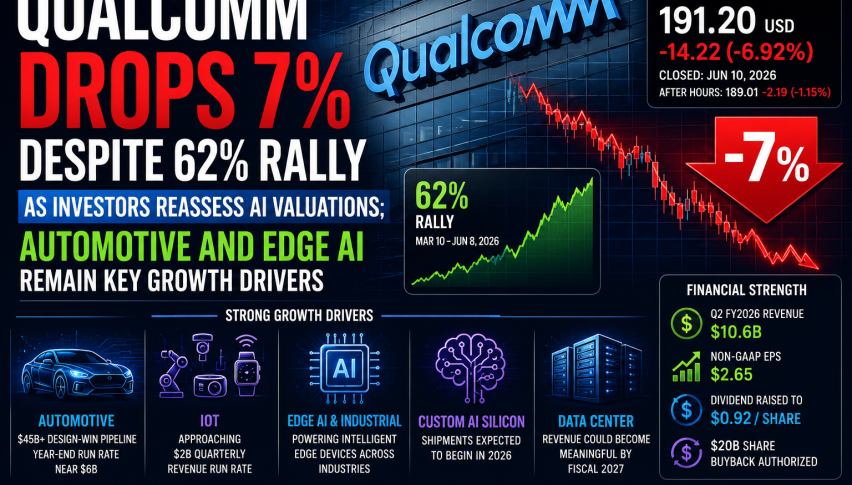

Qualcomm (NASDAQ: QCOM) shares plunged nearly 7% on Wednesday, extending a broader semiconductor selloff that swept through mobile and edge-computing chip stocks despite the company’s strong AI diversification strategy and growing presence beyond smartphones.

The stock closed at $191.20, down 6.92%, after reaching as high as $260 earlier this year. The decline comes after a remarkable 61.7% rally between March and early June, one of the strongest performances among large-cap semiconductor companies.

Investors appear to be locking in profits as rising bond yields, elevated valuations, and concerns about AI spending sustainability pressure the broader chip sector.

Qualcomm’s AI Expansion Story Continues to Evolve

Unlike Nvidia, Broadcom, or AMD, Qualcomm’s AI strategy is centered on edge AI, automotive computing, industrial automation, and connected devices rather than hyperscale AI data centers.

Recent developments highlight that transition:

Signed a new edge AI partnership with SLB for energy infrastructure automation.

Expanded automotive opportunities with a reported $45 billion design-win pipeline.

IoT business is approaching a $2 billion quarterly revenue run rate.

Custom AI silicon shipments are expected to begin in 2026.

Data-center revenue could become meaningful by fiscal 2027.

Raised quarterly dividend to $0.92 per share.

Authorized a $20 billion share repurchase program.

Qualcomm is also emerging as a strategic investor in next-generation robotics. The company recently participated in Neura Robotics’ $1.4 billion funding round, alongside Amazon and Nvidia, underscoring its long-term commitment to AI-powered autonomous systems.

Smartphone Business Remains the Largest Variable

The biggest challenge for Qualcomm remains its core handset business.

Although the company reported:

Revenue of $10.6 billion

Non-GAAP EPS of $2.65

Better-than-expected quarterly results

management acknowledged that smartphone shipments remain constrained by memory supply shortages and softer demand from some Chinese OEMs.

Investors continue to debate whether Qualcomm’s growth engines outside smartphones can scale quickly enough to justify a premium AI valuation.

That uncertainty explains why the stock trades at a significant discount to many AI-focused semiconductor peers.

Qualcomm’s Valuation Remains Reasonable Relative to AI Peers

Qualcomm’s valuation remains far more conservative than many AI-linked semiconductor stocks.

Key valuation metrics include:

Metric

Qualcomm

Market Cap

~$228 Billion

Forward P/E

~20x

Dividend Yield

~1.5%

Buyback Authorization

$20 Billion

Automotive Pipeline

$45 Billion

While Nvidia, Broadcom, and Arm command premium multiples tied directly to AI accelerator demand, Qualcomm remains priced closer to a diversified semiconductor company.

That could become an advantage if automotive, industrial AI, and edge computing continue gaining traction.

Is it a good time to buy Qualcomm (QCOM) stock?

QCOM Technical Analysis: Pullback Tests a Strong Long-Term Uptrend

Technically, Qualcomm remains in a correction phase after one of its strongest rallies in years.

The stock surged more than 60% in less than three months before encountering heavy profit-taking and broader semiconductor-sector weakness.

The indicators suggest short-term momentum has weakened significantly, though conditions are approaching oversold territory after the recent selloff.

Moving Average Structure

Moving Average

Level

Signal

10-Day EMA

$219.03

Sell

20-Day EMA

$216.29

Sell

30-Day EMA

$207.81

Sell

50-Day EMA

$193.15

Sell

100-Day EMA

$176.36

Buy

200-Day EMA

$167.53

Buy

Qualcomm currently trades below its short-term moving averages but remains comfortably above its 100-day and 200-day averages.

This setup typically reflects a correction within a broader uptrend rather than a complete trend reversal.

RSI and MACD

RSI (14) stands at 43.31, indicating neutral-to-weak momentum. The reading is approaching oversold territory but does not yet signal capitulation, suggesting sellers still maintain near-term control.

MACD remains at 8.40 but continues to flash a sell signal, reflecting deteriorating short-term momentum after the recent rally. However, the longer-term trend structure remains constructive as the stock continues to trade above major long-term support levels.

Volume and Trend Structure

The recent decline occurred on elevated trading volume, confirming that institutional investors participated in the selloff.

Importantly, the stock has retraced sharply from its recent highs but remains well above its March breakout levels. The current pullback resembles profit-taking after an extended rally rather than a breakdown driven by deteriorating fundamentals.

The broader trend remains tied to investor confidence in Qualcomm’s ability to diversify beyond smartphones and monetize emerging AI opportunities.

Key Support and Resistance Levels for QCOM Stock

Level Type

Approximate Area

Immediate Resistance

$198-$200

Major Resistance

$220-$230

Recent High Zone

$255-$260

Near-Term Support

$190-$193

Secondary Support

$175-$180

Major Trend Support

$165-$170

A recovery above the $200 area would improve the near-term technical picture and suggest buyers are returning after the recent correction. Conversely, a break below the $190 support zone could increase downside pressure toward the $175-$180 range.

Long-Term Outlook: Qualcomm Is Becoming More Than a Smartphone Company

The investment case for Qualcomm increasingly depends on diversification.

While smartphones remain the foundation of earnings, management is building multiple growth engines across:

Automotive computing

Industrial IoT

Edge AI

Robotics

Enterprise AI infrastructure

Custom AI silicon

Data-center acceleration

The market’s skepticism is understandable. Qualcomm is competing against Nvidia, Broadcom, AMD, Marvell, Texas Instruments, and NXP across several high-growth categories.

However, few semiconductor companies possess Qualcomm’s combination of wireless IP, edge computing expertise, automotive exposure, and cash-generation capability.

The recent selloff reflects valuation concerns and broader semiconductor weakness more than any deterioration in Qualcomm’s business fundamentals. For long-term investors, the key question remains whether edge AI, automotive, and custom silicon can eventually become large enough to reduce the company’s dependence on smartphones and unlock a higher valuation multiple.

Lead Markets Analyst – Multi-Asset (FX, Commodities, Crypto)

Arslan Ali Butt serves as the Lead Commodities and Indices Analyst, bringing a wealth of expertise to the field. With an MBA in Behavioral Finance and active progress towards a Ph.D., Arslan possesses a deep understanding of market dynamics.

His professional journey includes a significant role as a senior analyst at a leading brokerage firm, complementing his extensive experience as a market analyst and day trader. Adept in educating others, Arslan has a commendable track record as an instructor and public speaker.

His incisive analyses, particularly within the realms of cryptocurrency and forex markets, are showcased across esteemed financial publications such as ForexCrunch, InsideBitcoins, and EconomyWatch, solidifying his reputation in the financial community.