Forex Signals US Session Brief, Oct 30 – Some Positive Numbers From the US Ahead of the FED Meeting

The US GDP report came out better than expected for Q3, but USD traders are remaining on the sidelines ahead of the FED meeting

The global economy has been weakening for more than a year. The manufacturing sector and the industrial production have been hit the hardest from the trade war. The US economy, on the other hand, was holding up well until Q2, but it started slowing down as well and the slowdown picked up pace in recent months. As a result, the FED has turned quite dovish, cutting interest rates twice in the last two meetings and they are expected to cut them again today. The economic data has been pretty soft,which has forced the FED to take action, but today’s numbers weren’t too bad.

The ADP employment report came as expected at 125k, which is not great, but it has been steady in the last few months. Job creation was spread across all businesses which is a good sign. The GDP for Q3 was expected to slow down considerably to 1.6% from 2.0% previously, but it came at 1.9%, which is not too bad either, considering the soft data in recent months. The FED will go ahead and cut rates again today, but after the GDP report, they will likely pause for some time. The Bank of Canada kept interest rates unchanged as well, but the statement leaned more on the dovish side, sending the CAD around 100 pips lower.

The European Session

- Mnuchin Feels Positive About US Economy – US Treasury secretary, Steven Mnuchin was speaking in Riyadh, Saudi Arabia this morning, saying that the US economy is strong, with low unemployment and low inflation. But there is no question that global growth is slowing down. Europe needs to do more on the fiscal side and regulation to maintain growth. There goes another guy asking the German government to increase fiscal spending.

- French GDP and Consumer Spending – French economy slowed down in Q2,posting a 0.2% increase in the GDP in the initial reading. Although, that was revised higher today to 0.3%. For Q3, the GDP was predicted to have grown by 0.2%, but it beat estimates, posting a 0.3% growth once again. So, the economy looks steady. Consumer spending for August fell flat as last month’s report showed, but it was revised higher to 0.1% today. For September, spending was expected to fall flat at 0.0% again, but it missed expectations, posting a 0.45 decline.

- German CPI Inflation – Inflation has been weakening in Germany in recent month, as in the rest of the Eurozone. In August CPI (consumer price index) inflation declined by 0.2%, while last month CPI fell flat at 0.0%. This month inflation was expected to came out flat once again, but it beat expectations, showing a 0.1% increase. Although, that was anticipated by the time it was released because regional CPI figures from German regions beat expectations as well.

- UK Money Supply – The global economy has been weakening for more than a year and the economy of the Eurozone is where the weakness is more evident. The manufacturing and industrial sectors have been in recession for quite some time and the recession is getting deeper, instead of improving. Eurozone final consumer confidence declined to -7.6 points from -6.5 prior. Economic confidence softened to 100.8 points against 101.1 expected, business climate indicator came in at -0.19 points vs -0.24 expected. Industrial confidence deteriorated further to -9.5 points against -8.8 expected and services confidence also softened to 9.0 points vs 9.2 expected.

The US Session

- US ADP Non-Farm Employment Change – ADP non-farm employment change was expected to increase by 125K this month and the actual number came right on expectations at 125K. The previous month stood at 135K, but was revised lower to 93K today. Small businesses added +30K new jobs, medium sized businesses added +39K, while large businesses added +67K new jobs. Goods producing sectors added +8K new jobs, while service providing businesses added +127K jobs. This is a decent report, since job gains were spread across all businesses. But the downward revision for last month took some of the shine off this report.

- US Prelim Q3 GDP Report – US GDP report for Q3 has been released. The prelim reading was expected to show a slowdown to 1.6% on an annualized basis. The economy cooled off indeed, but by a lot less than markets were anticipating. The annualized GDP for Q3 came at 1.9%. Personal consumption increased by 2.9%, against 2.6% expected but down from 4.6% previously. The GDP price index cooled off to 1.7% against 1.9% expected. Personal consumption added 1.93% to the GDP, while gross private investment took off -0.27%.

- BOC Rate Decision – Bank of Canada left interest rates unchanged today at 1.75%. They were about to start easing the monetary policy a couple of months ago, but the recent economic data from Canada has shown stability and the BOC is remaining on the sidelines now. So, they kept rates unchanged as expected.

- BOC Statement – In the statement, the BOC said that resilience of Canadian economy ‘will be increasingly tested’ as trade conflicts and uncertainty persist. H2 growth expected to slow to a rate below potential due to trade, weak energy sector and unwinding of temporary factors. The BOC boosted 2019 forecast to 1.5% from 1.3% previously, but cuts 2020 GDP forecast to 1.7% from 1.9% and 2021 to 1.8% from 2.0%. Global growth expected to be slowest this year since financial crisis, but forecast to rise next year. Will pay close attention to sources of resilience in Canadian economy like consumer spending and housing activity. Trade risks are two-sided now but tilted to downside. Consumer spending is choppy but will be supported by income growth. Business investment and exports likely to contract in H2 before expanding again in 2020 and 2021.

Trades in Sight

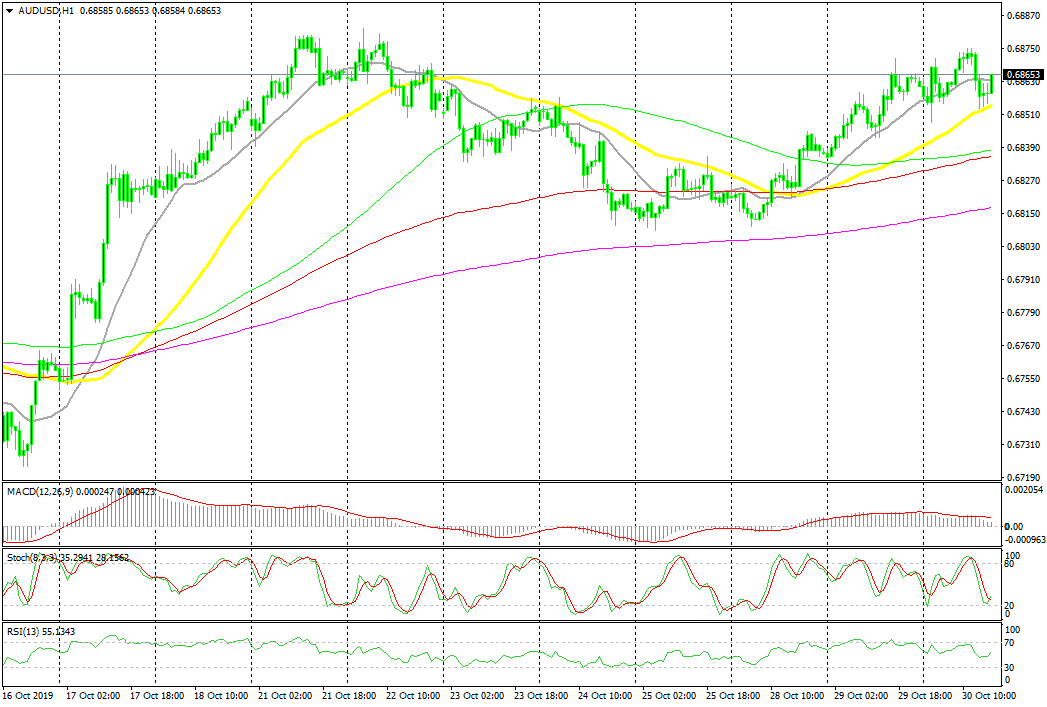

Bullish AUD/USD

- The trend has turned bullish

- the retrace down is complete on the H1 chart

- The 50 SMA has turned into support

- The previous 2 candlesticks point up

The 50 SMA is defining the trend for AUD/USD

AUD/USD has been bearish for a long time, but it turned higher in the third week of this month after comments that US and China were reaching a partial trade deal. As a result, this pair climbed more than 100 pips higher. Although, it retreated lower last week, but the bullish trend resumed again this week. Today we saw another pullback lower on the H1 chart, but the retrace seems complete now, with stochastic being oversold. The last two H1 candlesticks closed as dojis, which are reversing signals, and the 50 SMA (yellow) turned into support, so this pair is heading higher now.

In Conclusion

Markets have been quiet today and I expect them to remain like that as we head into the FED meeting this evening. The US GDP report and the ADP non-farm employment report leaned on the positive side today, helping the Buck for a while, but traders have taken the sidelines again just to be on the safe side until the FED is done with markets.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts