AMD Stock Risks Falling Below $500 as Investors Rotate Out of High-Cost US Chips

AMD shares retreated toward the important $500 level as investors adopted a more cautious stance toward semiconductor valuations, rising competition, and the long-term sustainability of the AI madness.

Quick overview

- AMD shares have retreated toward the $500 support level amid rising caution over semiconductor valuations and increased competition.

- The stock's recent decline follows a significant rally that peaked near $574, highlighting the volatility in investor sentiment within the semiconductor sector.

- Concerns about growing competition from Chinese memory manufacturers and a broader selloff in technology stocks have contributed to the downward pressure on AMD's shares.

- Despite positive developments and strong financial results, investor focus has shifted towards risk management and profit-taking, leading to increased volatility.

AMD shares retreated toward the important $500 level as investors adopted a more cautious stance toward semiconductor valuations, rising competition, and the long-term sustainability of the AI madness.

AMD Shares Reverse Lower as Semiconductor Weakness Intensifies

Advanced Micro Devices shares came under heavy selling pressure on Wednesday, reversing sharply lower and moving back toward the key $500 support zone.

The decline followed a remarkable rally that had pushed AMD to record highs near $574 only days earlier, highlighting how quickly sentiment can shift across the semiconductor sector.

After months of strong gains, AMD has spent much of July consolidating as investors increasingly rotate toward profit-taking and risk management rather than chasing momentum higher.

The move also reflects a broader pullback across technology stocks as concerns surrounding valuations and future growth expectations begin to outweigh near-term optimism.

Technical Momentum Begins to Fade

From a technical perspective, AMD’s latest decline has weakened the powerful upward trend that defined much of the year’s rally.

The stock is now testing an important support area around $500, a level that could prove significant for both short-term traders and long-term investors.

A sustained break below that zone could invite additional selling pressure as momentum investors reduce exposure and technical traders target lower support levels.

For now, buyers continue defending the area, but confidence appears noticeably weaker than during earlier stages of the rally.

Chinese Competition Raises Long-Term Questions

A major catalyst behind the latest selloff came from growing concerns surrounding competition in the global memory market.

According to a recent Barron’s report, Chinese memory manufacturers are rapidly increasing production capacity and market share, creating potential long-term challenges for established semiconductor companies.

Chinese producer ChangXin Memory Technologies, commonly known as CXMT, has emerged as the world’s fourth-largest DRAM manufacturer and continues expanding aggressively.

Reports that Apple is testing CXMT memory products for devices sold in China have attracted significant attention from investors.

At the same time, electric vehicle manufacturer Nio recently disclosed a $23.3 million investment in the Chinese memory producer.

The developments have raised concerns that growing Chinese scale could eventually pressure pricing power across portions of the memory industry.

Although AMD is not a pure memory producer, investors worry that greater competition across semiconductor markets could eventually weigh on margins and profitability throughout the sector.

Korean Semiconductor Selloff Spreads Globally

The weakness in AMD coincided with another sharp selloff across South Korea’s semiconductor industry.

SK Hynix suffered a steep decline while Samsung Electronics also moved sharply lower, dragging the broader semiconductor sector down with it.

The losses quickly spread into US markets as investors reassessed whether the premium valuations attached to AI-related companies remain justified.

Demand for AI hardware continues to be exceptionally strong, but markets are increasingly focusing on the durability of that demand rather than current conditions.

This shift in focus has created a more challenging environment for companies whose valuations depend heavily on future growth assumptions.

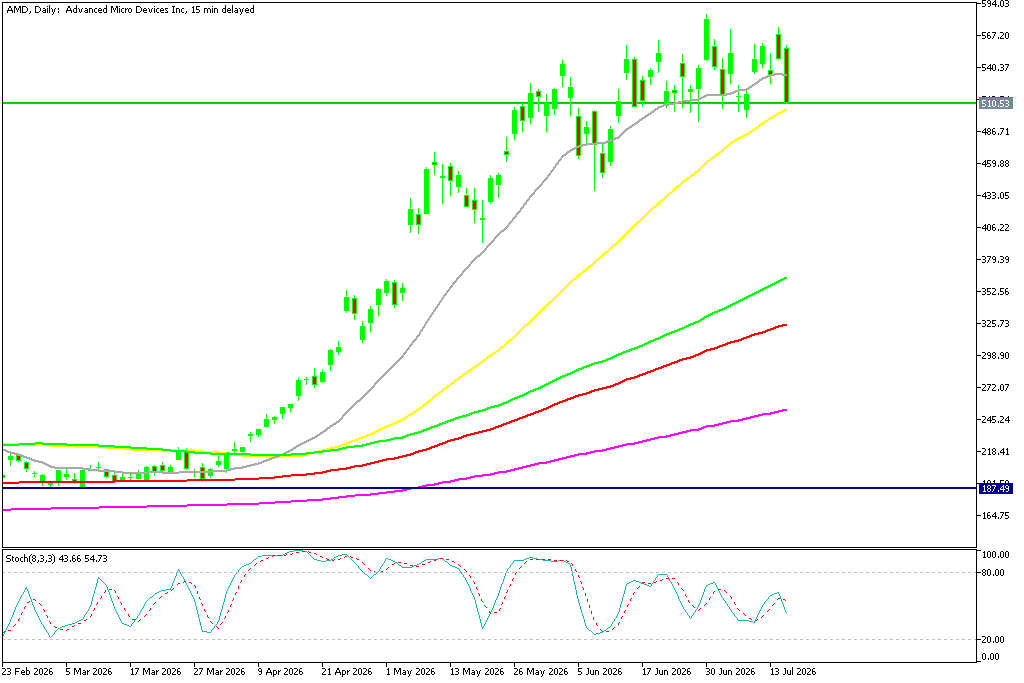

Share Price Reverses Swiftly

AMD shares fell sharply, sliding roughly 20% in January and pushing the stock below the $200 level. But the 100 SMA (red) acted as support on the daily chart. The price soared higher for three months, with the 20 daily SMA (gray) and reaching a high of $563 yesterday before reversing lower to $510 today.

AMD Chart Daily – Testing the 50 SMA

Positive Developments Fail to Support the Stock

The latest weakness is particularly notable because AMD entered the week with several positive catalysts supporting its long-term outlook.

Wells Fargo recently raised its price target on the stock, citing confidence in demand for AMD’s EPYC server processors and continued growth in AI infrastructure spending.

The company has also benefited from successful product launches, growing enterprise adoption, and strategic partnerships designed to strengthen its position in the data center market.

Under different market conditions, these developments may have provided enough support to extend the rally.

Instead, investors largely ignored the positive news and focused on preserving gains accumulated during the stock’s powerful advance.

Supply Chain Costs Add Another Layer of Risk

Investor caution has also increased following reports that AMD may raise prices on certain Radeon graphics products and graphics memory components.

The proposed increases are reportedly linked to higher memory costs and tighter supply conditions for graphics components.

While higher prices could support margins, they also create risks for consumer demand, particularly in the gaming segment where buyers tend to be more sensitive to pricing changes.

Gaming remains an important contributor to AMD’s revenue base, making any slowdown in consumer demand a potential concern.

Valuation Becomes the Dominant Debate

Perhaps the biggest challenge facing AMD is the valuation premium created during its extraordinary rally.

Much of the company’s market value reflects expectations for years of strong earnings growth driven by artificial intelligence adoption and data center expansion.

Those expectations leave little room for disappointment.

As a result, even modest shifts in investor sentiment can trigger significant volatility in the share price.

Higher interest rates and uncertainty surrounding future monetary policy have only amplified these concerns, encouraging investors to rotate away from richly valued growth stocks during periods of market stress.

For AMD, the long-term growth story remains intact, supported by competitive products and expanding opportunities in AI infrastructure.

However, the recent retreat toward $500 suggests investors are becoming increasingly selective about how much they are willing to pay for future growth.

Until confidence improves regarding valuations and the durability of the semiconductor investment cycle, AMD shares may continue experiencing periods of elevated volatility despite maintaining strong underlying fundamentals.

| GAAP Quarterly Financial Results |

|||||

| Q1’26 | Q1’25 | Y/Y | Q4’25 | Q/Q | |

| Revenue ($M) | $10,253 | $7,438 | Up 38% | $10,270 | Flat |

| Gross profit ($M) | $5,416 | $3,736 | Up 45% | $5,577 | Down 3% |

| Gross margin | 53% | 50% | Up 3 ppts | 54% | Down 1 ppt |

| Operating expenses ($M) | $3,940 | $2,930 | Up 34% | $3,825 | Up 3% |

| Operating income ($M) | $1,476 | $806 | Up 83% | $1,752 | Down 16% |

| Operating margin | 14% | 11% | Up 3 ppts | 17% | Down 3 ppts |

| Net income ($M) | $1,383 | $709 | Up 95% | $1,511 | Down 8% |

| Diluted earnings per share | $0.84 | $0.44 | Up 91% | $0.92 | Down 9% |

| Non-GAAP(*) Quarterly Financial Results | |||||

| Q1’26 | Q1’25 | Y/Y | Q4’25 | Q/Q | |

| Revenue ($M) | $10,253 | $7,438 | Up 38% | $10,270 | Flat |

| Gross profit ($M) | $5,685 | $3,992 | Up 42% | $5,855 | Down 3% |

| Gross margin | 55% | 54% | Up 1 ppt | 57% | Down 2 ppts |

| Operating expenses ($M) | $3,145 | $2,213 | Up 42% | $3,001 | Up 5% |

| Operating income ($M) | $2,540 | $1,779 | Up 43% | $2,854 | Down 11% |

| Operating margin | 25% | 24% | Up 1 ppt | 28% | Down 3 ppts |

| Net income ($M) | $2,265 | $1,566 | Up 45% | $2,519 | Down 10% |

| Diluted earnings per share | $1.37 | $0.96 | Up 43% | $1.53 | Down 10% |

Segment Summary

- Data Center segment revenue was $5.8 billion, up 57% year-over-year, driven by strong demand for AMD EPYC™ processors and the continued ramp of AMD Instinct™ GPU shipments.

- Client and Gaming segment revenue was $3.6 billion, up 23% year-over-year. Client business revenue was $2.9 billion, up 26% year-over-year, primarily driven by strong demand for leadership AMD Ryzen™ processors and continued market share gains. Gaming business revenue was $720 million, up 11% year-over-year, driven by solid demand for AMD Radeon™ GPUs partially offset by lower semi-custom revenue.

- Embedded segment revenue was $873 million, up 6% year-over-year, as demand strengthened across several end markets.

Recent PR Highlights

- AMD expanded its data center offerings and deepened strategic collaborations to deliver global compute infrastructure:

- Meta and AMD announced plans to deploy up to 6 gigawatts of AMD Instinct GPUs, with the first 1-GW to be powered by a custom AMD Instinct MI450-based GPU. Meta will also be a lead customer for the upcoming 6th Gen AMD EPYC CPUs, codenamed “Venice” and “Verano.”

- AWS, Google Cloud, Microsoft Azure and Tencent announced new and expanded 5th Gen EPYC-powered cloud instances, including Google Cloud H4D VMs for HPC and Azure instances across general-purpose, memory- and compute-optimized workloads.

- In the latest MLPerf® results, AMD Instinct MI355X delivered strong competitive performance across the full suite, with leadership results in multiple categories.

- AMD announced EPYC 8005 server CPUs, delivering leadership performance per-watt-per-dollar optimized for telecommunications and edge environments.

- AMD and Tata Consultancy Services (TCS) are co-developing AMD Helios-based rack-scale AI infrastructure to accelerate enterprise AI deployments and sovereign AI initiatives in India.

- AMD and Samsung are collaborating on next-generation AI memory and compute technologies, including HBM4 supply for AMD Instinct MI455X GPUs and advanced DRAM solutions for 6th Gen AMD EPYC CPUs.

- AMD is collaborating with NAVER Cloud and Upstage to deploy AMD Instinct GPUs and EPYC CPUs across their AI infrastructure, advancing sovereign AI initiatives in Korea.

- AMD joined Open Telco AI, a GSMA-led initiative to accelerate telco-grade AI models and systems, with AMD Instinct GPUs training Open Telco AI models.

- AMD expanded its offerings for premium enterprise and enthusiast PCs, including:

- The AMD Ryzen AI PRO 400 Series processors, expanding its lineup of next-generation enterprise desktop PCs that deliver Copilot+ experiences.

- The Ryzen 9950X3D2 Dual Edition processor, delivering enhanced performance for creative and developer workloads with dual stacks of AMD 3D V-Cache™ technology.

- AMD announced new adaptive and embedded AI processors, including:

- New Ryzen AI Embedded P100 Series processors, delivering scalable, power-efficient AI compute for industrial and edge applications.

- The Kintex™ UltraScale+™ Gen 2 family of mid-range FPGAs, delivering advanced memory bandwidth and I/O performance for industrial, imaging and broadcast applications.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts